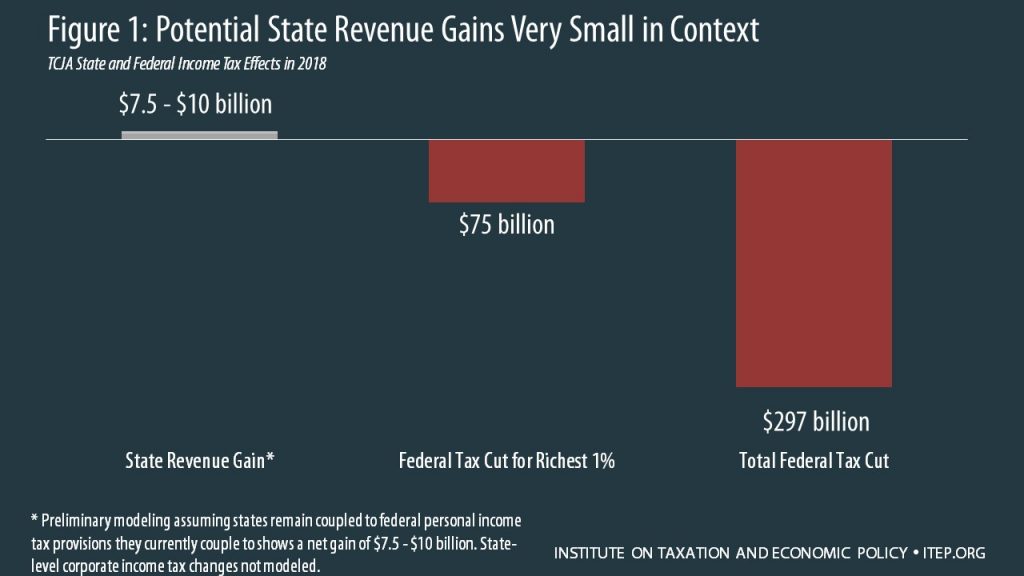

This post is the third in a series of what we’re watching in state tax policy during 2018 legislative sessions. The first post discussed state responses to federal tax cuts and the second focused on state revenue shortfalls.

This has been a big year for state action on tax credits that support low-and moderate-income workers and families. And this makes sense given the bad hand low- and middle-income families were dealt under the recent Trump-GOP tax law, which provides most of its benefits to high-income households and wealthy investors.

Many proposed changes are part of states’ broader reaction to the impact of the new federal law on state tax systems. Unfortunately, some of those proposals left much to be desired. While state lawmakers should focus on protecting and enhancing revenues in the face of federal funding cuts and protecting their states’ most vulnerable families, states like Idaho and Missouri have rolled family tax credit proposals into larger tax cut packages that are highly problematic overall. Other states, such as Hawaii and New Jersey, are considering needed expansions without taking steps back in other parts of their tax codes.

Steps States Are Taking to Create and Strengthen Child Tax Credits

This year, Idaho joins California, New York, Oklahoma, and to some extent Colorado in offering a state-level Child Tax Credit (CTC). Idaho’s new nonrefundable credit of $205 per child is a step forward for the state, but the overall package in which that improvement was included is far from ideal. A $130 credit passed initially as part of a $200 million tax cut package that reduces the state’s personal income tax rates, benefiting primarily the top 1 percent of taxpayers. Although the legislature later increased the credit from $130 to $205, the proposal still fails to hold harmless larger families with incomes between $39,000 and $200,000.

In Maine, Gov. Paul LePage proposed that a portion of the state’s revenue surplus be earmarked for a child tax credit. The state would eliminate its personal exemption under federal conformity and then use the resulting revenue to provide a nonrefundable credit. This is a welcome benefit for lower- and middle-income families. But unfortunately, it is being proposed alongside misguided tax cuts such as a lower corporate income tax and a larger estate tax exemption.

