Key Findings

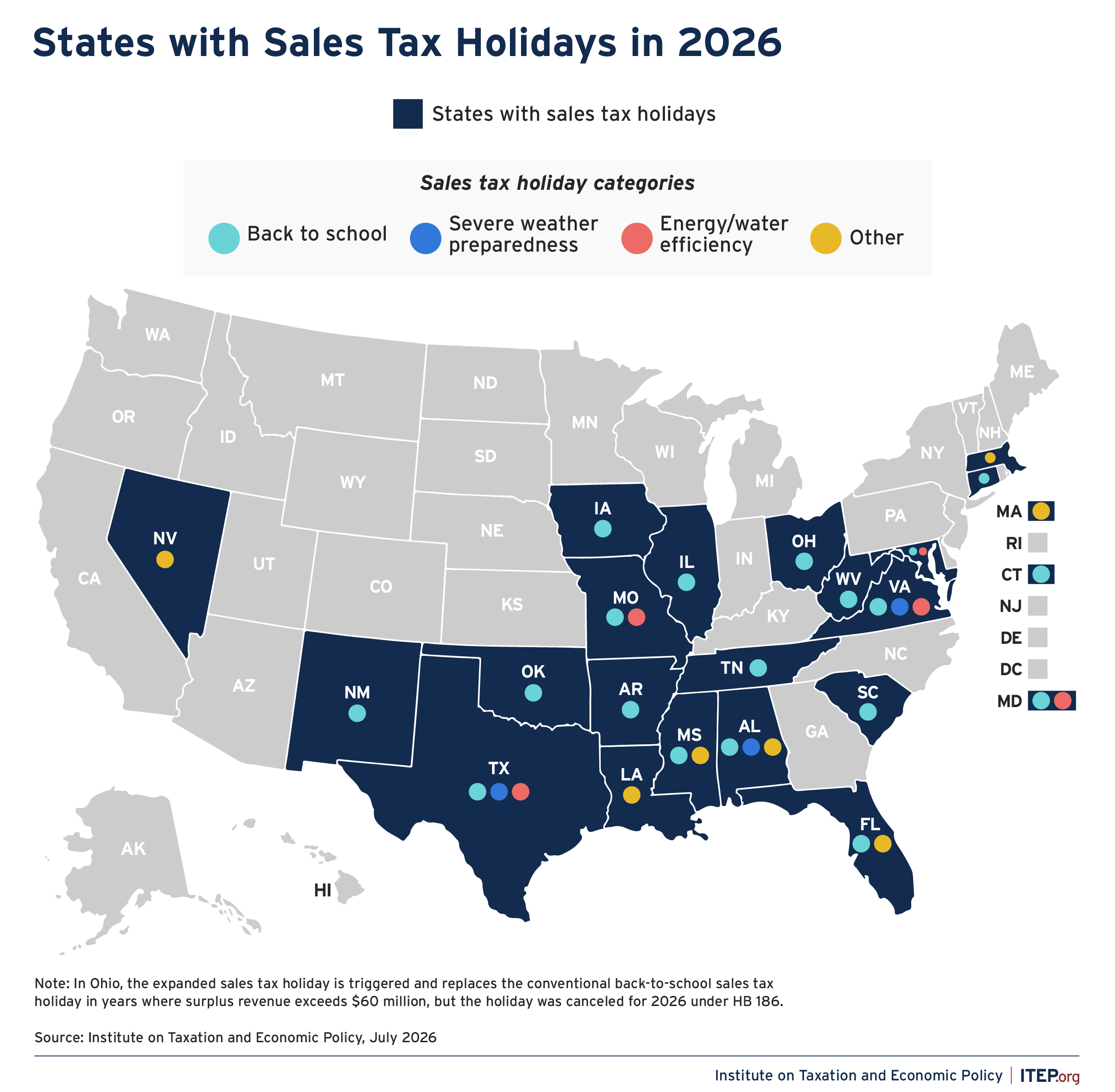

- Twenty states have sales tax holidays on the books in 2026, two more than last year as Alabama and Illinois enacted temporary, one-time sales tax holidays.

- These sales tax holidays will cost states and localities nearly $600 million in lost revenue this year.

- Sales tax holidays are poorly targeted and too temporary to meaningfully change the regressive nature of a state’s tax system.

- Overall, the benefits of sales tax holidays are minimal while their downsides are significant. Low- and moderate-income people would be better served by lawmakers pursuing targeted tax credits, such as low-income sales tax credits, Child Tax Credits, and Earned Income Tax Credits, or by making a meaningful shift in their systems to less reliance on sales tax and more reliance on more progressive forms of taxation like income taxes and corporate taxes.

Sales taxes are an important revenue source, making up close to half of all state tax revenues. But sales taxes also are inherently regressive because low-income families spend a greater share of their income on goods and services subject to the tax.

