The recently enacted Tax Cuts and Jobs Act (TCJA) has major implications for budgets and taxes in every state, ranging from immediate to long-term, from automatic to optional, from straightforward to indirect, from certain to unknown, and from revenue positive to negative. And every state can expect reduced federal investments in shared public priorities like health care, education, public safety, and basic infrastructure, as well as a reduced federal commitment to reducing economic inequality and slowing the concentration of wealth. This report provides detail that state residents and lawmakers can use to better understand the implications of the TCJA for their states and take this opportunity to improve the adequacy and fairness of their tax codes.

Most States’ Taxes Are Linked to Federal Tax Law

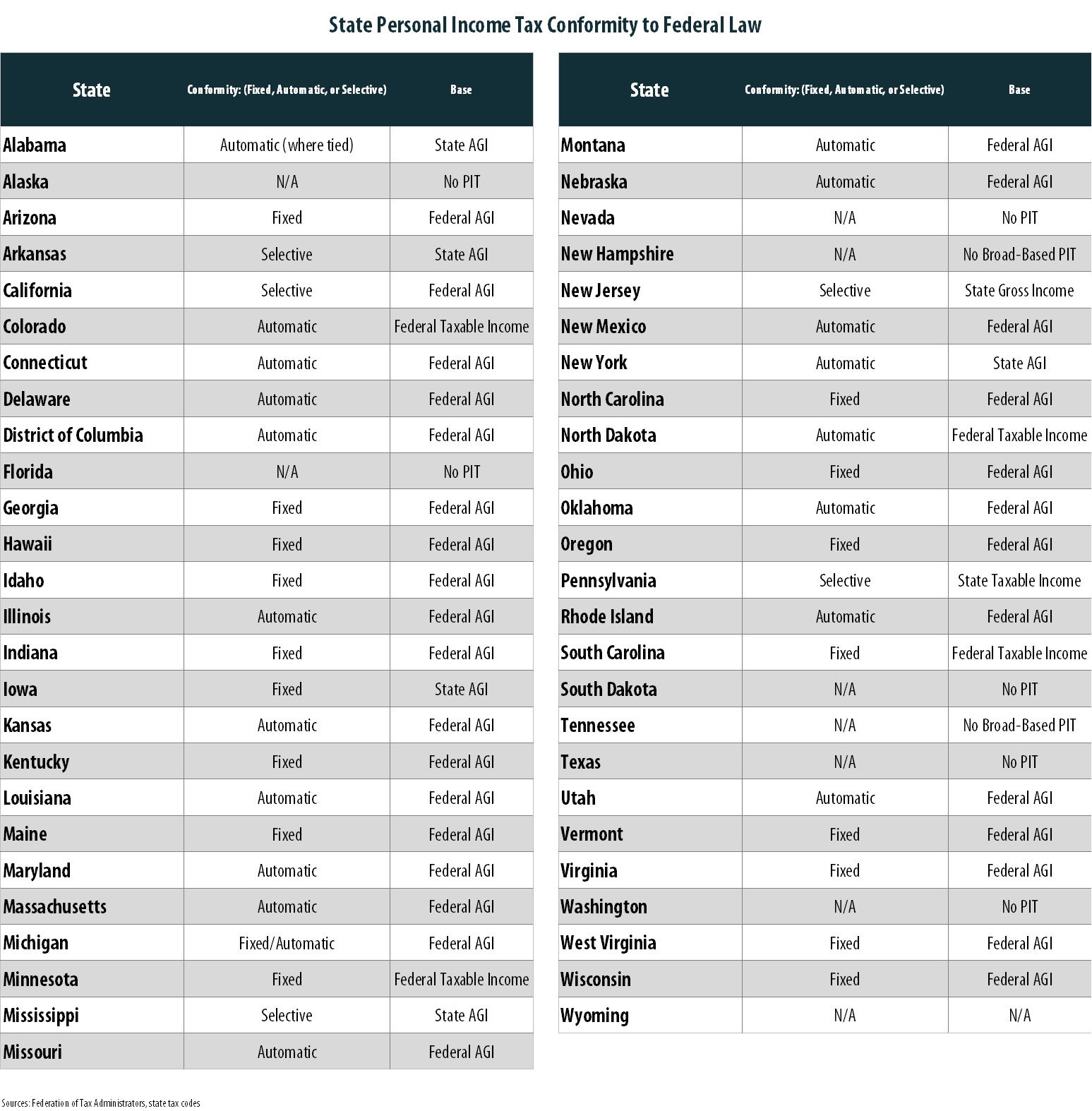

Most states with personal and corporate income taxes link their tax codes to federal tax law in some way, also known as “coupling” or “conforming” to the federal code, which helps simplify tax preparation. The most common way of doing so is to begin state income tax calculations with the federal definition of income called Adjusted Gross Income (AGI). States then apply their own deductions, exemptions, and other adjustments to arrive at taxable income, apply state tax rates to the taxable income amount to determine taxes owed, and finally apply any additional credits. Some states conform to federal law even more closely, adopting the federal deduction and exemption amounts and thus mirroring the federal calculation all the way to the determination of taxable income. Still others calculate their own measure of AGI and taxable income but use federal definitions of the amounts included therein.

States vary not only in the extent to which they conform to the federal code, but also in their procedures for doing so. When a federal law to which a state is coupled changes, states with automatic or “rolling” conformity generally adopt the federal changes automatically and must specifically de-couple from changes they do not want to adopt. States with “fixed-date” conformity adopt the federal rules from a particular year and must pro-actively choose to go along with federal changes. The table below provides an overview of state conformity approaches.

But even these approaches are broad generalizations – no two states conform to the federal code in exactly the same way, and many couple to particular federal provisions beyond the calculation of AGI or taxable income. For example, many states set their Earned Income Tax Credits at a percentage of the federal credit, and some reference the federal inflation definition to adjust their tax brackets and other provisions for inflation over time. A handful of states (Alabama, Iowa, Louisiana, Missouri, Montana, and Oregon) are also affected indirectly by federal tax changes because they allow taxpayers to deduct the amount they pay in federal taxes from their state taxable income.

How the TCJA Affects States and How They Can Respond

