Over the next few weeks we will be blogging about what we’re watching in state tax policy during 2018 legislative sessions. And there is no trend more pervasive in states this year than the need to sort through and react to the state-level impact of federal tax changes enacted late last year. All states are affected to some extent and virtually every state must make crucial decisions this year about whether to “couple to” the federal tax changes, how much to rely on the federal tax code going forward, and how to maintain adequate services in the face of impending federal funding cuts and other challenges. In future blogs we’ll cover many more topics, including tax cuts and shifts, progressive revenue raising efforts, state revenue shortfalls and solutions, infrastructure funding, and more.

The federal tax-cut bill (the Tax Cuts and Jobs Act, or TCJA) enacted in late 2017 has major ramifications for state fiscal policy, which we detailed here. And as we urged here, state lawmakers should focus their responses on protecting and enhancing revenues in the face of federal funding cuts, mitigating rather than exacerbating the TCJA’s deeply regressive tax effects, avoiding the temptation of trickle-down economics and Kansas-style tax competition, and taking a long-run view for the good of their state residents.

This week, lawmakers in both Georgia and Idaho unfortunately passed legislation that eschews sound policy guidance in favor of scoring anti-tax political points and blindly following long-debunked trickle-down economic maxims. But these two states are in the minority, as most states continue to debate the implications of the TCJA and still have time to craft effective policy responses.

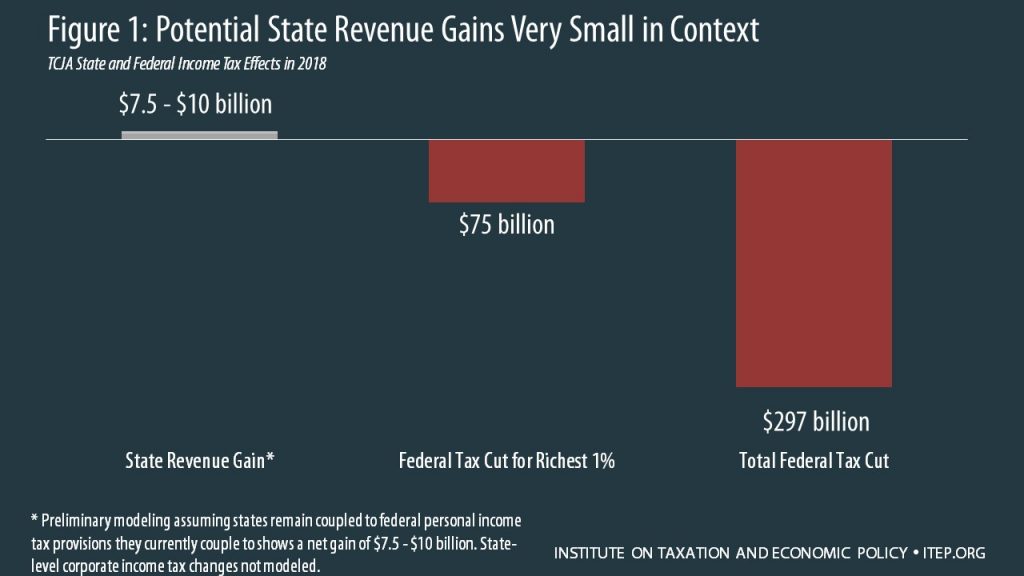

States already face budget shortfalls, underfunded services, inadequate savings, and tax codes tilted to favor the wealthy over average families. These issues have only deepened under the TCJA, which sent a clear message of reduced federal commitment to the goals of growing the economy for all, protecting democratic values from the threat of increasingly concentrated wealth and power, and investing in public goods like schools, safety, and infrastructure. States do have important questions to answer about the specific ways in which their tax codes are affected by the federal changes, but the key question remains: as the federal government steps down in these areas, will states step up to push back against spiraling inequality and raise the revenue needed to provide quality public services? Or will they choose another path, focusing on smaller or more peripheral issues – or worse, doubling down on the destructive aspects of the TCJA? Below we update on the general trends and specific policies as states sort through these questions.

Stepping Up to The Challenge

Some state advocates and policymakers are pushing for progressive state revenue changes designed to offset rather than exacerbate the regressive and/or budget-busting effects of the TCJA.

A California bill, for example, would add a surcharge on highly profitable corporations with the specific goal of tapping into a portion of their federal tax savings under the TCJA.

Policymakers in New York, at both the city and state level, have also noted the TCJA’s favoritism toward millionaires and focused on those wealthy beneficiaries for income tax increases.

In New Jersey, too, Gov. Phil Murphy is pointing out that the TCJA’s massive tax cuts on wealthy households are all the more reason to proceed with a millionaire’s tax to help address the state’s fiscal woes.

And though they are unlikely to pass this year, even the generally anti-tax legislature in Nebraska considered multiple bills to raise taxes on the wealthy beneficiaries of the TCJA.