Lawmakers in many states have enacted “sales tax holidays” to temporarily suspend the tax on purchases of clothing, school supplies, or other items. While lawmakers often tout sales tax holidays as a way to benefit everyday households, especially as household budgets continue to be squeezed by inflation, this approach falls short of alleviating the regressive nature of sales taxes on low- and middle-income households and tends to bolster political profiles with a highly visible but short-lived tax cut in lieu of more meaningful, permanent reform. Instead, the holidays arbitrarily reward people with specific hobbies or in certain professions while simultaneously reducing state revenues and creating administrative burdens.

Twenty states have sales tax holidays on the books in 2026, two more than last year. The combined annual cost to state and local budgets this year is estimated to be around $600 million. Nationwide, we saw two states, Alabama and Illinois, enact one-time sales tax holidays, both of which notably coincide with election cycles. Another state, Ohio, downsized its sales tax holiday after a major expansion in 2025.

Figure 1

Alabama legislators passed a two-month suspension of the state’s 2 percent sales tax on groceries from May 1 to June 30, which coincided with the state’s primary and primary runoff elections. Alabama is one of 13 states that taxes groceries and was one of only three states that fully levied its sales tax on groceries until 2023.

As Illinois Gov. JB Pritzker seeks a third term, Pritzker signed the state’s 2027 budget that included a one-time, back-to-school sales tax holiday for 10 days in August. During the holiday, the sales tax rate for qualifying clothing and school supplies will be reduced from 6.25 percent to 1.25 percent and is estimated to cost the state $10 million in lost revenue. The last time Illinois enacted a sales tax holiday was in 2022, when Pritzker was seeking a second term.

Ohio is reverting to its three-day back-to-school tax holiday this year after lawmakers canceled the expanded sales tax holiday and redirected the funds allocated for the holiday towards property tax cut legislation. While the state’s traditional sales tax holiday is limited to back-to-school items, the expanded holiday in 2025 lasted two weeks, applied to nearly all products priced at $500 or less, and cost the state $124 million in lost revenue. Lawmakers made the right choice in reducing the scope this year.

How Sales Tax Holidays Work

Sales tax holidays are temporary sales tax exemptions, usually applying to a small number of taxable items for a very limited period. They are typically timed to take place in August during the traditional back-to-school shopping season and usually offer breaks on school-related items such as clothing, school supplies, and computers. A few states exempt all taxable goods during the suspension. Most sales tax holidays last only two or three days, and almost all apply only to items below some specified price (for example, clothing items over $100 are generally not included).

In addition to traditional back-to-school weekend holidays, some states now have longer, broader exemptions with varying themes. Holidays for energy-efficient appliances and storm preparation materials are becoming increasingly common, for example. In 2026, there are also holidays being held for hunting and fishing activities in Florida and for National Guard members and their families in Nevada.

History of Sales Tax Holidays

The notion of such a holiday was first introduced in 1980 when Ohio and Michigan opted to not tax the sale of automobiles for a period of time. New York experimented with the current concept of sales tax holidays in 1996 but has since reversed the policy. More than 20 states have enacted legislation since 1980 at some point to temporarily suspend sales taxes, and proposals to extend the concept to more states and more types of purchases appear every year.

Many states have repealed or temporarily ended sales tax holidays when facing significant revenue gaps. For example, lawmakers in Florida, Georgia, Maryland, Massachusetts, and the District of Columbia all canceled holidays during the height of the Great Recession. Although most of these reinstituted them afterward, Georgia and D.C.’s holidays have not been revived. Louisiana, which once held three separate exemptions for back-to-school shopping, hunting season, and hurricane preparedness, started paring them back due to revenue shortfalls in 2016 and only recently revived its holiday for hunting season. Holidays in New York, North Carolina, Vermont, and Wisconsin were also either short-lived or repealed.

Problems with Sales Tax Holidays

Sales taxes are inherently regressive. Policymakers tout sales tax holidays as a way for families to save money while shopping for “essential” goods. On the surface, this sounds reasonable. However, a two- to three-day sales-tax-free shopping spree for selected items does nothing to reduce taxes for low- and moderate-income taxpayers during the other 362 days of the year. In the long run, sales tax holidays leave a regressive tax system unchanged, and the benefits of these holidays for working families are minimal. These temporary exemptions also fall short because they are poorly targeted, reduce revenue, can easily be exploited, and create administrative difficulties.

Sales Tax Holidays are Poorly Targeted

While lawmakers tout sales tax holidays as a way to benefit everyday households, these holidays are poorly targeted and discriminate among taxpayers.

Wealthier taxpayers are often best positioned to benefit from a temporary sales tax exemption since they have more flexibility to shift the timing of their purchases to take advantage of the tax break—an option that isn’t available to families living paycheck to paycheck.

Many low-income taxpayers spend most or all their income just getting by, which means that they have less disposable income than wealthier taxpayers to spend when a tax-free period arrives. One study found households that earn more than $30,000 (which would be about $50,000 when adjusted for inflation today) were likely to shift the timing of clothing purchases to coincide with a sales tax suspension, but households earning less than $30,000 were not.

