ITEP and Local Progress Impact Lab co-authored this report.

I. Introduction: It’s Time To Tax the Rich to Fund Our Communities

Working families in the U.S. are struggling. Decades of unchecked corporate greed have pushed up prices and kept wages low. Since 2020 alone, the prices of basics like housing, food, energy, and healthcare have increased by roughly 30% to reach record highs, making them unaffordable for many in our communities. At the same time, wages for working people have not kept up, resulting in the highest levels of credit card debt in U.S. history and missed payments at rates not seen since the 2008 Great Recession.

Meanwhile, the richest households and corporations have never had it so good. Thanks in large part to the massive tax cuts for the rich from President Trump and his congressional allies in the Tax Cuts and Jobs Act of 2017, the top 1% of Americans have seen their net worth explode by 120% from 2017–2025, a large jump from the 45% increase in net worth from 2009–2017. The number of U.S. billionaires rose by 50% from 2017–2025. Now, the bottom half of U.S. households—66 million households—hold $4.1 trillion in net wealth while the 905 billionaires in the U.S. hold almost twice as much wealth at $7.8 trillion.

That working families are scraping to get by while the rich get richer is the result of policy choices baked into our tax systems at the federal, state, and local levels. Those policy choices systemically favor moneyed interests over the public. And President Trump and his allies in Congress are only doubling down on these injustices. Trump’s signature legislative achievement thus far in his second term, the so-called One Big Beautiful Bill Act, was the biggest transfer of wealth from the working class to the rich in U.S. history: by 2035, the top 1% will have received over $1 trillion in tax cuts as working families suffer from massive cuts to the Affordable Care Act (ACA), Medicaid, and the Supplemental Nutrition Assistance Program (SNAP).

What that looks like on the local level is this: the wealthiest individuals and profitable corporations get richer from the president’s policies, while federal funding cuts decimate local budgets and threaten public programs that make energy, food, housing, and healthcare more affordable and accessible. Without urgent action, working families will become poorer and sicker as Trump’s rich allies become more powerful.

This system is deeply unfair and people know it. The American public overwhelmingly supports raising taxes on big corporations and the rich, with more than 80% of likely voters supporting higher corporate taxes with fewer loopholes, and more than 70% supporting making the wealthiest individuals pay more. This holds true at the local level, too, with support in rural, suburban, and urban communities across the country for taxes on wealthy households and profitable corporations.

The task for local elected officials in this moment is therefore clear: use available tools to make the wealthy pay their fair share to fund the essential public goods that allow our communities to live safe, healthy, and thriving lives. In other words, it’s time to tax corporations and the ultra-wealthy. This policy toolkit is designed to equip local leaders to do just that by outlining the importance of progressive revenue, common obstacles, and ways to make the rich pay their fair share.

II. An Overview of Local Progressive Revenue

Every day, local governments deliver the public services that communities need to thrive, like safe streets, quality schools, public health systems, parks, affordable housing, and vital infrastructure like water and sewage. To sustain these services, localities need reliable and equitable sources of revenue. Raising that revenue in a progressive way – that is, demanding that those with the greatest ability to pay contribute the most – helps ensure that communities can equitably fund these needs.

At its core, progressive revenue reflects a simple principle: that public investments that benefit the whole community should be financed in a way that asks more from those who have benefited most from the local economy.

Progressive v. Regressive Taxes

Definitions:

- A regressive tax makes middle- and low-income households pay a larger share of their incomes in taxes than the rich.

- A proportional tax takes the same percentage of income from everyone, regardless of how much or how little they earn.

- A progressive tax is one in which upper-income families pay a larger share of their incomes in tax than do those with lower incomes.

Sales taxes, excise taxes, fees for services, fines levied for traffic violations or in connection with the incarceration system – all of these are regressive; they take more from the poor than the wealthy relative to their incomes.

By contrast, more progressive taxes like graduated income taxes, well-designed taxes on high-end real estate transactions, and taxes on profitable corporations can align revenue systems more closely with residents’ ability to contribute.

Property taxes are a mixed bag, with their progressivity depending heavily on their specific design and administration.

The goal should be to ensure that essential services remain accessible and adequately funded without disproportionately extracting funds from working families.

Progressive Revenue Is a Fiscal Responsibility

But this is not just about inequality. It’s also about fiscal responsibility. By ignoring a major potential source of revenue – the income and wealth of their most prosperous residents and businesses – many localities are missing an important opportunity to diversify their revenue streams. This can be hugely consequential when recessions or economic shocks occur. A revenue system that relies almost entirely on just one source, all else equal, is vulnerable to economic swings in a way that a more multifaceted revenue system is not.

And the reality is that corporate profits and the incomes of the wealthy represent some of the fastest-growing parts of the economy. To overlook taxes on profits, income, and wealth not only asks more of working families than the rich and starves public programs of badly needed revenue, but it undermines our communities’ long-term viability.

In other words, strengthening progressive local revenue systems can help localities build a more stable foundation for the services residents depend on. By asking those with the greatest capacity to contribute a fairer share, local governments can reduce reliance on regressive revenue sources, better withstand economic shifts, and sustain investments that support thriving, equitable communities. In an era of fiscal uncertainty and declining federal funds in areas like healthcare, community development, and education, expanding the use of progressive local revenue is not only a matter of fairness – it is a practical strategy for protecting the public services that underpin safe, healthy communities.

But because of a long history of governance that enabled the wealthy’s hoarding of resources through low taxes and handouts of public subsidies, nearly all state and local tax codes today are upside-down. They collect a larger share of income from those with low and moderate incomes than from the highest earners.

And local governments in particular currently underuse progressive revenue tools. Across the nation, the majority of local revenue is raised through property taxes and sales taxes, with relatively limited use of progressive options such as graduated local income taxes, high-value real estate transfer taxes, or targeted taxes on concentrated wealth and high-profit industries.

The lopsided way in which those taxes are collected deepens the massive gap between high-income households and low-income households. But it doesn’t have to be this way. As this report shows, local policymakers have multiple options to make their revenue systems more progressive.

Further Reading

-

- ITEP, Who Pays? A Distributional Analysis of the Tax Systems in All 50 States, Seventh Edition. 2024.

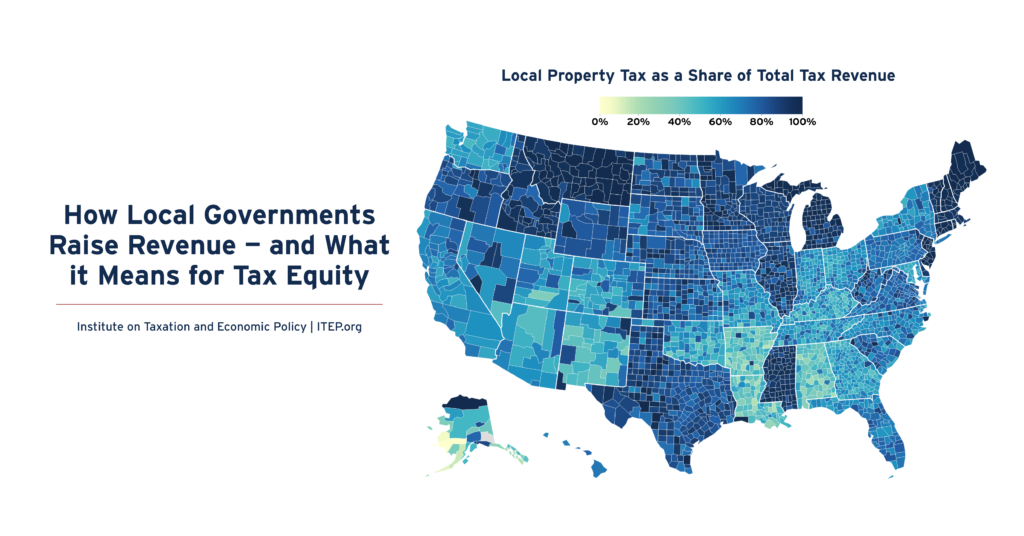

- Rita Jefferson, Galen Hendricks, How Local Governments Raise Revenue — and What it Means for Tax Equity, ITEP (Dec. 5, 2024).