New Jersey’s governor proposed creating a child and dependent care credit. In New York, a state Senator proposed legislation to expand the state’s dependent care credit by doubling the cap on deductible child care costs. Lawmakers in Minnesota proposed a new personal/dependent credit that phases out for upper-income taxpayers, while retaining the personal exemption. The Wisconsin legislature passed a one-time $100 child tax credit and in an odd coupling, with a sales tax holiday. Bills in Missouri would create a nonrefundable child tax credit. And an Arizona bill for a $250 per child credit, to be funded with revenue from the federal law changes, made some headway before being voted down.

State Actions to Create and Strengthen Earned Income Tax Credits

EITCs have been on the minds and policy agendas of governors in California, Massachusetts, Minnesota, Missouri, New Jersey, and Vermont this year. California’s Gov. Jerry Brown declared an EITC Awareness Week to help promote the state’s recently expanded credit. Gov. Charlie Baker of Massachusetts proposed increasing the state’s EITC from 23 to 30 percent. In Minnesota, Gov. Mark Dayton’s tax plan includes an expansion of the state’s Working Family Tax Credit—extending the credit to more low- and middle-class families, more dependents, and recipients beginning at 21 years of age. Missouri Gov. Eric Greitens’s proposed tax cuts for the wealthy, which would slash the top rate of the personal income tax and lower the corporate income tax rate, would also include the creation of a 20 percent nonrefundable state-level EITC. Gov. Phillip Murphy of New Jersey unveiled a budget proposal that, among other positive progressive steps, would raise the state’s EITC to 40 percent of the federal credit. And Vermont Gov. Phil Scott, in a larger restructuring of Vermont’s tax system, has proposed increasing the state’s EITC from 32 to 35 percent of the federal credit.

Lawmakers in a range of other states also have been looking for ways to improve and promote this highly-effective anti-poverty tool. Maryland lawmakers are considering expanding the state’s EITC to individuals without qualifying children and lowering the age of eligibility. Michigan lawmakers introduced legislation to expand the state’s EITC from 6 to 30 percent of the federal credit in response to federal conformity. A bill in Nebraska would increase the state’s refundable EITC from 10 to 12 percent. And in a more targeted approach, Utah lawmakers proposed a 10 percent EITC for those experiencing “intergenerational poverty.” That proposal passed the House and Senate Revenue and Taxation Committee but did not make it out of the Senate.

Bills in Hawaii and Oklahoma would make these states’ credits refundable. Hawaii’s EITC, enacted just last year, is currently set at 20 percent of the federal credit. But the nonrefundability of the credit limits its value for those Aloha State families most in need. While exploring revenue-raising proposals, Oklahoma lawmakers considered restoring refundability to the state’s EITC to protect low-income workers, but no agreement has been reached.

Advocacy for EITCs is strong in other parts of the country as well. Supporters of the credit in Indiana and Virginia are pushing to increase their EITC and make it fully or partially refundable. State groups in Arkansas, Georgia, and West Virginia—to name a few—continue to promote the benefits of EITCs and push for their creation to bolster the earnings of low-wages workers and provide them with an opportunity to move up and out of poverty toward meaningful economic security.

Federal Impact on Low-Income Credits

The Trump-GOP tax law made temporary changes to the federal Child Tax Credit (CTC) that are set to expire in 2026, however the lowest-income families with children were largely left behind from this expansion.

For the CTC, the amount made available per qualifying child increased from $1,000 to $2,000, the law raised the refundable portion of the credit to $1,400, lowered the earned income threshold from $3,000 to $2,500, and increased the credit phaseout from $75,000 to $200,000 of AGI for single filers and from $110,000 to $400,000 for joint filers. Unfortunately, these provisions prevent low-income families from fully accessing the CTC. Many of the lowest-income working families will see a mere increase of less than $75. Others will fare a bit better but will not get the full $1,000 per child increase that higher-income families are now eligible to receive. As a result, it is now more important than ever for states to take action to protect those that have been left behind from the federal change.

The federal EITC was largely left unchanged, but is now linked to a less generous inflation adjustment based on the Chained Consumer Price Index (chained-CPI). In addition to gradually pushing taxpayers into higher income tax brackets, chained-CPI will make the EITC, and other breaks, less generous over time.