How 25 companies claimed more than $15 Billion in tax breaks over the last 5 years

Introduction

When the Domestic Production Activities Deduction (DPAD) became law in 2004, proponents described it as a way to help American companies manufacture in the United States and export products abroad. In recent years, the DPAD has grown into one of the largest corporate tax expenditures,[i] with an estimated cost of more than $15 billion in 2016 and $174 billion over the next 10 years.[ii] At the same time, the DPAD has been criticized for being ineffective, overly complicated, and creating distortions in the economy. The top 25 companies that receive the greatest benefit from this break include several that mainly write software, five media companies, two tobacco companies, two energy companies and a food processor.

The deduction is too small to incentivize manufacturing, as it is intended to do. The deduction allows a 9 percent deduction for profits from domestic production activities, which can only reduce the tax rate on income earned from these activities by a few percentage points. (9 percent of the corporate tax rate of 35 percent comes to just 3.15 percentage points.) It is unlikely that this small break could prod companies to do anything they would not have done even in the absence of any such tax break.

An expansion of the deduction would be enormously costly and would increase the administrative and economic problems that come with defining what activities qualify for this break. If more companies claimed the deduction, this would only increase the impossible burden on the IRS to determine which activities qualify as “production” and would increase the economic distortions that result from subsidizing some types of commerce over others.

For example, retail food operations are not eligible for the deduction, but food processing is eligible, which means that a coffee house is eligible if it roasts coffee beans. Restaurants, in theory, are ineligible but the Cheesecake Factory takes the manufacturing deduction for “producing” cheesecake by putting garnishes on pre-baked cheesecakes and slicing them. Writing software is eligible but designing some apps is not eligible. World Wrestling Entertainment uses the deduction for producing wrestling-related films. The IRS rejected the claim of sports teams that they produce television entertainment, but it allowed networks airing sports to claim the deduction.

The IRS is a tax collection agency and it is not obvious that making these decisions are the best use of its time, and yet this is unavoidable when a subsidy for domestic production is provided through the tax code.

Supporters of this deduction argue that all this administrative complexity and economic distortion could be justified if DPAD boosts economic output or growth, but it is difficult to see how it possibly could. The 25 companies receiving the largest benefits are generally profitable and indeed tax deductions can only be taken by a company with profits. Companies do what is profitable with or without a tax break, thus this deduction is not an incentive. In truth, lawmakers have created a costly tax subsidy for profitable companies to incentivize business activities that they would have taken on anyway. The report shows that the DPAD is an ineffective and inefficient policy for incentivizing the manufacturing sector and concludes that there is no economic justification to maintain the DPAD in its current form. Discussing several reform options, it concludes that full repeal of the deduction is the best option.

Background

Origin and development

The US, like many other countries, has a long history of policies supporting its export industry. For example, the extraterritorial income (ETI) exclusion allowed firms to exclude certain export-related income from taxation. After the World Trade Organization ruled against this provision in 2002, the U.S. enacted DPAD in part to compensate exporting firms for the repeal of the ETI. Focusing on overall domestic manufacturing, the DPAD is broader than the ETI exclusion, but is intended to incentivize exports in a similar way on the theory that exports increase when domestic markets are satisfied. Congress phased in DPAD over a 10-year period, with a 3 percent deduction allowed in 2005 and 2006, 6 percent allowed in 2007-2009, and its current full rate of 9 percent allowed since 2010. One exception is the lower deduction rate for oil-related activities,[iii] which the Emergency Economic Stabilization Act fixed at 6 percent in 2008.[iv] Since its enactment, different groups have argued for both its expansion and its repeal.[v]

