Read as PDF (Includes Full Appendix of State-by-State data)

Go to State by State Data

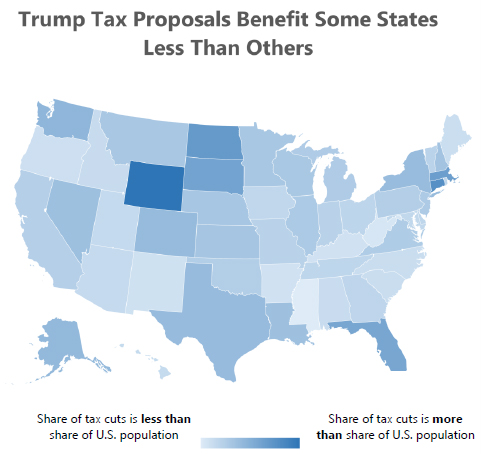

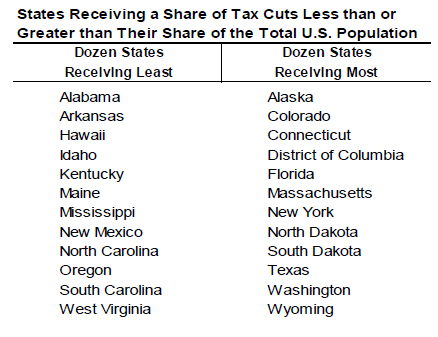

The broadly outlined tax proposals released by the Trump administration would not benefit all taxpayers equally and they would not benefit all states equally either. Several states would receive a share of the total resulting tax cuts that is less than their share of the U.S. population. Of the dozen states receiving the least by this measure, seven are in the South. The others are New Mexico, Oregon, Maine, Idaho and Hawaii.

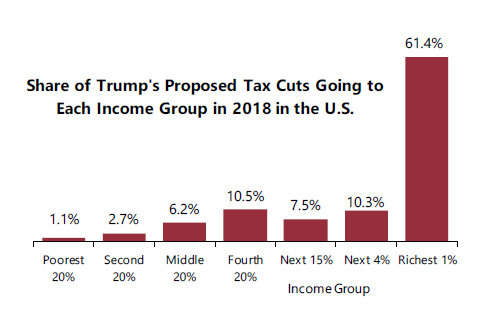

As the state-specific versions of this report explain, taxpayers within each state do not benefit equally from the Trump tax proposals either. Nationally, the richest one percent of taxpayers in America, who all will have an income of at least $599,300 in 2018, would receive 61.4 percent of the tax cuts that result from Trump’s proposals.

As the state-specific versions of this report explain, taxpayers within each state do not benefit equally from the Trump tax proposals either. Nationally, the richest one percent of taxpayers in America, who all will have an income of at least $599,300 in 2018, would receive 61.4 percent of the tax cuts that result from Trump’s proposals.

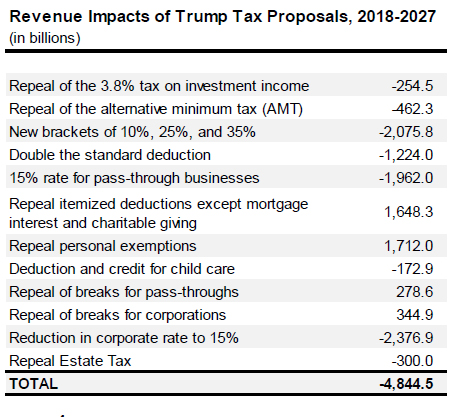

The figures in this report have been calculated by the Institute on Taxation and Economic Policy (ITEP) based on the broad principles for tax reform released by the Trump administration on April 26 and based on subsequent statements of administration officials. Because the principles and statements left many unanswered questions, the estimates required some assumptions, which are spelled out in this report. Based on what is known now about these proposals, ITEP estimates that together they would reduce total federal revenue by at least $4.8 trillion over ten years.