- Wesley Tharpe, States Should Protect or Raise Revenue as Uncertainty Looms, Center on Budget and Policy Priorities (Jan. 18, 2023).

III. Common Obstacles to Local Progressive Revenue

Wealthy interests have used their economic power to create formidable obstacles and wage well-funded fights against attempts to make them pay their fair share. As a result, there are entrenched legal, cultural, and economic biases that bend our tax systems towards the interests of the rich and starve local governments of badly needed revenue to fund our needs. Before launching into policy tools, this section will survey three common obstacles that localities encounter when pursuing progressive revenue and ways to push back.

1. Preemption

As legal creations of their home states, municipalities derive their taxing powers from state law. Local governments’ authority to change existing or implement new taxes varies widely across and even within states because of preemption, the principle that a law from a higher level of government trumps a law from a lower level of government when those laws are on the same subject and there is a conflict between the two, or when the higher level of government has barred lower levels from making laws on certain subjects.

When it comes to taxation, preemption abounds and comes in various forms that restrict localities’ ability to make their tax systems fairer and more resilient. For example, in some states, certain kinds of taxes may be prohibited altogether, while in others, localities may have to get special permission from the state legislature or go to the ballot to have a tax measure approved. This toolkit notes in Section V where certain kinds of taxes, like income taxes, are permitted. But one common source of preemption that allows the rich to escape paying their fair share can be found in most state constitutions: the uniformity clause.

Uniformity clauses generally require that taxes be levied at a uniform, or flat, rate within a class of property or taxpayers—thereby prohibiting graduated, progressive tax rates. A large majority of state constitutions contain these clauses in some fashion, making it difficult for localities to implement targeted tax policies that ensure the richest households and corporations pay their fair share. However, uniformity clauses sometimes apply to only certain kinds of taxes. For example, Arizona’s uniformity clause only applies to property taxes, whereas sales, income, and excise taxes are permitted to have differentiated rates.

As always, it is important to investigate the exact contours of municipal tax authority in your jurisdiction when considering local policy measures, as local authority varies significantly from state to state and sometimes even within a state. We highlight several policies discussed further below that are more commonly available to localities even in states with high levels of abusive preemption.

But to truly overcome preemption, statewide powerbuilding is necessary. Local elected officials must organize across jurisdictions and in coalition with local and statewide groups to replace the tax rules so often biased towards the rich with ones that raise progressive revenue to support working families. To find a tax and budget justice coalition in your state, please reach out to Local Progress staff.

2. Persistent Myths

Preemption is a legal constraint on localities’ ability to make the rich pay their fair share. But it is propaganda and exaggerated claims from corporations and the wealthy that shape the political possibilities of our tax systems. Prominent figures in the media and government spread myths and disinformation from wealthy interests that make progressive revenue seem like a bad, even dangerous, idea, when it is in fact the just and fiscally responsible approach.

It is therefore essential for local elected leaders to identify the most common myths the rich peddle to block progressive revenue, know the facts, and use their platforms to steer the conversation towards what overwhelming majorities of voters and residents want: for the richest individuals and corporations to pay their fair share so that we can fund schools, housing, transit, and other community needs.

Myth 1: The Millionaire Tax Flight Myth

The successful campaigns of Mayors Brandon Johnson of Chicago, Zohran Mamdani of New York City, and Katie Wilson of Seattle stoked an anti-tax backlash peddling a decades-old myth: if taxes are raised on top earners, they will flee for places with lower taxes for the rich.

Despite the prevalence of this myth, research shows that the claims are not supported by the data. The fact is that millionaires are unlikely to move because of taxes. Instead, like most other people, millionaires primarily choose where to live based on community ties, schools, and jobs, and are not likely to uproot their lives based on a marginal tax difference. In fact, states with the most progressive tax codes are consistently rated as places with a higher quality of living and better places to live, work, and raise a family. Indeed, research shows that the number of wealthy individuals and their cumulative wealth grew after the enactment of higher taxes on high earners in Massachusetts and a progressive capital gains tax on high-wealth Washingtonians. That is because when we all pay in and the rich pay their fair share, governments are able to fund education, healthcare, housing, and other public goods that make our communities more prosperous and secure.

To prove their point, proponents of the millionaire tax flight myth will often cite anecdotal, one-off examples of individual millionaires moving or threatening to move to lower-tax jurisdictions. But those examples are just that: drops in the bucket. Studies suggest only 0.3% of U.S. millionaires move to a lower-tax state in a given year. Indeed, a landmark study from 2025 found that “the rich in high-tax states do not move any more often than those in low-tax states.” Alternatively, peddlers of this myth will point to migration patterns of people leaving states with more progressive income tax systems like New York and California for states lacking income taxes like Florida and Texas. But those moving are overwhelmingly working families seeking cheaper housing, not lower taxes. And in reality, states like Florida and Texas actually have higher taxes on low- and middle-income households than California does thanks to state tax systems that systematically favor the rich.

In response to this myth, local elected officials should reframe the debate by grounding it in the real danger to our communities: working families being displaced because of a high cost of living and a lack of funding for public goods like housing and healthcare.

Myth 2: The Business Tax Flight Myth

Similar to the millionaire tax flight myth, the business tax flight myth claims that if a locality ends corporate welfare like property tax abatements or raises taxes directly on businesses, those companies will leave and take with them jobs, tax revenue, and other economic benefits.

But the data show that fears of business flight are overblown. Research indicates that tax incentives determine companies’ location decisions only 2% to 25% of the time. That is likely because taxes typically only consist of 2% to 4% of a business’s total costs and because relocation is logistically complicated and often extremely costly. For example, Ken Griffin’s hedge fund Citadel’s relocation from New York City to Miami incurred over $1.3 billion in real estate expenses, not including the costs of employee relocation.

And corporate subsidies like property tax cuts for businesses come with their own costs. The rationale for them is that the tax cut will spur economic development that will outweigh the foregone revenue. But generally, there is little evidence that property tax cuts for corporations are an effective economic development tool. As discussed further below, eliminating the vast range of corporate tax breaks is one of the most significant actions municipalities can take to build a progressive property tax system that funds essential services and ensures the rich pay higher or even similar rates as working families.

Myth 3: Low Taxes Spur Growth

Another common tax myth is that lower taxes pay for themselves by fueling economic growth. The idea is classic trickle-down economics: with the money that otherwise would have gone to taxes, businesses and the wealthy will supposedly spend that money in ways that expand economic activity and the revenues generated therefrom.

This is an idea that even conservative think tanks recognize is a myth. When given tax cuts, wealthy individuals and businesses are not more likely to invest in productive activity that benefits all. While arguments for local tax cuts or abatements promise economic development, it is most often economic development at the expense of neighboring municipalities rather than supporting broader community development needs. Taxes are a relatively small part of the cost of doing business, and there is little evidence to suggest businesses decide where to locate based exclusively on the basis of the state or local taxes. Moreover, each lost dollar of revenue means less money to invest in crucial public goods like education, transportation, housing, and energy infrastructure, all of which have enormous impacts on the economic health of our communities.

The Problem of Concentrated Wealth and Community Development

There is a deeper structural tension in local fiscal and community development policy when it comes to raising progressive revenue. To have a tax base that generates sufficient revenue, municipalities may attempt to attract or retain large businesses or wealthy households through means that might, at the same time, make life harder for working families. For example, the development-oriented policies many cities pursue to boost property valuations and property tax revenues may fuel gentrification and displacement. And of course, as Supreme Court Justice Louis Brandeis said, “We may have democracy, or we may have wealth concentrated in the hands of a few, but we cannot have both.”

Taxing the wealthy is thus a necessary but not sufficient step to ensuring that local economies center the needs of working people. In addition, localities should take steps to pursue alternative development models that build the self-sufficiency of publicly and community-owned economies. Local leaders may do so by directing revenues into public banks, community land trusts, social housing developers, and other public or cooperative enterprises that make local economies more stable, democratic, and independent of the whims of the wealthy.

IV: Design Considerations

Developing a progressive revenue strategy requires answering the following questions:

- What are we trying to fund?

- Who should pay?

- What will the economic impact be?

- How will the policy be implemented?