Description

Also referred to as section 199 – after its place in the federal corporate tax code – the DPAD is calculated as a percentage of the income attributable to certain production activities that take place within the United States (e.g., domestic production activities). This so-called Qualified Production Activities Income (QPAI) is defined as ‘income derived from the production or property that was manufactured, produced, grown, or extracted within the United States’.[vi] Electricity, natural gas, and potable water production is also eligible, as is film production. Domestic construction projects, as well as engineering and architectural services associated with such projects, also qualify. However, the QPAI definition is not very specific and open for interpretation; see for example the – sometimes amusing – QPAI claims in the next section. It is estimated that the DPAD, which was intended to target the manufacturing sector, now covers over one-third of total corporate activity.[vii] [viii]

Companies qualifying for the DPAD can reduce their effective tax rate by as much as 3.15 percent (2.1 percent for oil and gas companies).[ix] The amount of the deductions is limited by two factors: (1) the firm’s wages and (2) the amount of the firm’s taxable income. Specifically, the deduction cannot exceed 50 percent of the firm’s W-2 wages related to production revenues, and firms must report positive taxable income to claim the deduction. Firms with no taxable income in a given year cannot claim the deduction.[x]

Examples of (claimed) QPAI

The IRS definition of QPAI is open for interpretation. Since its introduction, many firms tried to claim – and sometimes got – the deduction for activities that are hard to describe as ‘manufacturing’. A few examples:

- World Wrestling Entertainment gets the DPAD for the ‘domestic manufacturing’ of wrestling-related films, reducing its effective corporate tax rate by almost 3 percent in 2015.[xi]

- Cheesecake Factory restaurants claiming an almost 3 percent deduction for taking pre-baked cakes and putting garnishes on them, or for simply slicing cheesecake; claiming to be literal cheesecake factories.[xii]

- Sports teams have even tried to claim it, saying they manufacture television entertainment. Although this effort was unsuccessful, the networks airing sports can in fact claim the deduction.[xiii]

- Similarly, television show producers, networks and cable companies have claimed the deduction for respectively manufacturing or airing tv shows and combining channels into a bundle. These companies now belong to the top DPAD beneficiaries with only five media companies this year claiming over half a billion dollars in deductions (see Table 1).[xiv]

- Hardware stores have claimed to be factories since they cut blank keys for customers. Similarly, paint stores claim they should receive the credit due to the fact they shake the paint cans before selling them to customers.[xv]

- Apparently, putting together a fruit basket may be considered manufacturing since they claim that it involves assembling fruit in a package. Similarly, the flower delivery company 1800flowers.com has tried to claim the credit for assembling bouquets of flowers.[xvi]

Magnitude

Budgetary impact

Since its enactment in 2004, the DPAD has developed into one of the most expensive corporate tax expenditures. Its cost increased from $3.27 billion in 2005 to $15.23 billion in 2016, which can be explained by the increasing phase-in rates before 2010, but also by the increasing number of Section 199 filings with on average higher reported QPAI claims over this period.[xvii] The Joint Committee on Taxation (JCT) estimates that its cost will continue to rise and total $174 billion over the next 10 years.[xviii]

Since most states base their tax laws on the federal tax code, many states’ budgets are affected by the DPAD, which was automatically adopted by many states without specific legislative scrutiny or a vote. The Center on Budget and Policy Priorities estimated that the 25 states allowing the DPAD lost more than $635 million in corporate tax revenue in 2014.[xix] As the same report points out, there is no good reason for states to allow this deduction. Because the DPAD is based on total US income and is mostly used by big companies with facilities in many states, it is unlikely that DPAD will create jobs within any specific state allowing the deduction. Moreover, the deduction provides little help to struggling businesses within a state, since only profitable businesses can use it.