Regardless of the details of how each state conforms to the federal tax code, one inescapable fact for all states is that the federal tax cuts will come hand-in-hand with reduced federal funding for many priorities such as education, health care, and basic infrastructure. On top of this, more than half of states already face revenue shortfalls and many are also already underfunding services, pension funds, and rainy day funds. And while it appears that some states may realize modest revenue gains by coupling to changes in the TCJA, there are many provisions of the federal bill that stand to reduce state revenues to an unknown extent, ongoing uncertainty regarding how states will interpret how their own laws interact with the TCJA, and a very high likelihood that people will discover and exploit loopholes in the hastily crafted law to further reduce their taxes in ways that no state revenue forecast can predict. Finally, to the extent that coupling to the TCJA does bring in revenue for states, it is mostly temporary, as most of the personal income tax provisions expire after 2025. Overall, even for those states that do see a revenue gain as a result of adopting the TCJA’s changes, the gains will be very small relative to states’ funding needs.

A second inescapable fact is that the federal tax cuts contained in the TCJA are overwhelmingly skewed to the wealthiest people in every state. Preliminary modeling using ITEP’s microsimulation tax model indicates, in fact, that the federal tax cuts for the richest one percent of Americans will dwarf state revenue gains from personal income tax changes roughly ten-to-one (See nearby graph). State policymakers should have these facts squarely in mind as they debate how to respond. States that recognize the need for additional revenue should ensure they do not raise it on the backs of low- and middle-income families, as these families get a meager share of the federal tax cuts and already pay an outsized portion of state and local taxes. They should instead work to require their wealthiest residents, who are the greatest beneficiaries of the federal tax cuts, to contribute more toward state funding needs. And if state leaders insist on avoiding overall revenue increases, they should do so through tax cuts that are targeted to low- and middle-income families, who are most likely to see short-term state tax increases and long-term federal tax increases.

Impacts of Major TCJA Provisions Options for Response

Standard and Itemized Deductions Changes

Standard Deduction: The TCJA nearly doubles the federal standard deduction, to which about nine states and the District of Columbia are currently coupled.[1] On its own, such a change would reduce taxes for everyone currently paying income tax because it reduces the amount of income subject to tax across the board. However, this result is unlikely in any state because each of these states also currently couples to some extent to federal itemized deductions, and there is inherent interaction between standard and itemized deductions because each taxpayer must take one or the other.

Itemized Deductions: The TCJA temporarily increases the medical expenses deduction, eliminates some miscellaneous deductions, and caps the federal deduction for state and local taxes (“SALT” deduction) at $10,000. Thirty-one states[2] and the District of Columbia follow federal itemized deduction policy to some extent. Because most of these states do not couple to the federal deduction for state income taxes paid but do allow a deduction for property taxes, the net effect of coupling to these changes would be a minor expansion of the income tax base as few people pay $10,000 in property taxes alone and the other eliminated deductions are relatively small. States with relatively low property taxes will see even less of an effect while states that do allow a deduction for state income taxes[3] would see more significant base expansion effects.