- What is the path from proposal to enactment?

What are we trying to fund?

Advocates often come to the revenue table because crucial public services or investments are underfunded or threatened with underfunding. Local governments use taxes and fees to pay for schools, childcare centers, healthcare facilities, jobs programs, public safety programs, parks, transportation infrastructure, and other things necessary for a community to thrive. Sometimes there’s a specific investment needing financial support. At other times there’s recognition that underfunded public services generally are falling short of community needs. Either way, it’s a budget gap that starts the revenue conversation.

Lay the foundation for a successful revenue campaign by articulating both (a) a specific programmatic goal (e.g., “fund new childcare programs” or “avert budget cuts that would cause teacher layoffs”) and (b) a specific revenue target to meet that goal, in dollars. Remember that most spending needs are multi-year and will rise in cost over time with economic growth or inflation, so make sure your revenue source can hold up for the long haul.

Being clear about what we’re trying to fund does not mean that the specific dollars used from a revenue proposal must be spent on a specific spending program. In fact, such statutory earmarking can hinder long-term efforts to support strong community services. A measure to fund transit, for example, can help take pressure off the budgets for schools, roads, and parks, and leaders in those areas can be effective messengers in explaining the broad public benefit of what otherwise might be seen as a parochial concern.

Who should pay?

Revenue proposals should reflect ability to pay, asking the most of those with the greatest resources. In today’s highly unequal economy, those with the greatest ability to pay are often wealthy individuals, large property owners, and highly profitable corporations. In nearly every community, these groups are already benefiting from upside-down tax systems that ask the least of those with the highest income. The wealthy are also benefiting tremendously from the 2025 Trump tax law, which is sending more than $1 trillion over the next ten years to the nation’s millionaires and billionaires, even as federal tariffs and other policies lead to higher taxes for low- and middle-income families.

Exactly how best to match a revenue proposal to ability to pay – that is, how to design a fair tax – will vary by community. In one place, we may want to focus on high-income suburbanites benefiting from city services. In another place, it could be a burgeoning tech sector sparking gentrification. In a third place, it could be wealthy universities and hospitals sitting on massive, untaxed endowments and operating glitzy facilities that use locally funded services for free.

One way to identify progressive revenue options, even in the face of state preemption or political opposition, is to scrutinize the exemptions, deductions, and other tax-based subsidies that localities often provide to special interests. This could include favorable property tax treatment, payroll tax rebates, sales tax exemptions, and other giveaways.

What will the economic impact be?

Many tax debates turn into debates about economic development. As discussed above, opponents of a new revenue source inevitably argue that the proposed tax will make the community “uncompetitive” and invoke the millionaire or business tax flight myth. Advocates should document the economic benefits of the proposed investment. Putting money into schools, roads, and family economic success can pay off for a jurisdiction – in both the short and long term – far in excess of the cost in increased taxes.

How will the proposal be implemented?

Winning enactment of a revenue proposal will be a hollow victory if it cannot be implemented effectively. Proposals should incorporate an accurate assessment of what resources the jurisdiction will need for effective implementation. They should also be carefully reviewed, before going forward, to make sure that they will not be easy for taxpayers to avoid or encourage taxpayers to adjust their finances to get around payment. A careful review to ensure compliance with state and federal law can avert the fear that an unfriendly judge could short-circuit the effort.

For example, a tax on high-valued property will have less impact unless the jurisdiction has practices in place to accurately assess property values and defend those assessments in court if necessary.

Piggybacking on existing progressive taxes can be a good way to increase progressivity without the implementation challenges of a brand new tax. Many localities with local income taxes, for example, derive the calculations from the state income tax.

What is the pathway from proposal to enactment?

A winning campaign can be as simple as a well-timed meeting with a key lawmaker or as elaborate as a multiyear campaign with hundreds of allies. Sometimes, revenue measures move very fast. In the heat of a budget debate, a well-placed policymaker can insert a revenue measure into budget legislation and push it through with little debate. That kind of victory can look easy, but it still requires careful assessment, planning, timing, and luck.

Other revenue measures may require a larger-scale effort, especially if the dollars involved are relatively large, if the measure requires a popular vote, and/or if the proposal runs up against well-organized opposition by wealthy or corporate interests. Developing alliances with advocates across multiple areas of the budget can help ensure that a revenue proposal isn’t seen as unduly propping up one part of the budget at the expense of another. Messaging matters, too. Any revenue measure, even a relatively narrow one, should be articulated as part of a longer-term campaign or movement to elevate the need for adequate funding of all the public services needed for a community to thrive. Take the opportunity to explain how the current revenue system enriches the wealthy and well-connected at the expense of the rest of us, and how changing the rules can ensure that they pay their fair share so that the whole community can thrive.

Further Reading

-

- Topos Partnership, Making a Case for Taxes (Feb. 2026) (messaging report).

- State Revenue Alliance, Local Revenue Toolkit (2025) (including messaging guidance at 7–13).

- The ITEP Guide to State & Local Taxes: What Principles Should Guide State and Local Tax Policy?, ITEP.

- Steve Wamhoff and Michael Ettlinger, State-by-State Estimates of the First Year of Trump’s Tax Policies: All But the Richest Americans Face Higher Taxes, ITEP (Feb. 23, 2026).

V: Revenue Generators

Income Taxes

Overview

An income tax is any tax levied on wages, investment income, or business income or profits. This means that if you work at a job, collect passive income like interest or dividends, or if your company makes a profit, those earnings may be taxed. The federal government as well as most state governments and many local governments collect income taxes.

At the local level, 7,045 taxing districts in 15 states and the District of Columbia levy taxes on personal income, capital gains, business gains, and/or corporate profits. Iowa, Kentucky, Ohio, and Pennsylvania allow a combined 2,989 school districts to collect local income taxes. In the localities where they are levied, income taxes provide substantial revenue. For instance, Baltimore collects approximately 40 percent of city revenues from its local income tax. Nearly 40 percent of Philadelphia’s revenues come from its wage and earnings tax and business taxes.

Some states connect their local income tax systems to the state income tax system. In those states, the state collects the local income tax on behalf of each locality and distributes those revenues. In others, the locality collects and administers its own tax.

Depending on the state, localities can tax residents and commuters. For instance, counties in Maryland only collect income tax revenues from their own residents, while cities like Wilmington, Delaware and Yonkers, New York can collect revenues from residents and commuters. In some cases, like in Ohio, it’s possible for individuals to be taxed by two different municipalities: where they work and where they live. In the District of Columbia and various municipalities in four states – Iowa, Maryland, New York, and Oregon – municipalities can use graduated income tax rates, meaning that a higher marginal tax rate applies to individuals or households with higher incomes.

Progressivity

Income taxes are generally better than other types of taxes at reflecting a taxpayer’s ability to pay, as those without income will not pay them. Ideally, an income tax would be levied on all types of income (investment income as well as salaries and wages) and would have a graduated rate structure with higher rates applied to higher-income individuals or households. Local leaders should avoid or eliminate special tax breaks, loopholes, or other unfairly distributed tax cuts.

In localities that have local income taxes, leaders should push for tax rates to be graduated and marginal, i.e., the tax rate goes up as incomes increase, and that the first dollar of earnings is taxed at a different rate than, for example, the millionth dollar of earnings. This smooths out the earnings curve and helps prevent income tax avoidance. But even a flat-rate income tax can be more progressive in its impact than a sales tax or a property tax.

Design Considerations

Robust, progressive state tax systems anchored by graduated-rate personal income taxes and strong corporate income taxes are ideal for localities, because they allow for robust funding of state aid to municipalities and the equalization of taxes across wealthier and poorer jurisdictions.

Local leaders should encourage states to protect and strengthen income taxes at the state and local levels. The 2025 Trump tax law gave out an estimated $1 trillion in personal and corporate income tax cuts to the wealthiest 1 percent of taxpayers, slashing essential government services like SNAP and Medicaid to help pay for them. Many states conform to the federal tax code, meaning that individuals and corporations will receive not just one tax cut, but two – when the impact is passed through to the state tax code. These provisions will erode state and local tax bases for little to no economic benefit. States should therefore decouple from those federal provisions, including the qualified small business stock exclusion (QSBS), opportunity zone credits, and deductions for tips and overtime. While the tips and overtime provisions have some political appeal, they erode the income tax base by exempting certain professions rather than income. There is no economic rationale for taxing restaurant staff at a lower rate than childcare workers.

