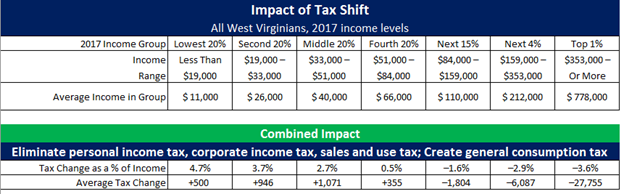

A recently introduced Senate Bill in West Virginia (SB 335) would ultimately eliminate the state’s personal and corporate income taxes, do away with the sales and use tax, and reduce the state’s severance tax. Under the plan, the revenue lost from this assortment of diverse taxes would be replaced by an 8 percent broad-based general consumption tax.

The result: low- and middle-income West Virginians pay more, much more, while wealthy residents heavily benefit.

In analyzing key components of the proposal, we found the plan to be highly regressive. On average, West Virginians earning less than $84,000 will pay more while those in the top 1% would receive an average tax cut of nearly $28,000.

*This analysis assumes a revenue neutral proposal.

For additional detail on the proposal and what it would mean for West Virginia, visit the West Virginia Center on Budget and Policy’s presentation before the Senate Select Committee and their detailed write-up of the impact.