The costs could be much higher, as explained further on.

Tax Cuts Mostly Aimed at High-Income Households

Officials in the Trump administration have said that their plan will help the middle-class, and that there would be “no absolute tax cut for the wealthy,”[1] but that is not true of the proposals they have put forward so far.

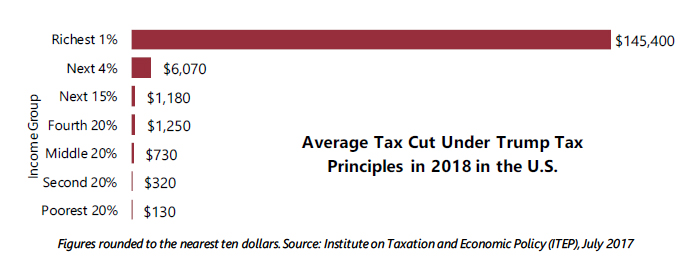

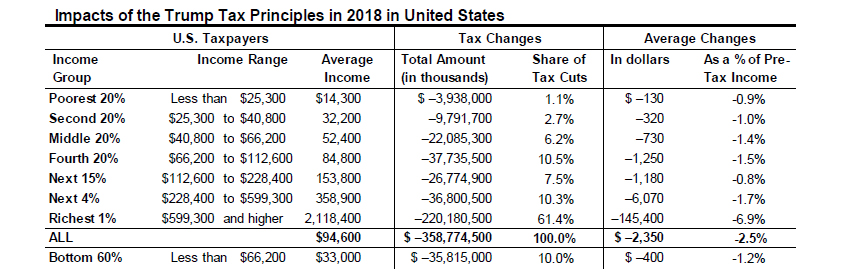

Americans who fall within the middle fifth of taxpayers on the income ladder, who are quite literally the “middle-class,” would receive just 6.2 percent of the tax cuts in 2018. They would receive an average tax cut of $730, which is tiny compared to the average $145,400 received by the richest one percent in 2018 alone.

The average income of the middle fifth of taxpayers is projected to be $52,400 in 2018. The average income of the richest one percent of taxpayers is projected to be $2.1 million.

The bottom three fifths of taxpayers (the poorest 60 percent of taxpayers) will all make less than $66,200 in 2018. This 60 percent of America will receive just 10 percent of the tax cuts in 2018, compared to the 61.4 percent received by the richest one percent of taxpayers.

Even as a Percentage of their Massive Income, the Richest One Percent Get the Biggest Tax Cuts

Some might mistakenly believe that the tax cuts are evenly distributed when measured as a percentage of taxpayers’ income. For example, could one argue that the average $730 tax cut received by the middle fifth of taxpayers is fairly significant relative to their income level?

Not according to the numbers. Even measured as a share of income, the tax cuts for the rich are far bigger than the tax cuts for everyone else. The richest one percent would receive tax cuts equal to 6.9 percent of their income in 2018. The bottom 60 percent of taxpayers would receive tax cuts equal to just 1.2 percent of their income.

Some Low- and Middle-Income Americans Would Receive a Tax Increase Under Trump’s Proposals

Among those Americans who find themselves in the middle 20 percent of taxpayers in 2018, 14 percent would pay higher taxes that year under Trump’s proposals. (The number with tax increases could be larger if Congress and the President eventually include more provisions to raise revenue.)* For these households, the effect of the Trump proposals to raise taxes would be greater than those that reduce taxes. There are two main proposals in the package that would raise revenue. The first is the repeal of the personal exemptions taxpayers claim for each family member. Larger families might be particularly affected by this. The second is the repeal of all itemized deductions except those for charitable giving and home mortgage interest. The biggest deduction repealed would be the deduction for state and local taxes. This would particularly affect those taxpayers living in states with higher state and local taxes.