States can also strengthen existing individual and corporate tax codes. While most states have a graduated rate income tax, 14 states have flat income tax rates that take the same share of income from low-income households as they do from wealthy households. In addition, many states’ corporate tax codes are insufficient for taxing parts of the digital economy, or are riddled with loopholes. States can pursue reasonable changes to those, like adopting progressive tax rates and worldwide combined reporting. States could also adopt a wealth proceeds tax, designed to generate revenues from passive income like interest, capital gains, and dividends. Even in cases where local income taxes may be politically or legally challenging, local leaders can press state legislators to improve state income tax systems, which can improve overall tax progressivity and raise much-needed revenues for state services.

Model Policy

Maryland’s statewide local income tax model

- Maryland has a comprehensive, statewide program of local income taxation that promotes progressivity at the local level, eliminates double taxation for residents, and offers a substantial revenue source for county governments and the city of Baltimore.

- All residents in Maryland are charged a local income tax rate based on where they live. Each county and the city of Baltimore selects its own tax rate. Two counties, Anne Arundel and Frederick, have progressive marginal rates depending on income and family size. The state administers the collection and distribution of tax revenues on behalf of counties, which simplifies local income taxes for residents, businesses, and counties. It also allows for easier application of local refundable credits, like the Earned Income Tax Credit or Child Tax Credit. Montgomery County has a local EITC.

- The local income tax in Maryland provides a substantial portion of revenue for the counties that collect them. State law requires county tax rates to be set between 2.25 percent and 3.3 percent; the tax provides between 12 percent and 43 percent of counties’ tax revenue.

Further Reading

-

- The ITEP Guide to State & Local Taxes: How Do Personal Income Taxes Work?, ITEP.

- Rita Jefferson, The (Mostly Untapped) Power of Local Income Taxes, ITEP (Feb. 5, 2025).

- Sarah Austin and Carl Davis, The Wealth Proceeds Tax: A Simple Way for States to Tax the Wealthy, ITEP (Oct. 30, 2025).

Property Taxes

Overview

Property taxes are levied on the value of physical property owned by an individual or business. They are the single largest source of local tax revenue, levied by localities in every state. They include both taxes on “real property,” meaning immovable property (i.e. real estate), and taxes on “personal property,” meaning physical objects like automobiles or business equipment.

Every state allows local governments to levy real property taxes on both residential and business property. Most states also allow local personal property taxes, but they often affect only businesses and sometimes personal automobiles. A few states also levy statewide property taxes.

About half of all property tax revenues nationwide go to fund K–12 school districts, making the property tax in most states the largest single school funding source. Public schools across the country are primarily supported locally by property tax revenues.

Property taxes are usually administered at the local level. Typically, municipal or county assessors determine the value of a property, which is then multiplied by the local tax rate, and collected by a local treasurer or collector’s office. Some states, like Maryland and Montana, assess properties at the state level.

In some places, properties are assessed at full market value; in other places, they are assessed at a portion of market value. Some states also allow different types of properties to be assessed at different ratios, generally designed to lower property taxes for homeowners.

Many states use various types of exemptions to the property tax to reduce the amount paid by various groups. Real property exemptions are generally used for homeowners, senior homeowners, or disabled homeowners. Personal property exemptions often exempt various types of personal property, or exempt a portion of the value of the personal property.

Many states impose formulaic limits on local property taxes. These come in four varieties: assessment growth limits, levy growth limits, revenue growth limits, or expenditure limits. All of these are bad solutions for municipalities dealing with growing costs of expenditures and increased demands from taxpayers. For instance, California’s Proposition 13 capped the growth of assessed values to 2 percent annually and limited levies to 1 percent of total property values. The amendment has severely restricted local property tax revenues, in part to blame for local governments’ high reliance on sales taxes. In addition, the law has led to substantial tax inequities between similar properties based entirely on when a property was purchased. Unlike the results of caps in many other states, Prop 13 applied broadly enough that commercial property owners also benefited, meaning that the largest beneficiaries of Prop 13 were major corporations.

Progressivity

Almost every household and business in the U.S. pays property tax to local governments and school districts, either directly as the property owner or indirectly through rent. A property tax is a benefit tax, meaning that individuals and businesses pay the tax because local services funded by the tax in turn boost property values. Property taxes can also be understood as a type of wealth tax. Houses are the most widely held form of wealth, as nearly two-thirds of Americans own their own homes. And commercial real estate represents a large share of corporate wealth.

But most wealth in America is held in the form of intangible assets like stocks and bonds – and mostly controlled by a much smaller share of households. So the property tax, as currently administered in the U.S., misses out on a large share of the nation’s actual wealth.

Because so many households hold so much of their wealth in their primary home, property taxes can fall harder on low- and middle-income households, making the tax slightly regressive, on average. The impact is worsened by systematic underassessment of high-value properties and overassessment of low-value properties. Improving the progressivity of property tax systems is possible, with many tools available to lawmakers and officials.

Progressive Property Tax Policies

- Ensure that renters and homeowners are treated equally through property tax reduction mechanisms. Renters tend to have lower incomes than homeowners. Since existing property tax measures often give preference to homeowners, policymakers should target new or additional measures toward renters.

- Address the systematic underassessment of expensive homes and businesses through regular, robust assessments with high-quality property information. Poor assessment practices exacerbate regressivity and the racial wealth gap. Academic studies show that Black-owned homes are overassessed compared to similar homes owned by white families, in part due to historical legal segregation and persistent social segregation. While some states have statutory restrictions on assessments like California, assessors in other states may be able to improve assessments through better data collection, better data analysis, and robust data checking.

- Repeal property tax caps and similar measures. These have the effect of inducing “lock-in” effects by encouraging existing homeowners to stay put, which drives up home prices and prevents younger people and families from buying homes. Instead, focus property tax breaks on families facing genuine financial distress, struggling to afford their property tax bill.

- Improve personal property taxes on vehicles or replace them with fairer revenue sources. Many states that levy personal property tax on personal vehicles use inaccurate valuations that put much of the responsibility on owners of older vehicles, far higher than the actual depreciated value of the vehicle. In Virginia, state and local leaders are trying to abolish the car tax and replace it with more progressive revenue streams.

- Adopt tools like mansion taxes, vacancy taxes, and pied-a-terre taxes. These taxes ask more of high-income or high-wealth households while protecting working people. Different cities may require different approaches; pied-a-terre taxes may be the best option for New York or Honolulu, mansion taxes may be the best approach for Philadelphia or San Francisco, and vacancy taxes may work best in Cleveland or St. Louis. Knowing the local property market is crucial for aligning these taxes with ideal housing outcomes.

- Restrict or eliminate property tax breaks for for-profit entities. These are meant to generate some public policy outcome but are often abused by organizations that have the political power to demand tax cuts from municipalities. Some of the most egregiously unwarranted property tax breaks go to professional sports teams, but more commonly they are given to developers with limited to no community benefits specified beyond “economic development.”

- Minimize the scope of Business Improvement Districts and Special Economic Zones, tools used by commercial property owners to improve the immediate conditions around their own properties. While these financing structures generally do not remove property from the tax rolls, it can reinforce inequitable distribution of public services by allowing private owners the right to privately manage public spaces. These often exist as beautification projects that can further emphasize the resource gaps between neighborhoods.

- Minimize the use of Tax Increment Financing (TIF) districts. TIFs funnel property tax funds away from community needs like schools and parks for the narrower benefit of property developers. In addition, TIFs can drive up tax rates for properties outside the zone, leading to distortions in local property markets. These are highly controversial tools, often leading to misused or poorly targeted funds, and many of which are unaccountable to residents. Promoting transparency in local TIF policies can open opportunities for residents to engage in the process. In addition, TIF districts should not be kept open beyond the lifespan of a project and should be closed once projects are completed.