Elimination of the “Pease” disallowance for itemized deductions: An overlooked but very important aspect of the TCJA is that it does away (temporarily) with the “Pease” disallowance, which reduces the total value of itemized deductions for very-high-income taxpayers and to which many states are currently coupled. These families previously saw their total deduction amount limited but can now fully deduct their charitable contributions and allowable mortgage interest on their federal taxes, and in states that couple to the change, on their state taxes as well. This means that in many states, the highest-income families would get a net state tax cut as a result of federal itemized deductions changes; they would pay slightly more due to the SALT cap but that effect would be outweighed by the elimination of the cap on their other deductions. These effects will be strongest in states with relatively low property taxes, where the SALT cap will have even less of an offsetting effect. On the other hand, states that use independent limits on itemized deductions rather than coupling to Pease may see a small tax increase on high-income taxpayers.

Other effects: Another underappreciated aspect of the TCJA’s impact on states is that in states that do not couple to the federal standard deduction amount but do require their residents to take the state standard deduction if they took the federal standard deduction, many of the people who will now take the new higher federal deduction will be forced into taking the state standard deduction even though itemized deductions would have been better for them at the state level. This would raise revenue in these states, mostly affecting middle- to upper-middle-income taxpayers who previously itemized at the federal level. Georgia, Maryland, and Virginia are examples where this impact is most notable as they have state standard deductions much smaller than the federal amount.

What state lawmakers can do: Each state will need to look at the revenue and tax fairness impacts of coupling to or decoupling from the specific combination of changes most likely to affect them. States that currently couple to Pease can improve revenues and help ensure they do not further exacerbate the regressive effects of the TCJA by decoupling from its elimination or adopting their own limits on itemized deductions. States with no limitations on itemized deductions may consider implementing limits or even eliminating itemized deductions altogether, perhaps following the lead of other states that have done just that. States in need of significant revenue might decouple from the federal standard deduction in order to avoid the revenue loss from this not-well-targeted tax cut. And all states, particularly “fixed-date” conformity states, have the option to decouple from all of these changes and fix their state deduction policies to the more stable federal policy that existed before the TCJA was passed and will return again after 2025.

Personal and Dependent Exemptions

The TCJA eliminates federal personal and dependent exemptions. Nine states and the District of Columbia currently couple fully to the number and dollar amount of federal exemptions.[4] There are also some 16 other states potentially affected by the change because while the amounts of their exemptions are independent of federal law, the number of exemptions a taxpayer is entitled to is based on allowable federal exemptions.[5] Although the TCJA does not eliminate the federal exemptions – rather, it temporarily reduces their value to $0 – some of these states have already concluded that their state exemptions are eliminated and many of them have yet to make a final determination.

What state lawmakers can do: Eliminating these exemptions raises revenue by increasing the amount of income subject to tax across the board, and for that reason it will be tempting for states to couple to this change. But because the exemption is a flat dollar amount, the effect is regressive, amounting to a tax increase that matters much more to the budget of a low- or middle-income family than to those with higher incomes. One option for state policymakers is to simply decouple from the federal exemptions or from the temporary elimination in the TCJA. Another is to adopt the change but offset the regressive effects through targeted tax cuts such as enacting or increasing state-specific low-income credits and Earned Income Tax Credits (EITCs). At a minimum, lawmakers should reject proposals to pair the exemption elimination with income tax rate cuts that primarily benefit their wealthiest residents, a blatant tax shift onto low- and middle-income families that exacerbates the regressive effects of the TCJA, made even worse if the rate cuts are permanent while the exemption change is temporary.

Deduction for Pass-Through Income

The TCJA creates a new 20 percent deduction for “pass-through” income and a limit on pass-through losses. Many businesses, rather than paying the corporate income tax, pass their profits through to their owners who pay personal income tax on that income instead. These types of businesses will now be able to deduct 20 percent of that income from their federal taxable income. Only the few states that couple to federal taxable income[6] would be affected by this change by default, but the federal tax cut going to these businesses is relevant to the debate in every state. At both the federal and state level, it is a tax cut whose benefits are skewed overwhelmingly to the highest-income 5 percent of residents.