A small portion of the tax increases would also be specific to moderate-income business owners. One of the proposals would tax “pass-through” income (income from businesses that do not pay the corporate income tax) at a rate of just 15 percent. The majority of this income goes to wealthy individuals who currently pay a marginal tax rate higher than 15 percent and who would therefore benefit a great deal from this change. But some moderate-income business owners who are now in the 10 percent income tax bracket would actually pay more under this proposal. A literal reading of the proposal leads one to conclude that all of this type of business income would be taxed at 15 percent, which would be a tax increase for those who currently pay at a marginal rate of 10 percent.

*For example, the Tax Policy Center (TPC) estimated that of those who find themselves in the middle-fifth of taxpayers, almost 24 percent would face a tax increase in 2018 under Trump’s tax proposals. This is because TPC included several additional revenue-raising provisions that Trump might eventually include in his proposals, such as repealing the “head of household” filing status, which benefits single parents. See Tax Policy Center, “The Implications of What We Know and What We Don’t Know about President Trump’s Tax Plan,” July 12, 2017. http://www.taxpolicycenter.org/publications/implications-what-we-know-and-dont-know-about-president-trumps-tax-plan

Price Tag of Plan Would Mean Cuts in Public Investments Low- and Middle-Income People Rely On

Trump’s tax proposals would cost at least $4.8 trillion over ten years. In the short-run this might just mean higher government deficits, but eventually Congress and the President would almost surely have to cut major programs like Medicare, Medicaid, food assistance and others to offset the costs. This reality is reflected in the draconian cuts from programs for low- and moderate-income people that the Trump administration recently proposed in its budget.[2] Low- and middle-income families would probably lose far more as a result than they gain from the small tax cuts President Trump would provide them.

Different Impact Among States

Often when tax cuts are proposed that mainly benefit the rich, states with more rich people logically receive a greater share of the tax cuts than others. This picture is somewhat more complicated for this particular package of tax proposals because it includes repeal of the deduction for state and local taxes. Some of the states with a disproportionate share of high-income residents are also those with higher state and local taxes, which would no longer be deducted from taxable income when calculating federal income taxes under this proposal.

Often when tax cuts are proposed that mainly benefit the rich, states with more rich people logically receive a greater share of the tax cuts than others. This picture is somewhat more complicated for this particular package of tax proposals because it includes repeal of the deduction for state and local taxes. Some of the states with a disproportionate share of high-income residents are also those with higher state and local taxes, which would no longer be deducted from taxable income when calculating federal income taxes under this proposal.

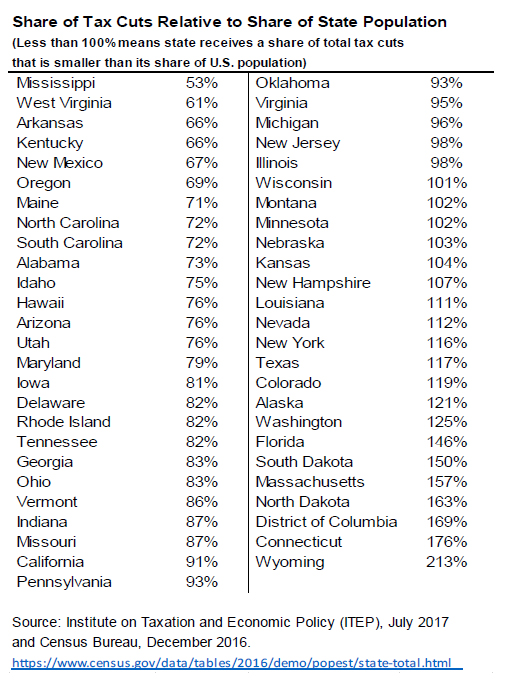

But it is still the case that many poorer states would receive a share of the total tax cuts that is less than their share of the total U.S. population, as illustrated in the nearby table. See the appendix for the complete list of states and their share of the total tax cuts relative to their share of the U.S. population.