This is more pronounced during economic downturns because low-income families or those who lose jobs see a much bigger hit to their incomes and generally recover more slowly. For families whose incomes are reduced or volatile for several years coming out of a downturn, a temporary sales tax suspension doesn’t relieve the monthly challenges associated with a regressive tax system that depends on a sales tax. Sales tax holidays are also not limited to state residents but instead extend to anybody who happens to be within the state’s borders at the time of the tax suspension, including tourists and people from other states who live close to the border.

Product-specific sales tax exemptions are also poorly targeted as certain taxpayers may not need the included products. For example, families with younger children, childless households, and seniors may not have the need to purchase products included in a back-to-school sales tax holiday. Similarly, an outdoor recreation sales tax holiday excludes households that do not participate in these hobbies or don’t have the financial resources to do so.

Finally, though the holidays are often marketed as boons to local businesses, nearly all sales tax holidays apply to online purchases—even those shipped from other states—giving no advantage to locally owned businesses.

Sales Tax Holidays Reduce Revenue

In 2026, sales tax holidays will cost states and localities about $600 million in lost revenue. This will ultimately have to be made up elsewhere, either through painful spending cuts or increasing other taxes. Cities and counties—which often have few revenue options and must rely on sales taxes to fund important priorities like roads, parks, police, and fire protection[i]—rarely have a choice in the matter of sales tax holidays. Only Alabama, Mississippi, and Missouri allow localities to opt out of them.

Moreover, now that most online sales are subject to state and local sales taxes (as they should be), the cost of these temporary suspensions has grown. Online purchases, which are tax exempt under all but one of these holidays, are a large and growing share of retail sales, and consumers can more easily time online purchases to coincide with a tax-free period than they can with brick-and-mortar purchases.

Out-of-state visitors also stand to benefit from these tax holidays at the expense of state revenue. If a state with a sales tax holiday abuts a state that chooses to not to enact such measures or enacts it on different dates, shoppers may cross borders to purchase products in the lower-taxed state. This results in states with the holiday providing a tax benefit to nonresidents, while sacrificing revenue that could be used to invest in their own residents.

Lawmakers’ recent experiments with longer and broader tax suspensions have added to this growing price tag, heightening the need to better understand why sales tax holidays are ineffective and how states can do more with less through more targeted policies.

Right now, these reductions in revenue will be particularly painful, with states facing the fallout of the recently passed federal tax and spending package that will shift many costs to states, economic uncertainty from the Trump administration‘s unpredictable tariffs and trade wars, and more.

Some Retailers Exploit Sales Tax Holidays

Retailers can also take advantage of the shift in the timing of consumer purchases by increasing their prices or watering down their sales promotions during the tax holiday. The influx of shoppers gives them an economic incentive to do so, and the evidence suggests that they often do. One study of retailers’ behavior in Florida, for example, found that up to 20 percent of the price cut consumers thought they were receiving from the state’s sales tax holiday was reclaimed by retailers.

Sales Tax Holidays Create Administrative Difficulties

Sales tax holidays create administrative difficulties for state and local governments and for retailers who must collect the tax. For example, exempting groceries requires a collection of well-defined government regulations to police the border between non-taxable groceries and taxable snack food – and only for a certain defined period of time. A temporary exemption for clothing (or for any other back-to-school item) requires retailers and tax administrators to wade through administrative changes for an exemption that lasts only a few days. Further complexity can arise in states with local sales taxes when some localities opt not to participate in the holiday and consumers unexpectedly end up paying local sales taxes on their purchases.

Better Alternatives to Sales Tax Holidays

Given these shortcomings and mirage of tax benefits from sales tax holidays, lawmakers should stop pursuing these gimmicky acts and instead focus on programs that provide better targeted, meaningful boosts to families’ budgets.

The best approach is to have a permanent progressive tax system that relies primarily on income taxes and corporate income taxes that fall most heavily on those most able to pay, and that permanently reduces regressive sales taxes across the board.

Since sales taxes cause low-income households to pay more of their overall income in taxes than high-income households, one of the strongest tools to improve fairness in tax policy is through targeted tax credits, like low-income sales tax credits, state earned income tax credits, or child tax credits.

These credits can be targeted to in-state residents and income groups most in need of tax relief and do not affect the sales tax base or long-term growth of sales tax revenue. Making these credits refundable is an essential component as it allows taxpayers with little or no income tax liability who pay a substantial portion of their income in sales taxes to still receive relief from the inherent regressivity of sales taxes.

Conclusion

Sales tax holidays are poorly targeted and too temporary to meaningfully change the regressive nature of a state’s tax system. Lawmakers must understand that they cannot resolve the unfairness of sales taxes simply by offering a short break from paying them. If the long-term consequence of sales tax holidays is a higher sales tax rate, low-income taxpayers may ultimately be worse off because of these policies. Policymakers seeking greater tax fairness would do better to shift from sales taxes to income and corporate taxes, or to provide a permanent refundable low-income sales tax credit, state-level child tax credit, or earned income tax credit. All of these would do more to help families make ends meet and to offset the impact of the sales tax on low- and moderate-income taxpayers.