Standing Up for Low- and Middle- Income Families

One unfortunate consequence of the TCJA in many states is the potential elimination of state personal exemptions, which serve to make the first few thousand dollars of a family’s income tax-free and are particularly important to low- and middle-income families, whose federal tax savings from the TCJA are generally meager and temporary. Advocates and lawmakers in several states have rightly stood up to at least ensure that these people are not asked to pay more in taxes.

In Maryland, although there is still debate about making more sweeping tax changes that could end up tilted to high-income households, the one thing legislators have found easy to agree on is preserving the state’s personal exemption.

Two bills in Nebraska aim to directly respond to the TCJA’s effects on Nebraskans by preserving the state’s personal exemption credit that would otherwise be eliminated.

Proposals in Maine have taken a different approach, which would allow the personal exemption to be eliminated but use the resulting revenue to deliver a more targeted refundable credit such as an Earned Income Tax Credit or Child Tax Credit that would be even more helpful to lower-income families.

Where legislative will is lacking, advocates have done their best to hold lawmakers’ feet to the fire on these issues, such as these efforts in Idaho.

Stepping Back to Rethink the Tax Code

Some state policymakers have seen all this TCJA chaos as a potential ladder they can use to gain perspective and consider truly fundamental changes to their tax codes.

In Vermont, Gov. Phil Scott has indicated an interest in rebuilding the state’s income tax from the ground up with a whole new structure of rates, deductions, exemptions, and credits.

The TCJA has also changed the conversation in Minnesota, which was originally about closing a revenue shortfall but now may shift to more comprehensive tax reform.

Utah, too, could reconsider its tax code in a big way, as the state’s tax code is closely but complicatedly coupled to federal law.

Taking Bad Federal Ideas and Running with Them

It will come as no surprise that the passage of top-heavy federal tax cuts that resulted in a small bump in state revenues have paved the way for state lawmakers to push for long-desired cuts to state personal and corporate income taxes. Making matters worse, in most of these cases the state-level tax cuts proposed are permanent even though the federal bill largely expires after 2025. That could leave these states in an even deeper revenue hole a few years down the line.

Idaho is a prime example of this approach, as legislators fixated on tax cuts have ignored these growing revenue needs and already sent an income tax cut to Gov. Butch Otter’s desk that will leave the state budget worse off by $100 million per year.

In Georgia, the state’s peculiar relationship to the federal tax code means the TCJA could generate more than $1 billion of state revenue, which could have been devoted to improving the tax code, preparing for federal funding cuts to come, and/or restoring full funding to K-12 schools; instead, lawmakers have passed a bill focused on cutting the top income tax rate and ultimately reducing the funding available for these priorities.

In Iowa, where revenue shortfalls are already routine, the TCJA has brought attention to the state’s regressive and costly deduction for federal income taxes paid; but both Gov. Kim Reynolds’s plan and the leading Senate plan would squander the opportunity for true reform and needed revenue by eliminating the deduction while deeply slashing tax rates.

Missouri doesn’t even anticipate a significant state tax increase resulting from the TCJA, but like in Iowa, the TCJA has highlighted Missouri’s deduction for federal income taxes and both Gov. Eric Greitens and Senate lawmakers are using that as a jumping-off point to push for major regressive income tax rate cuts.

In Michigan, lawmakers considered several approaches that were focused on offsetting any potential tax increases, but some lawmakers successfully pushed for changes that go beyond that call and will ultimately reduce state revenues.

Calls for adding state tax cuts to the federal cuts under the banner of (thoroughly debunked) trickle-down economics can be heard in essentially every state, as these examples from Minnesota and West Virginia demonstrate.

Also, in some cases, lawmakers are considering adopting provisions of the TCJA that they would otherwise not be affected by.

The TCJA’s 20 percent deduction for “pass-through” profits, on which business owners pay personal income tax instead of corporate income tax, would by default only affect a few states that use federal taxable income as their tax calculation starting point, but in Iowa, Gov. Kim Reynolds’s plan would adopt a smaller version of the deduction, and the leading Senate proposal would adopt the entire deduction.

Dancing around the TCJA

Rather than working on how their state will grapple with federal retrenchment in important policy arenas or figuring out how to tweak their tax codes to avoid unfortunate state-level effects of the TCJA, some are preoccupied instead with finding “workarounds” that are meant to reverse the TCJA’s effects on their residents’ federal taxes. These are generally focused on finding ways around the new $10,000 cap on the State and Local Tax (or “SALT”) deduction, which applies to the total of state and local property and income or property and sales taxes.

New York’s proposed move from an income tax to a payroll tax is one such effort, motivated by the fact that payroll taxes will continue to be fully deductible on federal tax returns while income taxes will be subject to the SALT cap.

A similar approach that is catching on in multiple states including California, Connecticut, Illinois, Nebraska, New Jersey, New York, Virginia, and Washington would convert some or all state or local tax payments into fully-federally-deductible “charitable contributions” by allowing taxpayers to “contribute” to a special fund and then receive a dollar-for-dollar credit, which has no net effect on revenues but circumvents the SALT cap.

The final tactic a few states – Connecticut, Maryland, New Jersey, and New York so far – are using is to sue the federal government in an attempt to overturn the TCJA, though few expect the lawsuit to be successful.