The Trump Tax Proposals Included in These Figures

This report assumes that the Trump administration’s tax plan includes the proposals described on a single page that it released on April 26.[3] In places where those proposals are vague and assumptions must be made about the details, this report assumes that they generally follow the contours of similar proposals made by Trump during his presidential campaign. For example, the April 26 release includes “Providing tax relief for families with child and dependent care expenses.” Because no other details are given about this particular proposal, this report assumes that it would be the same as the child and dependent care breaks that Trump included in the last tax plan he released as a presidential candidate.

This report assumes that the Trump administration’s tax plan includes the proposals described on a single page that it released on April 26.[3] In places where those proposals are vague and assumptions must be made about the details, this report assumes that they generally follow the contours of similar proposals made by Trump during his presidential campaign. For example, the April 26 release includes “Providing tax relief for families with child and dependent care expenses.” Because no other details are given about this particular proposal, this report assumes that it would be the same as the child and dependent care breaks that Trump included in the last tax plan he released as a presidential candidate.

This report also includes one proposal, repeal of personal exemptions, that was not clearly spelled out in the April 26 release but was confirmed by statements by administration officials afterwards, as explained further on.

Repeal of the 3.8 Percent Tax on Investment Income

The net investment income tax (NIIT) was enacted as a part of the Affordable Care Act to help finance the costs of expanding health insurance coverage. It applies at a rate of 3.8 percent to investment income for those with income in excess of $200,000 (or $250,000 in the case of a married couple).

The idea behind the NIIT was to ensure that people who largely live off of investment income pay a tax to support health care just as wage-earners pay the Medicare tax on earned income.

The estimate shown here for repeal of the NIIT is somewhat larger than other estimates due to different assumptions about how people with capital gains (a significant component of investment income) respond to different tax rates.[4]

Repeal of the Alternative Minimum Tax

The alternative minimum tax (AMT) is a backstop tax meant to ensure that relatively well-off people pay at least some federal income taxes no matter how many special breaks they claim. In theory, the tax system could be simplified and special breaks and loopholes could be eliminated so that there is no need for the AMT. However, some wealthy taxpayers would pay little or nothing in income taxes if repeal of the AMT is not coupled with elimination of the many special breaks and loopholes that it limits. Donald Trump himself paid substantial AMT in 2005 and would have paid almost nothing in federal income taxes that year if not for the AMT.[5]

New Tax Brackets of 10 Percent, 25 Percent, and 35 Percent

Trump’s proposal would replace the seven income tax brackets in place now with three brackets. Most taxable income would be taxed at rates of 10 percent, 25 percent and 35 percent. Taxable income that takes the form of capital gains or stock dividends would be subject to lower rates in each bracket, as they are now. The rates for capital gains and dividends would be 0 percent, 15 percent and 20 percent. The lower income tax rates for capital gains and dividends provide the most regressive break in the tax code, but Trump would maintain it.[6]

The proposals released on April 26 did not specify the level of taxable income where each bracket begins, so this report assumes that brackets would be structured like those proposed in Trump’s campaign tax plan, with annual adjustments for inflation.

Some of the greatest beneficiaries of this new rate structure are high-income people who are currently in the 39.6 percent income tax bracket and would save substantially from having their marginal tax rate reduced from 39.6 percent to 35 percent.

Double the Standard Deduction

When calculating their taxable income, taxpayers are allowed to deduct amounts that Congress has decided should not be included in determining how much income is available to pay taxes and expenses that Congress has decided to subsidize through the tax code for other policy reasons. Most of these deductions are the “itemized” deductions. However, taxpayers are also allowed to instead claim a standard deduction. Most taxpayers, particularly those who are not wealthy, claim the standard deduction because they are eligible to claim little or nothing in itemized deductions.

In other words, the standard deduction reduces the amount of income on which low- and middle-income people must pay taxes. Doubling the standard deduction, as Trump proposes, would therefore benefit many working people. But as this report explains, the other tax cuts in this package of proposals that disproportionately benefit the wealthy far outweigh those benefiting everyone else.