25 companies with largest DPAD benefits

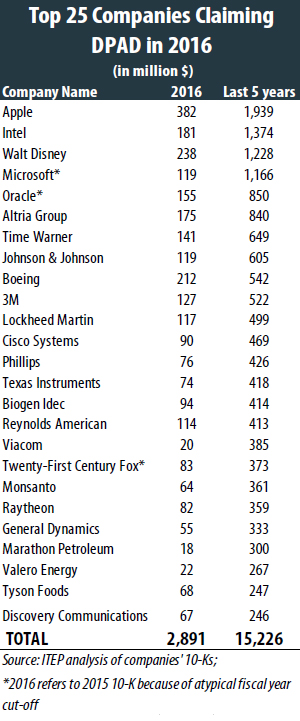

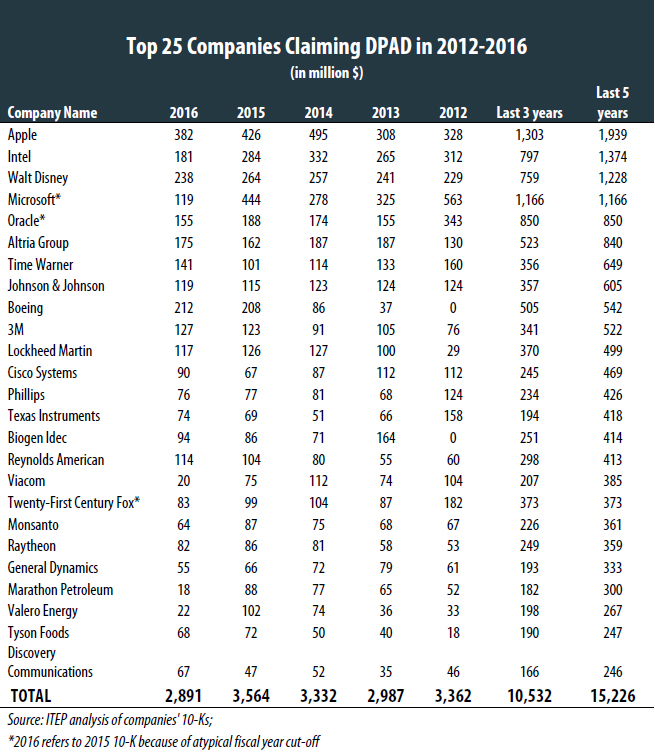

It is well documented that the DPAD is skewed to bigger public-owned companies. The largest companies, with more than $1 billion in assets, claim more than 85 percent of the total deduction, with large public corporations reporting 75 percent (and large private firms reporting 10 percent).[xx] However, less is known about which companies are the biggest beneficiaries of the DPAD. This report takes a closer look at the 25 companies reporting the highest DPAD claims over the last five years. Table 1 shows these companies’ DPAD related benefits for fiscal year 2016,[xxi] ranked based on their five-year cumulative DPAD benefits.[xxii] [xxiii] These 25 companies lowered their federal income tax bills by $2.9 billion in 2016; almost one-fifth (19 percent) of the total DPAD claims in that year. The same companies claimed over $15 billion in DPAD tax benefits over the last five years, with one-third being claimed by only five companies. Looking at this list, what stands out is that four of the companies in the top five are large tech companies, while the other one profits from the media/entertainment exclusion. This is representative of the overall list, which includes five big media/entertainment companies, seven high-tech firms, two tobacco firms and two companies with activities related to oil and gas. Notably, the list only includes five to nine companies which are generally viewed as being traditional, manufacturing companies

Evaluation

Congress introduced the DPAD to support the overall manufacturing sector, but there is no evidence that the deduction resulted in more manufacturing jobs since its introduction in 2004. On the industry level, the Progressive Policy Institute (2013) for instance finds no correlation between the share of an industry’s DPAD claims as a share of its revenues and the industry’s employment growth.[xxiv] Using a more sophisticated firm-level analysis, Lester (2016) finds no relation between the DPAD and job growth and only a slightly positive relation with domestic investment.[xxv] This section elaborates on some of the reasons for the DPAD’s ineffectiveness, as well as other problems associated with the DPAD, including its complexity, high compliance costs and distortive effect on the economy.