- Demand that wealthy universities, hospitals, and other nonprofits that may be exempt from property taxes make “payments in lieu of taxes” (PILOTs) to compensate jurisdictions for the services they benefit from. While these can include community services, it is best practice to ask for monetary contributions to city governance.

Model Policies

Santa Fe mansion tax. Santa Fe voters established a progressive real estate transfer tax in 2023 to provide a permanent funding source for affordable housing. Santa Fe’s 3% tax applies to the portion of single-family residential property sold for more than $1 million. The graduated rate structure means a home sold for $1.1 million pays tax on $100,000 of its value, similar to the graduated design of the federal income tax. The million-dollar threshold is double the value of the median Santa Fe home.

Proceeds from these high-end purchases will provide an estimated $6 million per year into Santa Fe’s affordable housing trust fund, approximately tripling the fund’s size. The revenue will be used to build new homes and ease housing costs for low-income and middle-income residents.

Honolulu classification system for second homes and short-term rentals. Honolulu uses a classification system for valuation that balances the needs of full-time residents with owners of second homes and short-term rental operators. The tax rate for homes that don’t qualify for homeowner exemptions is marginal, but it nearly triples for properties worth more than $1 million. Properties operated as short-term rentals face a rate nearly three times the residential rate, with a marginal rate that applies at $800,000.

Washington, D.C., vacant property tax. Since 2011, Washington, D.C. has taxed vacant and blighted properties at a rate five to ten times higher than occupied properties – a method more commonly known as split roll property taxation. Properties are determined to be either vacant or blighted by the District’s Department of Buildings. Though the city relies on self-registration, the department is empowered to audit taxpayers, and has won multiple high-profile cases against negligent landlords.

The tax is paid by landlords who have persistent vacancies rather than short-term vacancies. This means that unlike traditional property taxes, these taxes are not falling on renters in the form of higher rents but instead on landowners, and it enables the city to maintain a lower tax rate for all occupied residential properties.

Administering a vacancy tax through the property tax system also has the benefit of being able to move properties through the property tax foreclosure process. This allows the city flexibility to take possession of a problem property before it can become a public health threat or further damage the property values of surrounding properties.

Case Study: Los Angeles’s Real Estate Transfer Tax

Overview

A grassroots coalition of housing advocates, labor groups, and nonprofit housing developers organized to pass Los Angeles’ real estate transfer tax, more commonly referred to as Measure ULA in 2022. Measure ULA taxes sales of buildings valued at $5 million or more, with annual inflation adjustments. All generated revenues are dedicated to affordable housing development in the city.

From April 2023 to January 2026, ULA raised over $1 billion from 1,435 transactions. Since its passage, ULA has helped fund 5,600 affordable units, provide $54 million in direct financial assistance for tenants, reduce street homelessness by 17.5%, reduce eviction filings by 16%, and support the creation of thousands of jobs tied to affordable housing development and construction activity.

Collaborative Governance in Action

One crucial way the organizers of ULA won public support for the tax was by building a diverse coalition to advance solutions identified by those closest to the problem, including unhoused people and renters struggling to stay housed in gentrifying neighborhoods. United to House LA—a coalition of homeless service providers, nonprofit affordable housing builders, labor unions, community land trusts and renters’ rights advocates—came together to meet the housing needs of low-income Angelenos by making super-wealthy property owners pay their fair share.

After an extensive, hard-fought campaign, Measure ULA won with 58% of the vote.

In response to mounting criticism of the real-estate transfer tax and attacks by private real-estate developers and anti-tax groups at the local and state levels, the Los Angeles City Council created an Ad Hoc Committee on Measure ULA in March 2026 and appointed Local Progress member and LA City Councilmember Ysabel Jurado as chair.

As chair, Councilmember Jurado is leading an ongoing, structured review of Measure ULA implementation, focused on identifying what is working in practice, where adjustments may improve delivery, and how to ensure voter-approved revenues translate into timely housing and homelessness prevention outcomes. “Measure ULA is delivering resources Los Angeles urgently needs – affordable housing, rental assistance, tenant protections, and homelessness prevention at a scale this City has never had before,” Councilmember Jurado explains. As the ad hoc committee continues hearings and develops recommendations for the City Council, Councilmember Jurado underscores the heart of the debate regarding changes to Los Angeles’s progressive real-estate transfer tax: “Any proposed changes to ULA should be judged by a simple standard: do they help Los Angeles deliver more housing and prevent more homelessness, or do they weaken the tools voters gave us to do that work?”

Further Reading

-

- Good Jobs First, Tax Break Tracker: Discover What Localities Lose to Corporate Tax Abatements (2026) (database of jurisdiction-level foregone revenues due to corporate tax abatements).

- The ITEP Guide to State & Local Taxes: How Do Real Property Taxes Work?, ITEP.

- The ITEP Guide to State & Local Taxes: How Can Communities Collect Property Taxes from Exempt Nonprofits?, ITEP.

- Rita Jefferson, Anti-Tax Revolts Backfire: What We’ve Learned from 50 Years of Property Tax Limits, ITEP (July 15, 2025).

- Brakeyshia Samms, Property Tax Reforms Can Bring Racial Justice, ITEP (Feb. 19, 2026).

- Rita Jefferson, Local Vacancy Taxes: A Tool but Not a Panacea, ITEP (Nov. 17, 2025).

- Andrew Boardman, Local Mansion Taxes: Building Stronger Communities with Progressive Taxes on High-Value Real Estate, ITEP (Mar. 14, 2024).

Sales & Excise Taxes

Overview

Definitions:

- Sales taxes (aka sales and use taxes): taxes on the sale of goods or services at the level of consumption.

- Excise taxes: taxes on specific goods or activities typically applied on a per-unit basis instead of as a percentage of the purchase price.

On average, sales and excise taxes comprise over a third of state and local taxes across the U.S., and are the second-largest source of revenue for local governments behind property taxes.

General sales taxes are levied in 45 states plus the District of Columbia and Puerto Rico. They apply to items we purchase every day, including goods like furniture and automobiles and often also services such as car repairs and dry cleaning.

To compute sales tax, the price of a taxable item is multiplied by the tax rate. Many states also have local sales taxes which are added on top of the state tax. Local taxes usually apply to the same items as the state sales tax, but a few states give municipalities flexibility on which items to tax.

Separately, states also have excise taxes, such as taxes on cigarettes, alcohol, and utilities. Excise tax is often applied on a per-unit basis instead of as a percentage of the purchase price. For instance, cigarette excise taxes are calculated in cents per pack. And most gasoline excise taxes are levied in cents per gallon.

Progressivity

Sales taxes are often the primary reason why local taxes fall disproportionately on low- and middle-income families: sales tax applies at the same rate to everyone, but spending as a share of income falls as income rises. That means that low-income households end up paying more than double in sales taxes as a percentage of their income than upper-income families.

Due to the regressive nature of sales taxes, municipalities that aim to build a more progressive tax system ought to shift some of their revenue from sales and other taxes on consumption to other major sources more amenable to progressive interventions, like income or property taxes. This would not only mitigate regressivity but also protect local budgets from economic recessions, because when consumption drops, so do sales tax revenues.

Of course, sales taxes will continue to have a place as a major source of municipal revenue. They are an important component of a diversified revenue base, despite their regressivity, and should capture internet sales and sales of services to ensure similar transactions are not taxed differently. But localities can also advance progressivity in sales and excise taxes, such as by creating rebates, exemptions, or credits targeted at working families, and ensuring that sales tax revenues are dedicated to benefiting working families. In addition, sales and excise taxes that target certain categories of goods and services disproportionately bought by wealthy households and corporations—like a tax on luxury goods—can result in progressive revenue streams.

Progressive Sales Tax Policies

Levy luxury taxes. Luxury taxes can be placed on non-essential or expensive goods or services to ensure that wealthier consumers pay a fairer share of sales tax revenues. These can be structured either as a surcharge on top of regular sales taxes or as excise taxes targeting specific goods or services.

For example, a luxury tax can be placed on cars above a specific price, jewelry, furs, or other non-essential high-value items. As for services, luxury helicopter, private jet, or other charter transportation services may be worthwhile targets, not only on progressivity grounds but also on environmental and safety grounds. The challenge with a local luxury tax, however, is that these expensive commodities can often be obtained outside of the taxing jurisdiction.