What state lawmakers can do: The states that currently couple to federal taxable income can easily decouple from this particular change and should do so. They may also consider scaling back their conformity to the more common practice of starting with federal AGI and setting their own deduction and exemption policies. And every state in need of revenue should note that these particular businesses and their wealthy owners have just received a major federal tax cut, creating an opportunity for states to raise revenue through targeted taxes or surcharges on these businesses.

Other Effects and Responses

Six states allow a state deduction for federal income taxes paid.[7] The TCJA’s massive federal tax cuts reduce the amount that taxpayers can deduct in these states and therefore will result in additional revenue in those states, particularly in Alabama, Iowa, and Louisiana where the deduction is uncapped. The deduction itself is an unnecessary and regressive feature of these states’ tax codes that happens to result in a revenue gain in this case but generally leaves states vulnerable to unpredictable federal policy changes. These states should first consider eliminating or limiting the deduction and directing the revenue toward state investments or tax changes that make their tax codes less regressive and more stable. If they do not go that far, they should exercise great caution because the revenue gains will likely be temporary and could swing dramatically in the other direction if Congress reverses course to balance the federal budget in the future.

The TCJA permanently adopts the “Chained CPI” as the federal inflation measure. Moving to this version of the Consumer Price Index (CPI) for adjusting tax parameters over time – including income tax brackets, EITC parameters, and deduction and exemption amounts – affects states to some degree, particularly in the long term. Reducing these cost-of-living adjustments means that taxes will slowly increase and, for low- and middle-income families, that the TCJA raises their federal taxes in the long run. States can opt to switch to another inflation measure but a simpler approach may be to strengthen other protections for low- and middle-income families.

The TCJA increases the child tax credit. Only two states, Oklahoma and New York, have credits directly tied to the federal child tax credit. In Oklahoma, the federal credit change reduces taxes primarily on middle-income families since the state limits the credit to taxpayers with incomes under $100,000, so state lawmakers should consider remaining coupled to the increase if it does not greatly interfere with their ability to fund other priorities. New York lawmakers should consider decoupling from the expanded income eligibility which gives the credit to married couple taxpayers with incomes up to $400,000 (as opposed to $110,000 under permanent law).

The TCJA raises the federal estate tax threshold. Five states and the District of Columbia[8] couple to the federal estate tax threshold and will lose revenue if they remain coupled to the new higher threshold in the TCJA. The revenue effects of coupling to the change are unknown at this point but are undoubtedly negative and regressive. These states, and most others, can look to decouple from the federal estate tax altogether, which has been greatly weakened over time. States can establish their own estate or inheritance taxes that will do more to protect revenue adequacy and reduce the concentration of wealth.

The TCJA changes “529” college savings plans. Expanding the use of tax-advantaged “529” college savings accounts for private K-12 education will reduce state revenues, but the extent of the effect is indeterminate. States should monitor this to determine whether policy changes are needed.

The TCJA repeals the Affordable Care Act Insurance Mandate. This change will affect states as well but its effects are also indeterminate.

The TCJA reduces the corporate income tax rate, moves to a “territorial” corporate tax scheme, allows businesses “full expensing” of equipment purchases, and makes other changes to business taxes. These changes too have unknown effects for states but will likely result in reduced state revenues. States should again exercise caution and budget conservatively knowing that these corporate tax cuts (which are permanent) are likely to further weaken their revenues and introduce additional uncertainty into revenue forecasts.

[1] Colorado, District of Columbia, Idaho, Minnesota, Missouri, New Mexico, North Dakota, South Carolina, Utah, and Vermont.

[2] All of the above as well as Alabama, Arizona, Arkansas, California, Delaware, Georgia, Hawaii, Iowa, Kansas, Kentucky, Louisiana, Maine, Maryland, Mississippi, Montana, Nebraska, New York, North Carolina, Oklahoma, Oregon, Virginia, and Wisconsin.

[3] Arizona, Georgia, Hawaii, Louisiana, and North Dakota.

[4] These are Colorado, District of Columbia, Idaho, Maine, Minnesota, New Mexico, North Dakota, South Carolina, Utah, and Vermont.

[5] These include California, Delaware, Illinois, Indiana, Kansas, Maryland, Massachusetts, Michigan, Missouri, Nebraska, New York, Ohio, Oregon, Rhode Island, West Virginia, and Wisconsin.

[6] Colorado, Minnesota, North Dakota, and South Carolina.

[7] Alabama, Iowa, Louisiana, Missouri, Montana, and Oregon

[8] Delaware, District of Columbia, Hawaii, Maine, Maryland, New York,