First of all, the deduction is poorly targeted to those industries and companies it was intended to support. Through its overly-broad definition of eligible income, about one-third of corporate economic activity now qualifies for the deduction.[xxvi] At the same time, only 65 percent of the deduction was attributable to the manufacturing sector in 2012, while 13 and 6 percent were claimed by the highly profitable information and mining sector (which includes oil- and gas activities), respectively.[xxvii]

Likewise, the DPAD is skewed to more profitable and bigger businesses, which raises the question if these companies need the extra incentive in the first place. For well-performing firms, the DPAD – at least partly – subsidizes investments which they would likely have made anyway, resulting in a deadweight loss. At the same time, the fact that only profitable businesses can use the DPAD makes it of little help to support struggling businesses that need it most. As such, the DPAD functions more like a special interest subsidy than a well-targeted incentive.

Moreover, economic theory suggests that the DPAD is an inefficient policy to stimulate physical investment and job creation in general. As Lester (2016) points out, firms respond to legislative changes in the tax code in the most cost-effective way possible, which often includes shifting income over time (inter-temporal shifting) or jurisdictions (accounting re-characterization).[xxviii] Real physical domestic investment — which is associated with job creation – is more expensive and will only be considered after making full use of the first two options. Using a control group of firms ineligible for the DPAD, Lester (2016) finds evidence that firms avoid taxes by shifting significant amounts of income over time and jurisdictions to maximize their DPAD tax benefit. But even if the DPAD would result in more real domestic investment, this does not automatically translate into job growth if primarily invested in capital or automatizing work.[xxviv]

Another problem with tax expenditures like the DPAD is that they increase the complexity of the tax code, resulting in more uncertainty and higher compliance costs for both the IRS and firms. Because it is often not clear which activities are eligible for the DPAD, firms often do not know if their claims will be honored, which increases uncertainty and limits investment. The complexity of the DPAD regulations moreover increase firm’s compliance costs, including the administrative burden and extra bookkeeping costs.[xxx] The IRS in turn experiences higher collection and enforcement costs to combat misuse. Moreover, the IRS must spend much of its scarce resources on court cases involving obscure QPAI claims – including sport teams who claim to manufacture television entertainment and restaurants claiming to produce cheesecake by simply slicing it.[xxxi]

Besides its limited effectiveness and high (compliance) costs, the DPAD causes distortions in the economy. By increasing the after-tax return to investments in certain industries, the DPAD distorts the allocation of capital and limits economic efficiency. In other words, the DPAD lowers the overall productivity of capital and labor in the economy by favoring certain industries over others. The arbitrary nature of the eligible activities cause economically unjustifiable distortions both between and within industries.[xxxii] For example, food processing qualifies, but not retail food businesses—unless the food establishment roasts beans used to brew coffee — the infamous Starbucks exception.[xxxiii] Another example is the high-tech sector, where software development is favored over some forms of app design and cloud computing.[xxxiv] Lacking an economic justification, these differences distort investment decisions, limit economic efficiency, and likely retard economic growth.

Policy options

The last section detailed the myriad of problems associated with the DPAD in general, including its ineffectiveness in stimulating manufacturing jobs, related deadweight loss, high compliance and enforcement costs, and distorting effects on the economy. Given these problems, there is no economic justification for the DPAD and therefore it should be repealed on both the federal and state level.

At the federal level the DPAD should either be phased out or immediately abolished. Immediate repeal would raise $174 billion over the next 10 years,[xxxv] money that could be used to support the federal budget.[xxxvi] Repealing the DPAD at the state level would likely raise over $635 million and could easily be accomplished by adding a single sentence to state tax law disallowing the deduction.[xxxvii]

Short of full repeal, there are a number of ways that the DPAD could be reformed. Sensibly limiting the DPAD to the manufacturing and production sector would raise $65 billion over ten years.[xxxviii] Eliminating the deduction for the oil, gas, coal, and other fossil fuel companies would raise $18 billion over the same period.[xxxix] By preventing companies without significant overseas sales from claiming the deduction, another $30 billion could be saved.[xl] But the easiest way to limit the costs of the DPAD would be to simply lower its deduction rate, for instance back to its phasing-in rates of 6 or 3 percent. It is estimated that this would raise respectively $55 and $125 billion between 2014 and 2023.[xli] Although these reforms would reduce the number of DPAD claims and their costs, they do not deal with the more fundamental problems associated with the DPAD.