End exemptions for data centers and other large businesses. Data center tax breaks are costing states and localities billions. Three states are each losing $1 billion or more per year to data centers: Virginia ($1.9b), Georgia ($2.5b), Texas ($3.2b). Others are close behind. And these are just the states that we know about: of the 32 states offering data center tax incentives, 14 fail to disclose aggregate revenue losses. These tax incentives often come in the form of sales tax exemptions on equipment and software upgrades. In one case, a New York county awarded JPMorganChase $77 million in tax exemptions in exchange for a single full-time job created by a data center development deal.

Given their overwhelming costs, Local Progress recommends taking action to halt hyperscale data center development. But where data centers have already been permitted, local governments should collect as much revenue from them as possible.

Levy tourism taxes. Taxing tourism activity is an efficient and politically feasible way for municipalities to ensure that visitors pay their share of public services so residents aren’t stuck with the full bill. Below are examples of these taxes and ways to maximize progressivity.

Examples of tourism taxes:

- Hotel taxes, also called transient occupancy, visitor, or bed taxes, are levied on consumers who rent rooms or other accommodations on a short-term basis. These may be structured as flat fees or as a percentage of the total cost of the stay. These taxes are primarily paid by non-residents. For equity reasons, hotel taxes should also be applied to the short-term rental market, including Airbnb and VRBO.

- Vehicle rental taxes are levied on car and truck rentals. Usually structured as a percentage of the cost of the rental, these taxes are paid primarily by visitors.

- Taxes on ridesharing services are a tax on the passenger who hails a rideshare. Taxis usually pay a tax or fee on medallions, but rideshare companies have often avoided paying medallion fees. Rideshare taxes can be a flat fee or a percentage of the cost of the ride. Rideshare taxes are paid by residents, commuters, and visitors.

- Parking fees, including metered spots and parking garages, can also generate revenues for cities. Many municipalities are not charging enough for the temporary use of public land and may be best served by raising meter fees.

- Restaurant taxes, often referred to as prepared food and beverage taxes, are taxes on eating out at restaurants, bars, and cafes paid directly by consumers.

How to maximize progressivity in tourism taxes:

- Charge higher rates for more expensive goods and services. For example, New York City has a progressive tax structure that charges a higher tax rate to pricier hotel rooms than cheaper rooms.

- Use a zone scheme. Targeting zones frequented by tourists, such as historic districts or downtowns, can help ensure things like tourism-related ridesharing taxes, increased parking fees, and restaurant taxes more efficiently target tourism activity rather than residents.

- Use seasonal tax rates. Destinations with highly seasonal tourism, such as summer towns or ski communities, could experiment with seasonal sales tax rates to more precisely target tourism. Municipalities in Alaska are testing these to capture the economic value from tourists who overwhelmingly visit in the summer months. South Dakota’s lodging and amusement taxes only apply from June through August.

Apply excise, or “sin taxes” on goods according to price. Excise taxes are often applied at a flat rate per unit to discourage the consumption of particular goods such as alcohol, tobacco, and soda. Although these taxes are somewhat effective in changing consumer behavior, these taxes tend to fall disproportionately on the poor who typically spend a higher percentage of their income on these products.

To make excise taxes more effective in deterring consumption and less regressive, the tax should be levied as a percentage of the price, rather than per unit. For example, high-end liquors should generate a higher sales tax liability than a case of standard beer. Excise taxes can potentially even be coupled with a luxury tax so more expensive products are charged at a higher rate of excise tax.

Earmark sales tax revenue for progressive purposes. Although raising progressive revenue from sales taxes is more difficult than through other tax types, municipalities can blunt the regressive effects of sales and excise taxes by earmarking revenues for programs that disproportionately benefit working families. State law often requires such earmarking before municipalities may institute new taxes.

Sample Policies

Luxury Taxes

Connecticut’s luxury tax – a 7.75% sales and use tax rate, instead of the 6.35% general rate, that generally applies to the total value of motor vehicles over $50,000; jewelry over $5,000; and clothing, footwear, and other specified goods over $1,000.

Canada’s Select Luxury Items Sales Tax, which applies to sales and leases of certain vehicles and aircraft with a purchase price over CAD $100,000 and certain boats with a purchase price over CAD $250,000.

Dedicating excise tax revenue to progressive ends

- San Francisco’s soda tax directs revenues from an excise tax on distributors of sugary beverages towards nutrition and food access programs targeted at underserved neighborhoods, public health initiatives aimed at reducing disease, grants to community-based organizations, and school meal and wellness programs.

- Washington State’s local sales tax for affordable housing permits cities and counties to levy up to a 0.1% sales tax on top of the statewide rate whose revenues are dedicated to affordable housing, typically going into housing trust funds supporting affordable housing construction and preservation and rental assistance.

Further reading

-

- ITEP Guide to State & Local Taxes: How Do State and Local Excise Taxes Work?, ITEP.

- Rita Jefferson, Travelers’ Checks: How to Tax Tourists in States and Localities, ITEP (Mar. 30, 2026) (includes a state-by-state list of what tourism-related tax powers are available locally).

Business Taxes

Overview

In many cases, the income taxes, property taxes, and sales taxes described above are actually collected and remitted by businesses. That does not necessarily mean that the business and its owners absorb all of the cost; rather, depending on the tax, a portion may be passed through to the employees and/or customers of the business. It can be appropriate to levy such taxes on businesses because businesses benefit from local government services.

Progressive Business Tax Policies

Limit Gross Receipts Taxes to Larger Businesses

Some localities levy gross receipts tax, sometimes called a Business and Occupation (B&O) tax, a business license tax, or a privilege tax. This is a tax on a business’s total revenue, without deductions for costs of goods sold, wages, or other business expenses. This is different from income-based taxes, since a business can be profitable or unprofitable and will still owe the same gross receipts tax if its revenues are the same. Rates are typically very low, sometimes fractions of a percent, to offset the broad base. Some jurisdictions use tiered rates by industry type (e.g., different rates for manufacturing, retail, services, and financial activities), recognizing that gross margins vary enormously across industries. States that allow some or all local governments to levy gross receipts taxes include California, Pennsylvania, Virginia, Washington, and West Virginia.

Localities may be able to reduce the impact of these taxes on smaller businesses whose owners may have less ability to pay by exempting businesses with gross receipts below a specific level and by applying higher rates to the largest businesses. San Francisco’s Gross Receipts Tax, for example, exempts businesses with less than $5 million in receipts, and Seattle’s B&O Tax has a $2 million threshold.

Levy Corporate Income Taxes

Only a limited group of municipalities are allowed to tax business or corporate incomes directly. Cities in Michigan, Missouri, Ohio, and Pennsylvania, as well as New York City and Washington, D.C., are allowed to tax corporate incomes. These have many names, including business corporation taxes, business franchise taxes, net profits taxes, or profit taxes.

Institute Payroll Expense Taxes

One straightforward way to tax businesses is through payroll expense taxes. These are any tax on the total amount of income a company pays to employees. These taxes are easily made progressive by exempting lower-income employees and only applying to higher-income ones. Depending on the applicability of state uniformity clauses, cities may also be able to exempt small businesses, or businesses with few employees from the tax.

