Summary

- States have for many years exempted advertising from state and local sales taxes, but these exemptions should be reconsidered, for two main reasons:

- Advertising is a major financing mechanism for the consumption of goods and services like newspapers, television, internet searches, and social media. So states should tax advertising for the same reason they tax forms of consumption that are purchased directly: as a broad-based, reasonably fair way to raise much-needed revenues to fund public services.

- Most advertising today takes the form of targeted or programmatic ads, largely flowing through electronic platforms controlled by a few gigantic corporations. This advertising funds social media and other online services — services which are increasingly associated with harms to mental health, the demise of local journalism, and other problems. If they don’t tax advertising, states are implicitly subsidizing a sector of the economy that is creating demonstrable social costs.

- Utah and Washington have recently joined Hawaiʻi, Maryland, and New Mexico in taxing some or all advertising sales, although the details of how the taxes operate vary. If all other states taxed either targeted advertising, or all advertising, at rates comparable to current sales taxes that they levy on other forms of consumption, they could collectively raise roughly $16 billion to $27 billion a year.

- Some of these taxes have been challenged in court as violations of the federal Internet Tax Freedom Act (ITFA), which bars discriminatory taxes on internet-based advertising. But there is reason to hope that courts will find all or most of these taxes to be compliant with ITFA, since these important state revenue laws should be presumed to be constitutional and were generally carefully drafted to comply with preexisting law.

- How these taxes will affect consumers’ pocketbooks or corporate profits is not entirely clear. The taxes generally are assessed based on where the advertisements are used or viewed. The economic incidence of these taxes will fall on some combination of advertisers, advertising platforms, and end users. Since low- and middle-income consumers in most states already pay more than their share of state and local taxes, states may want to use a portion of the revenue to fund other tax provisions, like state Child Tax Credits, that support low- and middle-income families. Meanwhile, given the enormous profits and wealth arising from targeted advertising, states should continue to explore additional ways to fairly tax those profits and wealth.

Exempting All Advertising Sales from State Taxation No Longer Makes Sense in the Big-Data Economy

Sales and excise taxes are a major way that state and local governments fund public services such as schools, hospitals, and roads. Most states levy state and/or local general sales taxes, every state taxes the purchases of cigarettes and alcohol, and a few states have gross receipts taxes on businesses’ total sales.

These taxes are largely levied on consumer purchases, but they apply to many purchases by businesses, too. Academic and industry studies have consistently found that states collect, on average, around 40 percent of their sales taxes on business-to-business purchases.

It’s common, however, for states that levy a sales tax on goods to exempt from taxation the purchase of services. Most general sales tax laws were enacted in the 1930s, 1940s, and 1950s — a time when tangible goods made up the vast majority of consumption, and when it would have been administratively difficult to tax services.1 The economic context today has flipped, so that service industries are a much larger share of the economy and much easier to tax. Nonetheless, states still tend to tax goods but generally not services, except for specific services they add to the tax base.

Advertising is an example of a service that has long been exempt from nearly every state’s sales tax. In the last two decades, however, the entire field of advertising has changed, with profound impacts on consumers, so it is worth reconsidering whether this exemption is still sound policy (if it ever was).

The big change is that most advertising today is delivered to individual consumers based on data about their characteristics, behaviors, or interests, rather than showing the same ad to everyone. Such targeted advertising has not only displaced most traditional advertising, but it is also one of the fastest-growing segments of the economy.

Targeted advertising based on individual data is not entirely new – think about direct mail – but it has expanded enormously in the Information Age because companies can easily collect vast amounts of information on consumers and use that data to develop new ways to predict and influence their behavior.2 Because this practice is most valuable to the companies that can accumulate massive amounts of data and use that data over time to increase the power of the algorithms, it is not surprising that it has become concentrated in the hands of a small number of companies that wield a great deal of economic power.