Conclusion

The DPAD has grown into one of the most expensive corporate tax expenditures, costing over $15 billion in 2016 and an estimated $173.7 billion over the next10 years. Almost one-fifth of this tax break goes to only 25 companies, claiming over $15 billion in DPAD related benefits over the last five years. Most of these companies are not the struggling manufacturing and export-focused companies the DPAD was intended to support, but rather highly profitable companies in industries such as the high-tech, mass media, tobacco and oil and gas sector. This is illustrative of the more fundamental problems with this costly provision, which now covers over one-third of corporate activity. There is no evidence that the DPAD stimulates manufacturing employment. At the same time, by arbitrarily favoring some corporate activity over others, it distorts investment decisions both between and within industries, limiting economic efficiency. As such, the DPAD functions more like a special interest subsidy than a well-targeted incentivizing policy. Moreover, by making the tax code even more complex, the DPAD facilitates tax avoidance and increases both compliance and collection cost for companies and the IRS. Considering these arguments, this report concludes that there is no economic justification for the DPAD and its costs and hence joins the growing number of voices calling for its repeal.

Appendix

[i] Only deferral, state and local bonds, and accelerated depreciation are bigger, costing respectively $222.030, $47.080 and $30.500 billion in 2016. See for a full overview of all tax expenditures and their projections: Office of Management and Budget,”Budget of the U.S. government: Tax Expenditures Fiscal Year 2018,”2017, https://www.whitehouse.gov/sites/whitehouse.gov/files/omb/budget/fy2018/ap_13_expenditures.pdf

[ii] See Congressional Budget Office,”Options for Reducing the Deficit: 2017-2026,”2016, https://www.cbo.gov/sites/default/files/114th-congress-2015-2016/reports/52142-budgetoptions.pdf

[iii] Oil-related QPAI is attributable to the production, refining, processing, transportation, or distribution of oil or gas, or any primary product from oil or gas. See Internal Revenue Agency, “Form 8903”,2017, https://www.irs.gov/pub/irs-pdf/i8903.pdf

[iv] See for a more complete overview of the DPAD’s legislative history: Congressional Research Service, “The Section 199 Production Activities Deduction: Background and Analysis,”2012, www.taxpayer.net/images/uploads/articles/CRS_Report-The_Section_199_Production_Activities_Deduction.pdf

[v] Ibid.

[vi] See U.S. Code § 199, “Income attributable to domestic production activities,” https://www.law.cornell.edu/uscode/text/26/199

[vii] Lester & Rector (2016) find that 37.2 percent of all positive corporate taxable income is reported as eligible for the section 199 deduction in 2012. See Lester, R. & Rector, R.,”Which Companies Use the Domestic Production Activities Deduction?,”2016, Tax Notes, Vol. 152, No. 9, 2016, https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2837027

[viii] See for similar results for 2012: Progressive Policy Institute, “Anatomy of a Special Tax Break and the Case for Broad Corporate Tax Reform,”2013, https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2541896

[ix] A deduction of 9 percent with a corporate tax rate of 35 percent leads to an effective reduction of 0.09*35% = 3.15%.

[x] U.S. Code § 199 (see endnote 5)

[xi] World Wrestling entertainment, Inc., “Annual report 2016,”2016, http://corporate.wwe.com/~/media/Files/W/WWE/annual-reports/2016.PDF

[xii] The Cheesecake Factory, “Annual report 2016,”2016, http://investors.thecheesecakefactory.com/phoenix.zhtml?c=109258&p=irol-reportsannual

[xiii] See Ryan Grim, “PwC’s Other Debacle: A Tax Boondoggle That Has Ballooned Out Of Control”, March 2017, Huffington Post, http://www.huffingtonpost.com/entry/pwcs-other-debacle-a-tax-boondoggle-that-has-ballooned-out-of-control_us_58b73172e4b023018c6c9852

[xiv] Ibid.