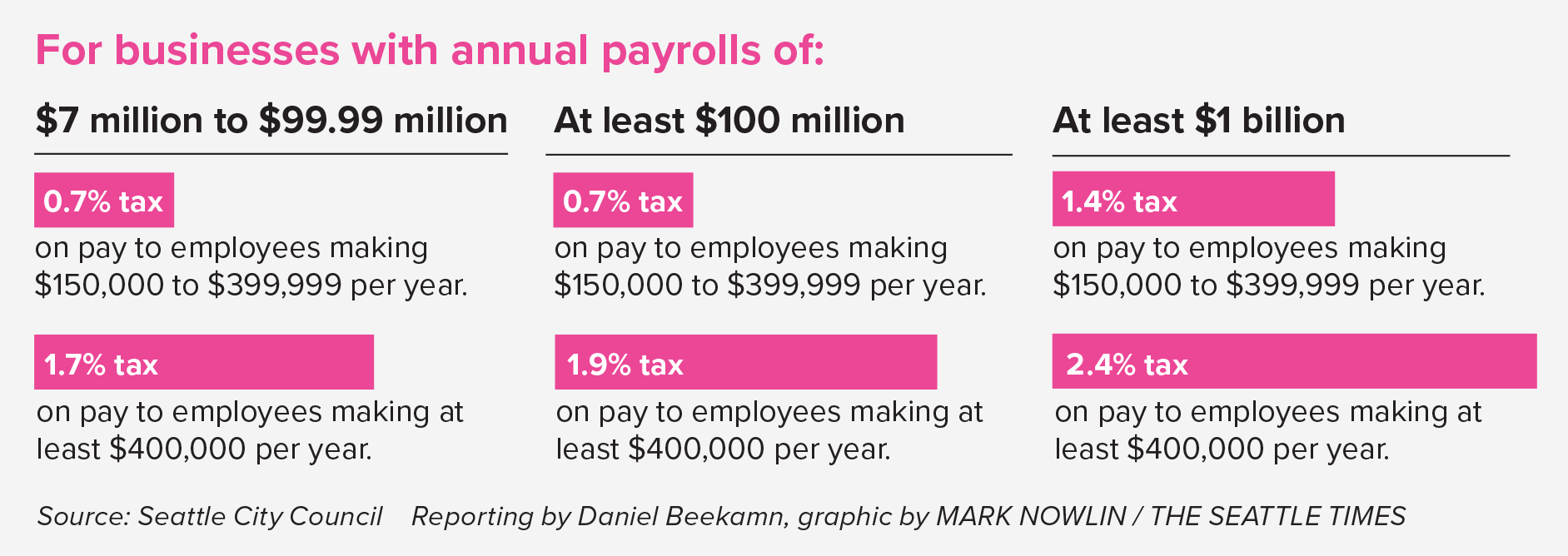

Case Study: Seattle’s Payroll Tax

Overview

JumpStart Seattle is a progressive payroll tax passed in response to COVID-19’s economic impacts on Seattle. JumpStart taxes the largest and wealthiest companies on highest salaries within those companies. The initial rate structures are set out below and have since been adjusted annually for inflation.

Notably, JumpStart is designed to protect small firms and low- and middle-income earners. Businesses with less than $7 million of annual Seattle payroll are not taxed, meaning the vast majority of Seattle businesses are exempt. And because larger businesses only pay the tax on high earners, it is more likely to protect lower-income people working for large corporations, especially those working at large retail or food service jobs.

Former Seattle Councilmember and current King County Councilmember Teresa Mosqueda explains, “This was intentional in a post-Covid context, where certain companies actually profited from the pandemic while other small business and service sector employers struggled to survive.”

JumpStart has generated badly-needed progressive revenue in the most prosperous city in Washington, which has the second-most regressive tax structure of all states. JumpStart generated $315 million in 2023 and $360 million in 2024.

Seattle’s payroll expense tax first provided immediate Covid relief to Seattle families and public programs, and now supports local affordable housing development, small business development, local Green New Deal programs, and the city’s general fund.

The Lead-Up to JumpStart

JumpStart passed after a very public rollback of an Employee Hours Tax (a head tax) in 2018, with many believing it was impossible to levy a progressive businesses tax. The Employee Hours Tax failed because it was a tax on all Seattle businesses, including some small businesses like grocery stores. This made it easier for the business community to organize to defeat the tax with the threat of putting it on the ballot. What made JumpStart different is its narrow targeting of big businesses with high-earning employees. It also earmarked millions of dollars in Covid relief funding for the very small businesses the head tax had included.

Seattle had tried to pass its own income tax on wealthy households, but that was defeated in court. In addition, there was a state legislative effort to pass a progressive business tax in 2018, but that also failed to gain enough momentum for a vote.

Collaborative Governance in Action

Community advocates called on former Councilmember At-Large Teresa Mosqueda’s office to work on a progressive revenue source to fund much-needed supports and community services. Community advocates worked to identify spending priorities and policy levers for the tax. Part of JumpStart’s tremendous success was thanks to the unique alliance of community organizations and traditional opponents, including big businesses that would be taxed like Expedia, who came to the table to secure the largest progressive business tax the city has seen in decades.

The JumpStart plan was built over three months with a coalition of labor unions; small and large businesses; and community advocates from 100+ nonprofits representing immigrant and refugee rights organizations, transportation and environmental advocates, neighborhood groups, equity-based organizations, food security advocates, and housing and homelessness advocates. The campaign involved thousands of hours of engagement with stakeholders, policy development, and strategic communications.

The decisions on spending were made by a large group of community advocates. There was consensus that while long-term the progressive tax should fund affordable housing, equitable development and small business supports, in the short-term the spending plan needed to prioritize direct assistance to Seattle families suffering from the immediate impacts of the Covid-19 economic crisis.

Despite finding itself in opposition to the mayor on certain issues, the Seattle City Council at the time was firmly in support of JumpStart due to the dire need for funding to maintain services during Covid-19. Because personal income taxes are prohibited by state law, local leaders instead selected a payroll tax and passed this innovative tax through the City Council.

Adapted from Dare to Reimagine: JumpStart the Local Economy, Local Progress (2021).

Tax Big Tech. There are also emerging, innovative opportunities to tax the digital economy. Despite being some of the most valuable companies in the U.S., mega-corporations like Amazon, NVIDIA, and Meta pay almost nothing in federal taxes, and despite the fact that they are deeply embedded in the economies of nearly every community, most localities do not tax them at all. As tech companies, social media companies, and AI companies make billions off the personal information of residents and businesses, localities should tax them to ensure they pay their fair share of local services and the tremendous social costs of their business activities.

Tax Internet Betting and Prediction Markets. The rise of sports betting, internet gaming, and speculative wagers on prediction markets represent new opportunities to both raise revenue and curb predatory business activity. In states where gambling is permitted, localities should tax businesses generating revenue from such betting activity (although whether states and localities are even allowed to tax and regulate prediction markets is currently under litigation). Care must be taken not to allow the desire for gaming revenues to overwhelm localities’ obligations to protect their residents from a deeply exploitative industry, especially because experience shows that gambling revenues are a poor long-term funding source.

Example: Chicago Sports Wagering Tax.

Case Study: Chicago’s Tech Taxes

Overview

In 2025, Chicago expanded and enacted three taxes that apply to different parts of the digital economy.

First, Chicago uses a cloud computing tax. Originally enacted in 2015 and increased to a rate of 15% in 2025, the cloud computing tax is structured like a lease tax on the use of certain computer software as a service (SaaS) tools like Salesforce. This ensures that businesses operating mostly or entirely digitally are also paying city taxes that are owed by companies more reliant on physical goods.

Second, Chicago expanded its existing amusement tax to apply to social media companies who monetize users’ personal data. Companies with more than 100,000 monthly users in Chicago will pay 50 cents per user per month. Revenues will go towards community youth mental healthcare, connecting the social costs of social media with a direct funding stream to protect users.

Third, Chicago also expanded its amusement tax to capture mobile and online sports wagering—in addition to in-person wagering, which was already being taxed—and increased the tax rate from 2% to 10.25% for all types of sports wagering.

Tech companies accustomed to not paying their fair share are filing legal challenges to taxes on the digital economy, including Chicago’s online sports betting tax. As novel tax law questions work their way through the courts, local leaders can nevertheless take a stand by pursuing vetted, reasonable taxes on the digital economy to fund essential public goods.

The Lead-Up to Chicago’s Tech Taxes

As Jung Yoon, Chief of Policy for the Office of the Mayor of Chicago, explains, “[w]hen Mayor Johnson took office, Chicago was facing a massive structural deficit – the direct result of decades of bad policies from previous mayors including pension mismanagement and the notorious sale of our public assets like parking meters. Chicago is also prevented from levying a wide variety of common-sense progressive revenues with a state constitution that pre-empts graduated taxes.”

To realize the mayor’s vision of making Chicago “the safest, most affordable big city in the country,” the mayor’s office “engaged in extensive research to identify progressive revenue policy proposals, working closely with our budget, finance, and legal team to ensure the taxes were legal and implementable,” explains Yoon.