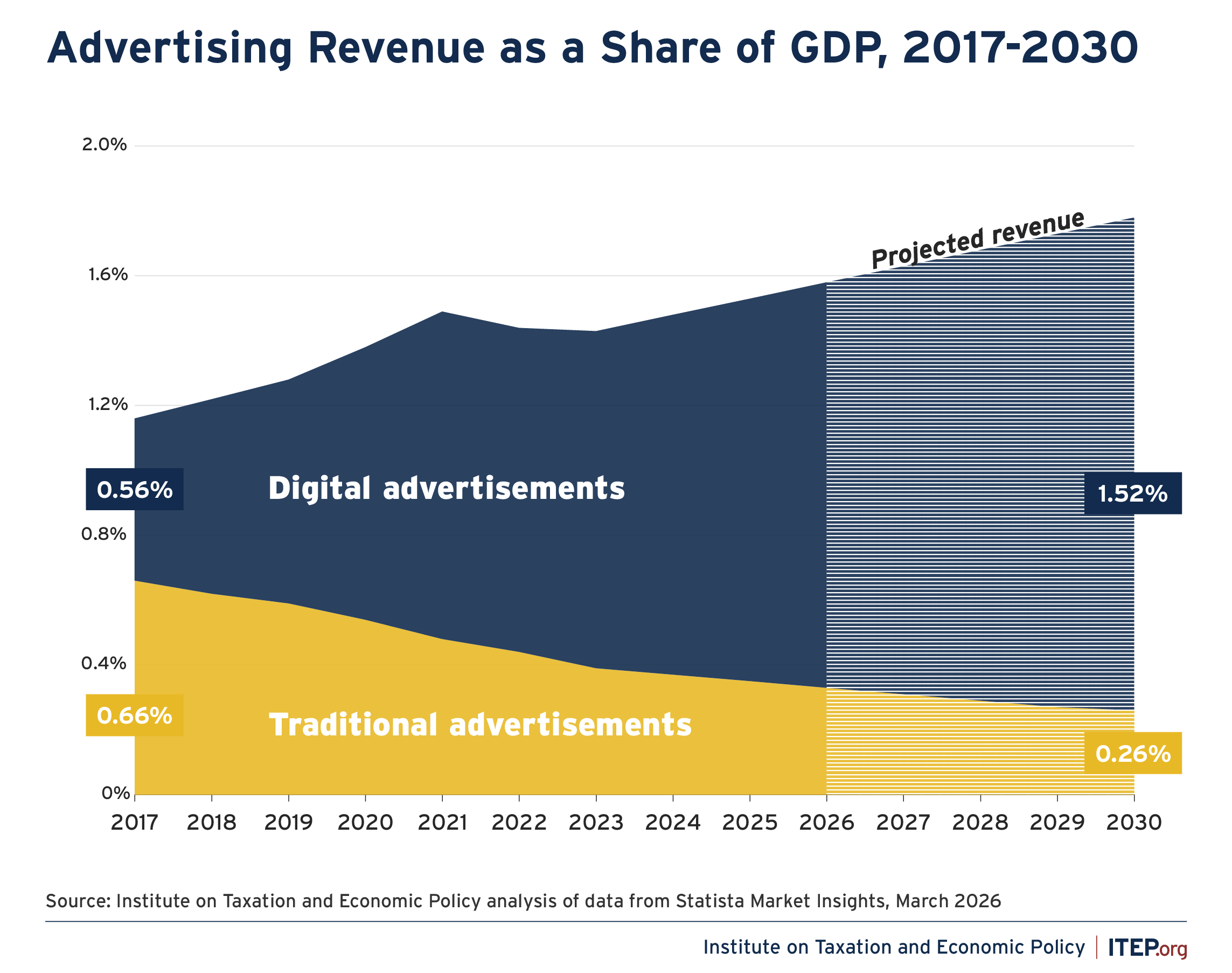

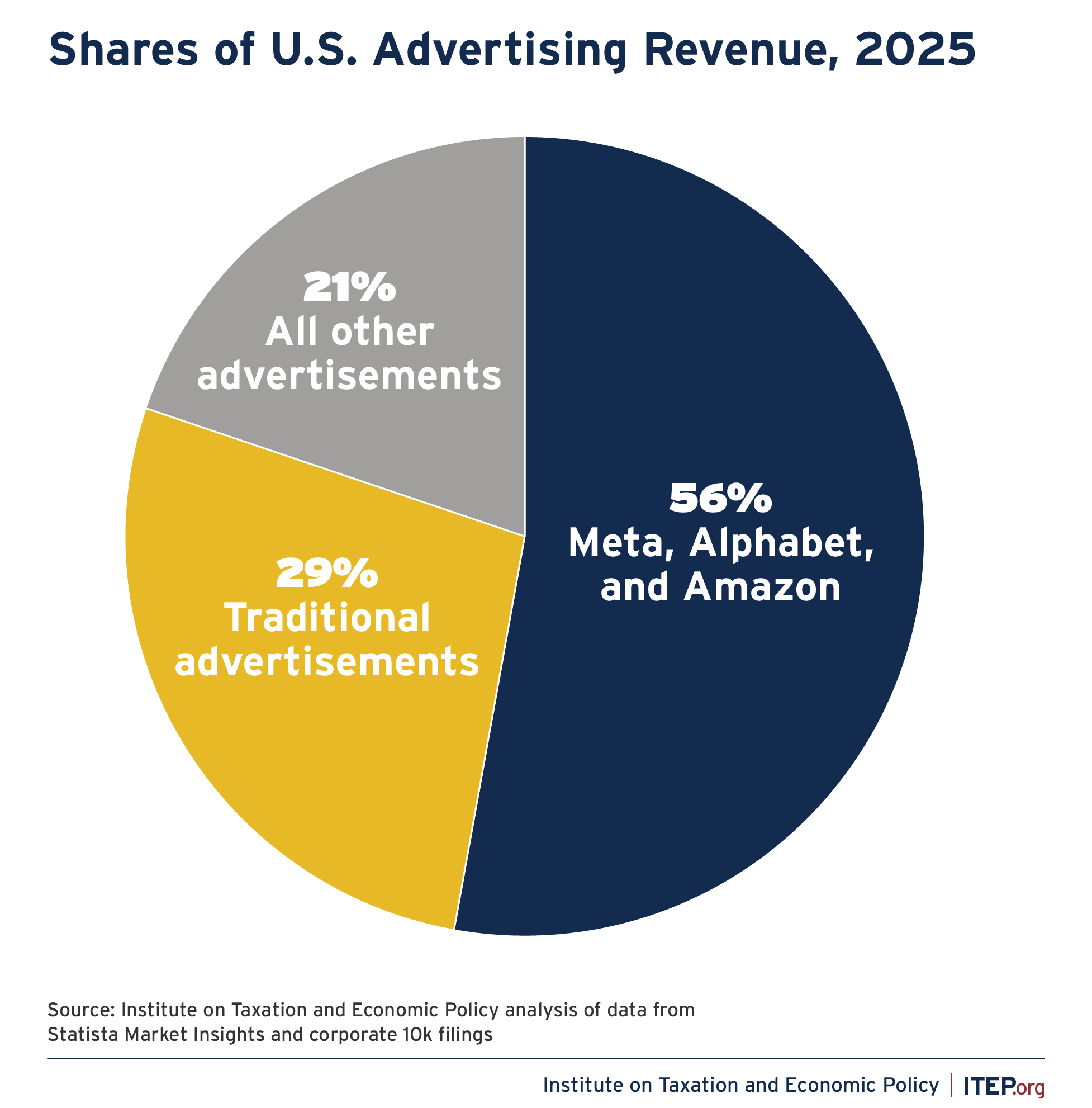

Over half of all U.S. advertising dollars now flow through just three massive technology companies: Alphabet (which owns Google and YouTube), Meta (Facebook and Instagram), and, to a lesser extent, Amazon. Those companies took in about $250 billion in 2025 in U.S. ad sales – an amount equal to 1.2 percent of U.S. consumers’ total purchases and about 56 percent of all U.S. advertising.3 Traditional media such as television, radio, newspapers, and direct mail account for roughly one in four U.S. advertising dollars, with the fraction dropping every second.