15 Percent Rate for Pass-Through Businesses

Business that do not pay the corporate income tax are often called “pass-through” businesses, the idea being that the income is passed through to the owners and reported on their personal income tax form. Sometimes pass-through companies are mistakenly characterized as small businesses. The truth is that many law firms, hedge funds, and even huge companies like Bechtel are structured as pass-through companies.[7] It’s also the case that the owners of pass-throughs who receive most of their profits are mostly, but not entirely, high-income individuals. One of Trump’s proposals is to provide a special tax rate of just 15 percent for this income. According to ITEP’s estimates, 79 percent of the benefits of this proposal would go to the richest one percent of taxpayers in 2018.

This proposal could cost far more than is estimated here because highly compensated individuals could respond to the change by routing their income through pass-through entities to take advantage of the lower rate. For example, if John Smith is the CEO of ACME and is paid a salary of $10 million a year, that salary would be subject to the top income tax rate of 35 percent under Trump’s proposals. Smith could instead form a new pass-through entity called John Smith Services, which contracts with ACME to provide management services. Instead of receiving a salary from ACME, Smith would receive pass-through income that would be taxed at just 15 percent.

Repeal Itemized Deductions Except Those for Mortgage Interest and Charitable Giving

The April 26 release of Trump’s tax proposals include two lines that are particularly vague.

“Eliminate targeted tax breaks that mainly benefit the wealthiest taxpayers.”

“Protect home ownership and charitable tax deductions.”

Together, these appear to mean that Trump would include a proposal in the tax plan released by House Republicans last summer to repeal all itemized deductions other than those for mortgage interest and charitable giving.

The most significant of the deductions that would be repealed is the deduction for state and local taxes. It is not immediately obvious how the argument for repealing this deduction could be stronger than the argument for repealing the other two. Since the amount of state and local taxes paid is something that an individual has little or no control over, subtracting them from income arguably helps calculate how much income is actually available to pay federal taxes. In other words, the deduction for state and local taxes is arguably more justified than other deductions, but Trump proposes to repeal it.

Repeal Personal Exemptions

Repeal of personal exemptions was not spelled out on the April 26 release but was confirmed by administration officials shortly afterwards. During the release and in the days following, National Economic Council Director Gary Cohn said several times that families would not pay any income tax on their first $24,000 of income. [8] One of the Trump proposals released on April 26 is to double the standard deduction, which would bring it to a little more than $24,000. This seems to mean that personal exemptions, which further reduce taxable income, would no longer be available. Repeal of the personal exemption was part of the Trump campaign tax plan and therefore appears to be included in the current package of proposals.

Deduction and Credit for Child Care

Because the proposals released on April 26 do not explain what is meant exactly by “Providing tax relief for families with child and dependent care expenses,” this report assumes it refers to the child care tax breaks proposed as part of the Trump campaign tax plan.

During the campaign, Trump proposed an above-line-deduction (a deduction that can be claimed even by taxpayers claiming the standard deduction) to help pay child care expenses. His plan explained that “All but the wealthiest Americans will be able to take an above-the-line deduction for children under age 13 that will be capped at state average for age of child, and for eldercare for a dependent. The exclusion will not be available to taxpayers with total income over $500,000 Married-Joint /$250,000 Single.”

Trump also proposed that “The child care exclusion would be provided to families who use stay-at-home parents or grandparents as well as those who use paid caregivers, and would be limited to 4 children per taxpayer.”

The language seems to mean that a family who has a child in daycare can deduct their actual child care costs, up to the average child care costs in their state based on the age of their children. However, a family with a stay-at-home parent is allowed to take a deduction as well, but since such a family has no actual child care expenses, it is assumed that they would simply deduct an amount equal to the average child care cost in their state based on the age of their children.