[xv] Ibid.

[xvi] Ibid.

[xvii] Lester, R. & Rector, R. (see endnote 7)

[xviii] Congressional Budget Office (see endnote 2)

[xix] See The Center on Budget and Policy Priorities, “States Can Opt Out of the Costly and Ineffective ‘Domestic Production Deduction’ Corporate Tax Break,”2013, https://www.cbpp.org/research/states-can-opt-out-of-the-costly-and-ineffective-domestic-production-deduction-corporate?fa=view&id=553#_edn1

[xx] Lester, R. & Rector, R. (see endnote 7)

[xxi] Given the different reporting of fiscal years, June 30th is used as cut-off date for every fiscal year. In the case of Microsoft, Oracle and Twenty-first Century Fox this means that we used the 10-K of the last year.

[xxii] Methodological note: The data is gathered by studying the publicly available 10-K’s of all companies included in the fortune 500 list during the period of study. When sufficiently large, companies are required to document their DPAD in their 10-K.

[xxiii] See Appendix I for a more detailed table with numbers for the whole period 2012-2016.

[xxiv] Progressive Policy Institute (see endnote 8)

[xxv] See Lester, R., “Made in the U.S.A? A Study of Frim Responses to Domestic Production Incentives,”2016, Stanford Graduate School of Business, https://www.gsb.stanford.edu/faculty-research/working-papers/made-usa-study-firm-responses-domestic-production-incentives

[xxvi] Lester, R. & Rector, R. (see endnote 7)

[xxvii] See Committee for a Responsible Federal Budget, “The Tax Break-Down: Section 199, the Domestic Production Activities Deduction,”2013, http://www.crfb.org/blogs/tax-break-down-section-199-domestic-production-activities-deduction

[xxviii] Lester, R (see endnote 7)

[xxix] It is even possible that the DPAD stimulates oversees – instead of domestic – job creation. The DPAD could for example increase the demand for some technological services, partly provided by an Indian soft-ware engineer who works for an US tech-company.

[xxx] There are simplified rules for firms with less than $10 and less than $100 million of average annual gross receipts. Internal Revenue Service (see endnote 3)

[xxxi] See Ryan Grim, “PwC’s Other Debacle: A Tax Boondoggle That Has Ballooned Out Of Control”, March 2017, Huffington Post, http://www.huffingtonpost.com/entry/pwcs-other-debacle-a-tax-boondoggle-that-has-ballooned-out-of-control_us_58b73172e4b023018c6c9852

[xxxii] See for a more elaborate discussion of the distorting effects of the DPAD: Congressional Research Service (see endnote 4)

[xxxiii] Progressive Policy Institute (see endnote 8)

[xxxiv] See Rosenberg, D. et al., “The domestic production activities deduction for computer software: Software can qualify for this valuable tax break,” 2015, Journal of Accountancy, http://www.journalofaccountancy.com/issues/2015/mar/computer-software-tax-deduction.html

[xxxv] Congressional Budget Office (see endnote 2)

[xxxvi] See Congressional Research Service, “International Corporate Tax Rate Comparisons and Policy Implications”,2014, https://fas.org/sgp/crs/misc/R41743.pdf

[xxxvii] See The Center on Budget and Policy Priorities, “States Can Opt Out of the Costly and Ineffective ‘Domestic Production Deduction’ Corporate Tax Break,”2013, https://www.cbpp.org/research/states-can-opt-out-of-the-costly-and-ineffective-domestic-production-deduction-corporate?fa=view&id=553#_edn1

[xxxviii] Committee for a Responsible Federal Budget (see endnote 27)

[xxxix] The Joint Committee on Taxation, “Description Of Certain Revenue Provisions Contained In The President’s Fiscal Year 2015 Budget Proposal,”2014, https://www.jct.gov/publications.html?func=startdown&id=4682

[xl] Committee for a Responsible Federal Budget (see endnote 27)

[xli] Ibid.