Figure 1

Exempting Advertising Is Costly to States

States’ longstanding tax exemption for advertising may once have been defensible at least in part as a subsidy to locally owned newspapers, television stations, and the like. But that exemption now is mostly a transfer of billions of dollars away from funds for schools, health care, and roads and into the pockets of Alphabet, Meta, Amazon, and other very large companies. As discussed further below and shown in Table 1, if states extended their sales taxes to advertising in general or more narrowly to targeted forms of advertising, they could raise $16 billion to $27 billion a year. Local governments, whose sales tax bases typically reflect the state tax base, could receive billions more from the inclusion of advertising, depending on the design of the tax.

Figure 2

Ad Taxes Level the Playing Field with Other Forms of Consumption

One argument for exempting advertising has long been that advertising is a business input rather than a consumer expenditure. Sales taxes are often framed as taxes on final consumption, and while no state exempts all business inputs, all states exempt at least some. One reason to exempt business inputs is that sales taxes on an input typically are incorporated into the cost of the finished product, like when lumber is turned into a chair. This can result in the accumulation of multiple layers of sales tax, a phenomenon known as “pyramiding” or “cascading.” 4

But advertising purchases, targeted or otherwise, are different from many other business purchases because they directly involve a third party beyond the buyer and seller of the advertisement: the consumer of the platform, publication, or other content where the ad is placed. An advertiser pays a traditional platform like CBS or a newer platform like Google to run its ads; the ads allow CBS or Google to deliver content or services (like video content, search engine, social media, etc.) to consumers. There are really two distinct transactions happening: a business-to-business sale of an advertisement, and a business-to-consumer transfer of programming or services.

Consumers pay for what they’re getting with their eyeballs and, to an increasing degree, with their personal data – data that platforms in turn use to help sell more ads. Advertisers obtain not only direct customers who see their ads but also personal data that they can monetize further. But none of this is subject to sales tax unless states tax advertising revenue.

In other words, the consumption of “free” products escapes sales tax, even when it’s not really free. By contrast, the consumption of products financed via subscriptions are taxed. For example, most states tax at least some sales of subscriptions to online products, like streaming services.5 So Netflix collects sales tax on paid subscriptions, but social media platforms can provide their online content without any tax being collected, creating a bias in the tax code in favor of those platforms. Moreover, when Netflix provides a cheaper subscription that depends on consumers seeing ads, only the lower subscription cost is subject to sales tax even though those subscribers are “consuming” the exact same content as the subscribers paying the higher monthly fee. This disparity exists in the non-digital world, too; a magazine purchased in a store may be subject to sales tax (depending on the state) while a free one supported entirely by advertising typically is not – nor is the advertising that financed that magazine.

The uneven treatment of ad-funded and paid purchases also means that the pyramiding argument doesn’t apply as neatly to most advertising as it might apply to other business inputs. Almost all advertising expenditures are for consumer goods and services, not business-to-business purchases. The trade journal Emarketer estimates business-to-business digital ad spending represents between 5 percent and 6 percent of all digital ads. So a tax on advertising affects, at most, one level of production.6

In short, taxing advertising revenue that is being used to monetize “free” consumer services or to subsidize reduced-price versions is appropriate for the same reason directly taxing any other purchases are appropriate: such advertising revenue reflects at least some portion of the value that the consumer is giving for their use of the provider’s service making it an appropriate source of revenue for schools, roads, health care and other services.

The Rising Social Toll of Advertising and the Case for Excise Taxation

There is a further case for ending advertising’s exemption. Economists and social scientists have long recognized that advertising imposes costs that extend beyond the immediate transactions among platform, advertiser, and consumer. Examples include the visual clutter of outdoor advertising that degrades shared public spaces, the perpetuation of harmful stereotypes and unrealistic body images, the normalization of unhealthy products, and the psychological toll of near-constant commercial messaging. The literature on these costs stretches back at least as far as economist John Kenneth Galbraith’s 1958 critique of advertising’s role in manufacturing artificial demand in The Affluent Society.