Based on a literal reading of the proposal, for families without a stay-at-home parent, the deduction would be limited to actual child care expenses but “capped” at average child care expenses (based on the state of residence and the age of their child), meaning they could deduct nothing at all if they receive free child care from a family member. Meanwhile families with a stay-at-home parent (who tend to be better-off) apparently receive a deduction equal to average child care expenses (based on the state of residence and the age of their child). This is a bizarre result but follows from a literal reading of the proposal.

The proposal also includes a tax credit, described as an addition to the Earned Income Tax Credit (EITC) to help cover child care costs for those families too poor to benefit from the deduction. This credit would be available to single parents with income below $31,200 and married parents with incomes below $62,400. The credit amount would be too low to make child care noticeably more affordable, at a rate of 7.65 percent of the cost of child care or half of the payroll taxes paid by the taxpayer, whichever is less (and based on the parent with lower earnings in a two-parent household).

The strict limits on this break explain why it is estimated to have a small revenue impact (relative to the other proposals) and why it is unlikely to make child care significantly more affordable for families who struggle the most to pay for it. On the other hand, it is difficult to know how people might respond to the strange rules in a way that might have an impact on how much the proposal costs. For example, would some working parents in two-parent families actually drop out of the workforce in order to get a better deduction?

Repeal Breaks for Pass-Through Businesses and Corporations

The Trump administration’s April 26 release said that business tax reform would “eliminate tax breaks for special interests.” No specific tax breaks were listed. For this analysis, ITEP assumes that all tax credits for both pass-through businesses and C corporations (corporations that pay the corporate income tax) would be repealed. It also assumes that the deduction for domestic manufacturing would be repealed.

This interpretation gives Congress and the President considerable credit that they will, in fact, eliminate many tax breaks that have proven very popular for lawmakers and the lobbyists who are in contact with them. The more likely scenario may be that lawmakers are not able to agree on any such list of revenue-raising provisions, in which case the overall package of changes would be costlier and would provide even larger tax breaks to high-income households.

Reduce the Corporate Tax Rate to 15 Percent

In addition to including a 15 percent rate for all businesses in his April 26 proposal, Trump has stated that the tax rate for corporations specifically is too high. During his address to Congress on February 28, he claimed that America’s corporate income tax rate of 35 percent is the highest in the world, making our companies unable to compete.

But the effective tax rate paid by American corporations (the share of profits actually paid in taxes) is far less than 35 percent because of special breaks and loopholes in the tax code.

A 2016 study produced by the Government Accountability Office found that the effective tax rate paid by large profitable American corporations from 2008 through 2012 was just 14 percent. It found that the share of these corporations paying no federal income tax at all was 19.5 percent in 2012 and 24.1 percent in 2011.[9]

A recent study from ITEP examines a particularly profitable group of corporations – the Fortune 500 corporations that were profitable each year from 2008 through 2015. Even among these super-profitable companies, there were several with effective tax rates that were close to zero or below zero for the eight-year period.[10]

In other words, there seems to be little justification for reducing the corporate income tax rate to 15 percent, which is the costliest of Trump’s tax proposals.

Corporate Taxes Mainly Impact High-Income Households

All taxes are paid by people. This includes the corporate income tax even though it is paid directly by corporations. The corporate income tax reduces dividends that companies can pay to shareholders and affects the value of other business assets. This means that the owners of stocks and other business assets ultimately bear most of the tax.

Advocates of corporate tax cuts often claim that the corporate income tax is ultimately borne by workers who lose employment or wages because, the argument goes, the tax causes investment to go offshore. However, corporations are lobbying heavily to reduce the corporate income tax, and it seems unlikely that they would do so if they did not believe that their shareholders were ultimately bearing the tax.