As with any progressive tax, challenges were expected. In anticipation of challenges to the Social Media Amusement & Responsibility (SMART) Tax, the Mayor’s Office conducted extensive research into similar cases nationwide. According to Yoon, that “allow[ed] us to draft an ordinance that avoids the legal vulnerabilities seen elsewhere.”

The SMART Tax legislation ensures that its revenues are dedicated to Chicago’s public health infrastructure. Yoon adds, “We also did not budget any expenditures for 2026 on the SMART Tax, but instead established a special revenue fund, known as the “Protecting CARE Fund” to expand our public mental health and crisis intervention programs in 2027 and beyond.”

Collaborative Governance in Action

Development and enactment of Chicago’s tech taxes was a citywide effort grounded in collaborative governance. Interbranch coordination with the City Council was key, as the Mayor’s Office collected feedback on revenue ideas from alders. Outside of City Hall, the Mayor’s Office invited residents to shape the proposals through virtual public comment, multiple budget engagement roundtables, and town halls. It also worked with community organizations and policy advocates to solicit ideas and refine each tax proposal to ensure the final package was both stronger and more responsive to public needs. Following passage of Chicago’s tech taxes, the State of Illinois mirrored the city’s SMART Tax and introduced a statewide version of the legislation.

Further Reading

-

- Zach Schiller and Carl Davis, Taxes and the On-Demand Economy, ITEP (Mar. 15, 2017).

- Institute for the Public Good, The Chicago SMART Tax Pathways to Recouping Big Tech Tax Avoidance (Mar. 2026).

- Tazra Mitchell, Erica Williams, and Nick Johnson, A Business Activity Tax Would Make DC’s Tax System More Equitable While Raising Revenue, DC Fiscal Policy Institute (Jan. 30, 2025).

Progressive Fees and Well-Structured Fines

Overview

As the costs of basics have quickly risen over the last decade, so too have the household costs of municipal service fees for things like water and sewage, electricity, sidewalks, and waste. Studies indicate that some of these have become more regressive over the last several years as providers have moved to more fixed fees instead of volume-based pricing.

In contrast to the many obstacles around taxes, municipalities typically have broad authority to set fees for municipal services. Local action to make municipal service fees more progressive is thus essential to help reduce the cost of living for working people. Local Progress has previously written about how to make common fees for municipal services more progressive and how to structure new fees to ensure municipal services are paid for by those who bear most responsibility for their cost.

This section does not discuss justice system fines and fees, which disproportionately harm low-income households and communities of color. Local officials should under no circumstances rely on law enforcement or justice system fees to fund local budgets, as it incentivizes overpolicing and causes tremendous damage to people’s lives. For more on reducing reliance on fines and fees, please visit the Fines and Fees Justice Center.

This section will highlight high-level progressive approaches to fines and fees and a promising new fee type in the U.S.: congestion pricing.

Progressive Fine and Fee Policies

Make fines income-based. Income-based fines (also called “day fines,” “unit fines,” or “structured fines”) currently exist in varying forms in several European countries and were tested in various U.S. jurisdictions in the 1980s and 90s. By making a higher-income individual or business pay a higher fine than a lower-income one violating the same law, day fines increase accountability, deterrence, and fairness. In addition, day fines can result in a more efficient use of resources (e.g., if they offset prison sentences) and can raise revenue. In the U.S., day fines may also reduce the financial incentives for criminalizing poverty and over-policing communities of color.

Use tiered payment structures. Local governments can charge tiered rates depending on usage volume and customer type for things like water and waste. These charge bigger users like businesses more and residents less. Example: Durham, North Carolina.

Offer repayment assistance. To alleviate the impact of fines and fees on working people while ensuring continued provision of essential services, localities can create payment plans for late payments or utility debts—or outright forgive them for working people. Such repayment plans can offer lower or zero interest rates on the payments.

Implement congestion pricing. Congestion pricing charges drivers a fee to use certain roads or enter specific busy areas during peak periods. While congestion pricing was primarily conceived of as an economic tool to force drivers to internalize the costs of high traffic on public roads and thereby reduce pollution and increase travel speeds, it also has significant revenue potential. New York City’s congestion pricing scheme, which charges drivers entering Manhattan’s core, has proven to be a success, generating $562 million in its first year and reducing pollution and traffic.

Demographic data from NYC suggests that broad-based congestion pricing—i.e., charging all drivers in the congestion zone the same fee—does not have particularly regressive effects. On the contrary, higher-income drivers are more likely to pay congestion charges, while lower-income individuals are more likely to use public transit and can benefit disproportionately from faster and better-funded transit systems. For working people who must travel by car into a congestion zone, local governments can include discounts or exemptions targeted at lower-income drivers. Congestion pricing can be even more progressive by charging a special surcharge for trips via rideshares and autonomous vehicles.

Local governments usually cannot implement congestion pricing on their own and will often need state authorization and, when federal highways or funding are involved, approval from the Federal Highway Administration. Another major concern is privacy: some congestion pricing systems rely on automated license plate readers (ALPRs), which expose drivers to surveillance by state actors. Local governments should take steps to mitigate privacy issues by using alternative technologies or by using the least intrusive means of data collection possible, for example, by limiting data disclosure, limiting the types of data collected and for how long, and ensuring data security.

Further Reading

-

- Lillian Patil & Dr. Marshall L. White, The Cost We No Longer Pay: How Fine and Fee Reform Delivered Billions in Relief for Families, Fines And Fees Justice Center (Apr. 2026).

- Shawn Sebastian & Karl Kumodzi, Progressive Policies for Raising Municipal Revenue, Local Progress (Apr. 2015).

VI. Evening the Scales: Tax Assistance for Working Families

Tax systems can be used not only to raise important revenues for schools, roads, and other services, but also to deliver assistance directly to taxpayers. As localities look to provide a stronger foundation for families and communities to thrive, well-designed local refundable credits are an effective and proven option. Substantial evidence on these credits at the federal, state, and local level illustrates why: having inadequate resources holds people and communities back. By directly bolstering households’ resources, refundable credits help workers and families get by and achieve their potential. The results are stronger outcomes and greater equity in health, education, employment, and more. Below are some common examples that exist at various levels of government.

Income Taxes: Earned Income Tax Credits

Earned Income Tax Credits (EITCs) support low and moderate-income people who have earnings from work at some point during the tax year. Most of the benefits go to families with children, but workers without children also benefit. New York City, Philadelphia, and Montgomery County, Maryland have local EITCs integrated into the local income tax system. But it’s not necessary to have a local income tax to have an EITC. Cities without a local income tax can piggyback on federal or state credits; San Francisco used American Rescue Plan Act funds to pilot a local EITC.

Tax Support for Working Families: Local Child Tax Credits

Child Tax Credits (CTCs) provide financial support for children up to specified income levels. Child tax credits also have the power to substantially reduce child poverty. A recent report from ITEP and the Center on Poverty and Social Policy at Columbia University detailed how 12 cities could cut child poverty in half with a local CTC.

Property Taxes: Circuit Breakers, Classification, and Homestead Exemptions

Circuit Breakers: Property tax circuit breakers support low-income homeowners and renters who may have a difficult time affording property taxes. Some places target circuit breakers just to seniors under the logic that many seniors are on fixed incomes; others make them available to all residents. The city of Hialeah, Florida recently created a circuit breaker for seniors that refunded an average of over $500 to qualifying low-income homeowners.

To advance progressivity, these programs must be refundable, meaning that if the credit amount exceeds what a family owes in income taxes, it receives the difference as a refund.

Classification: Property classification is a tool used to tax different types of property owners at different rates. This can help improve property tax progressivity by taxing properties used commercially at higher rates than properties used as residences. While some states’ uniformity clauses preclude the ability for localities to use classification, other states restrict it to certain localities or large counties, like New York City or Cook County, Illinois. The most comprehensive statewide classification scheme is in Montana. Properties in the state are taxed at different rates depending on use. This has allowed localities to tax homeowners at a lower rate than many commercial properties, and has recently enabled the state to adopt a tax on second homes.