The Congressional Budget Office and the Treasury Department have stated that they believe the vast majority of the corporate income tax is borne ultimately by the owners of corporate stocks and other business assets. The ownership of these assets is concentrated among the wealthiest households, which makes the corporate income tax a progressive tax. For this study, ITEP assumes that the distribution of the corporate tax is as the Congressional Budget Office most recently estimated, with about 47 percent of the tax borne by the richest one percent of taxpayers and about 63 percent of the tax borne by the richest five percent of taxpayers.* These groups would therefore receive the primary effect of either raising or lowering the corporate tax.

*Congressional Budget Office, “The Distribution of Household Income and Federal Taxes, 2013,” June 2016. www.cbo.gov/publication/51361

Repeal the Estate Tax

The federal estate tax is paid only on the largest estates that are passed from one generation to the next. In 2017, a married couple could leave to their heirs an estate worth at least $11 million and no tax would be collected on it. Usually even larger estates avoid the tax because charitable bequests and certain other amounts are not included in the taxable estate. As a result, only about 0.2 percent — that’s two-tenths of one percent — of deaths result in estate tax liability.[11]

The Joint Committee on Taxation estimated that if the estate tax is repealed, more than 70 percent of the benefits would go to families with estates worth more than $20 million.[12]

Changes to International Corporate Tax Rules

Another Trump proposal would adopt a “territorial” tax system, which means the offshore profits of American corporations would be exempt from U.S. taxes. This report does not include estimates for this proposal because they are highly uncertain, but it is very likely that the result would be greater offshore corporate tax avoidance and thus a reduction in tax revenue.

Under current rules, American corporations are already allowed to “defer” paying U.S. taxes on profits that they report earning offshore. This has created an incentive for corporations to use accounting gimmicks to characterize profits earned in the U.S. or other countries where they do business as earned in countries with a very low corporate tax or no corporate tax at all. By effectively shifting profits to these offshore tax havens, corporations defer paying much of anything on their profits for decades, possibly forever.

We know that American corporations engage in these accounting gimmicks because the profits they report to the IRS that they have earned in low-tax countries are impossible. For example, American corporations reported that their subsidiaries in the Cayman Islands earned a total of $46 billion, but this is impossible because that tiny country’s entire economic output that year was only $3 billion.[13]

Shifting to a territorial system would only increase the rewards for this type of offshore profit-shifting. Whereas the current system allows corporations to defer paying taxes on profits they characterize as having been generated offshore, a territorial system would completely exempt profits they characterize as having been generated offshore.

Largely because of deferral and techniques used to take advantage of it, American corporations today are officially holding $2.6 trillion in profits offshore. In many cases this money is “offshore” only as an accounting matter, but the result is that U.S. taxes are not paid on it.

Another of Trump’s proposals would transition to the territorial system by imposing a one-time tax on this $2.6 trillion that corporations hold offshore right now. There would be no further U.S. tax on these profits.

The proposal does not specify what the rate would be, but during the campaign he proposed a one-time tax on these offshore profits at a rate of ten percent. In the long-run, this would be a significant break for corporations that otherwise would have to pay the full U.S. corporate tax rate on these profits. The proposal would raise revenue in the short-run, but because this is only a temporary, one-time impact, it is not included in the estimates for this report.

Appendix I: States Ranked by Share of Tax Cuts Relative to Population

Appendix II: State-by-State Figures

Click to see the distribution for taxes in your state:

End Notes

[1] Bloomberg, “‘Mnuchin Rule’ Against Wealthy Tax Cuts Comes Back to Bite Him,” May 25, 2017. https://www.bloomberg.com/news/articles/2017-05-25/-mnuchin-rule-against-wealthy-tax-cuts-comes-back-to-bite-him

[2] Center on Budget and Policy Priorities, “Trump Budget Gets Three-Fifths of Its Cuts From Programs for Low- and Moderate-Income People,” May 30, 2017. https://www.cbpp.org/research/federal-budget/trump-budget-gets-three-fifths-of-its-cuts-from-programs-for-low-and

[3] CNN, “The 1-Page White House Handout on Trump’s Tax Proposal,” April 26, 2017. http://www.cnn.com/2017/04/26/politics/white-house-donald-trump-tax-proposal/index.html

[4] The Joint Committee on Taxation and the Congressional Budget Office assume that investors will sell fewer assets, meaning there will be fewer capital gains to tax, when taxes are increased on capital gains, and vice versa when taxes on capital gains are lowered. The Congressional Research Service has written that this behavioral effect probably does exist but is likely to be smaller than the effect assumed by JCT and CBO. The estimates in this report assume that changes in taxes on capital gains have effects that are in line with what the Congressional Research Service has found. The method used to calculate these effects and incorporate them into the cost estimates is described in Citizens for Tax Justice, “Policy Options to Raise Revenue,” March 8, 2012. http://ctj.org/ctjreports/2012/03/policy_options_to_raise_revenue.php

[5] Jim Zarroli, “In 2005, Trump was Hit with a Tax that He Now Wants to Abolish,” NPR, March 15, 2017. http://www.npr.org/sections/thetwo-way/2017/03/15/520276847/in-2005-trump-was-hit-with-a-tax-that-he-now-wants-to-abolish

[6] In 2013, the Congressional Budget Office found that 68 percent of the benefits of the lower tax rate for capital gains and stock dividends went to the richest one percent of taxpayers, making it by far the tax break most focused on the richest Americans. Congressional Budget Office, “The Distribution of Major Tax Expenditures in the Individual Income Tax System,” May 29, 2013. http://cbo.gov/publication/43768

[7] Graham Bowley, “In Tax Overhaul Debate, Large vs. Small Companies,” New York Times, May 23, 2013. http://www.nytimes.com/2013/05/24/business/in-tax-overhaul-debate-its-large-vs-small-companies.html

[8] Gary Cohn, National Economic Council Director, speaks to “CBS This Morning”: Full transcript, May 1, 2017, http://www.cbsnews.com/news/gary-cohn-national-economic-council-director-speaks-to-cbs-this-morning-full-transcript/; Julia Limitone, “Gary Cohn: Trump Wants Washington Out of Middle Class Pockets,” Fox Business News, April 28, 2017, http://www.foxbusiness.com/politics/2017/04/28/gary-cohn-trump-wants-washington-out-middle-class-pockets.html; Briefing by Secretary of the Treasury Steven Mnuchin and Director of the National Economic Council Gary Cohn, April 26, 2017, https://www.whitehouse.gov/the-press-office/2017/04/26/briefing-secretary-treasury-steven-mnuchin-and-director-national.

[9] Government Accountability Office, “Most Large Profitable U.S. Corporations Paid Tax But Effective Tax Rates Differed Significantly from the Statutory Rate,” GAO-16-363, April 13, 2016, http://www.gao.gov/products/GAO-16-363

[10] Matthew Gardner, Robert S. McIntyre and Richard Phillips, “The 35 Percent Corporate Tax Myth: Corporate Tax Avoidance by Fortune 500 Companies, 2008 to 2015,” March 2017, https://itep.org/the-35-percent-corporate-tax-myth/.

[11] Institute on Taxation and Economic Policy, “The Federal Estate Tax: A Critical and Highly Progressive Revenue Source.” December 7, 2016. https://itep.org/the-federal-estate-tax-a-critical-and-highly-progressive-revenue-source/

[12] Memorandum from Thomas A. Barthold, Joint Committee on Taxation, March 24, 2015. https://democrats-waysandmeans.house.gov/sites/democrats.waysandmeans.house.gov/files/documents/114-0191.pdf

[13] Citizens for Tax Justice, “American Corporations Tell IRS the Majority of Their Offshore Profits Are in 10 Tax Havens,” April 7, 2016. http://ctj.org/ctjreports/2016/04/american_corporations_tell_irs_the_majority_of_their_offshore_profits_are_in_10_tax_havens.php