The advent of programmatic advertising has created a new set of concerns about the high social costs that advertising and advertising-funded platforms, specifically in their increasingly targeted, algorithm-driven forms, are imposing on individuals, communities, and society.

The best-documented harm from new advertising-funded products is related to social media. A rapidly growing body of medical research is documenting the damage to brain structure and chemistry from these new advertising-funded products, especially among teens, because their brains are still developing. Social media addiction, though not yet a standard psychological diagnosis, is increasingly recognized as a threat to public health. Specific harms range from depression and eating disorders to increased teen suicide risk and heightened long-term risk of dementia.7

The widely documented and reported harms from social media are inseparable from those platforms’ reliance on ads for revenues. Social media is so pervasive largely because it is addictive by design; the longer a platform can keep a consumer’s attention, the more time it has to market a product. In other words, social media exists so that the platforms can sell more ads, gather more data, and seize more attention.

Social media and other online platforms are also responsible for much of the decline in local journalism and the spread of misinformation. Journalism is in serious trouble.8 For decades, news organizations have been making less money while readers increasingly expect to get news online. This matters because democracy depends on people having access to good information. While the internet has made more information available than ever, producing quality journalism is expensive. The main problem is that the business model has collapsed. Tech platforms like Google and Facebook now control how news gets distributed and seen online. Artificial intelligence-driven large language models like ChatGPT go a step further, synthesizing online information in ways that displace actual journalism.

The advertising money that formerly supported newsrooms now flows to these tech giants, who set the rules for how news reaches readers. The loss of funding combined with competition from online platforms hits local news outlets especially hard. On top of that, news organizations must constantly adapt to changing platform algorithms and policies, which makes running a newsroom even harder. The result: fewer resources for real reporting, weaker news institutions, and more room for misinformation to spread.

In short, the transformation of advertising over the last few years is imposing significant social costs. Fortunately, states have a ready-made mechanism to partially compensate for those costs: excise taxes. We tax tobacco, alcohol, cannabis, gambling, and fossil fuels not just to raise revenues but because their consumption imposes demonstrable costs on society. Taxing these products fairly and appropriately can compensate the public for medical costs, lost productivity, and other losses that result from the products’ use.

Excise taxes (as opposed to, say, outright prohibition) are particularly appropriate in cases where social costs are accompanied by at least some social benefits. Fossil fuels cause climate change, but they also heat our houses and facilitate transportation; alcohol consumption is bad for our health but for many people is simply enjoyable. So the fact that targeted advertising has the benefit of efficiently connecting consumers to products in which they might be interested is no reason to rule out excise taxes to compensate for the harm that accompanies any such benefit.

More directly, excise taxes can fund mechanisms for mitigating those harms, like mental health treatment. And, by making products more expensive, they can encourage consumers and businesses alike to spend their money on other, less socially destructive alternatives. Extensive research shows that higher tobacco and alcohol taxes save lives and reduce health care costs by discouraging smoking and drinking, especially among teens and young adults. There is at least the potential that taxing some or all advertising could nudge companies toward other types of expenditures, like improved product development.

The excise-tax argument also suggests that a tax rate even higher than the general sales tax is warranted. Just as states typically levy cigarette excise taxes in addition to general sales taxes, so too might states consider both extending their general sales tax and an additional excise tax to advertising. Going a step further, recognizing that governments bear many of the costs of addressing these social problems, some proposals earmark revenues for purposes related to those harms like mental health or public journalism.

How States Can Tax Advertising

The rapid emergence of targeted advertising, tied to the collection and use of personal data, and largely deployed via social media, has led states to explore various new taxation strategies. (Appendices A and B list examples of current and proposed taxes in this area.)

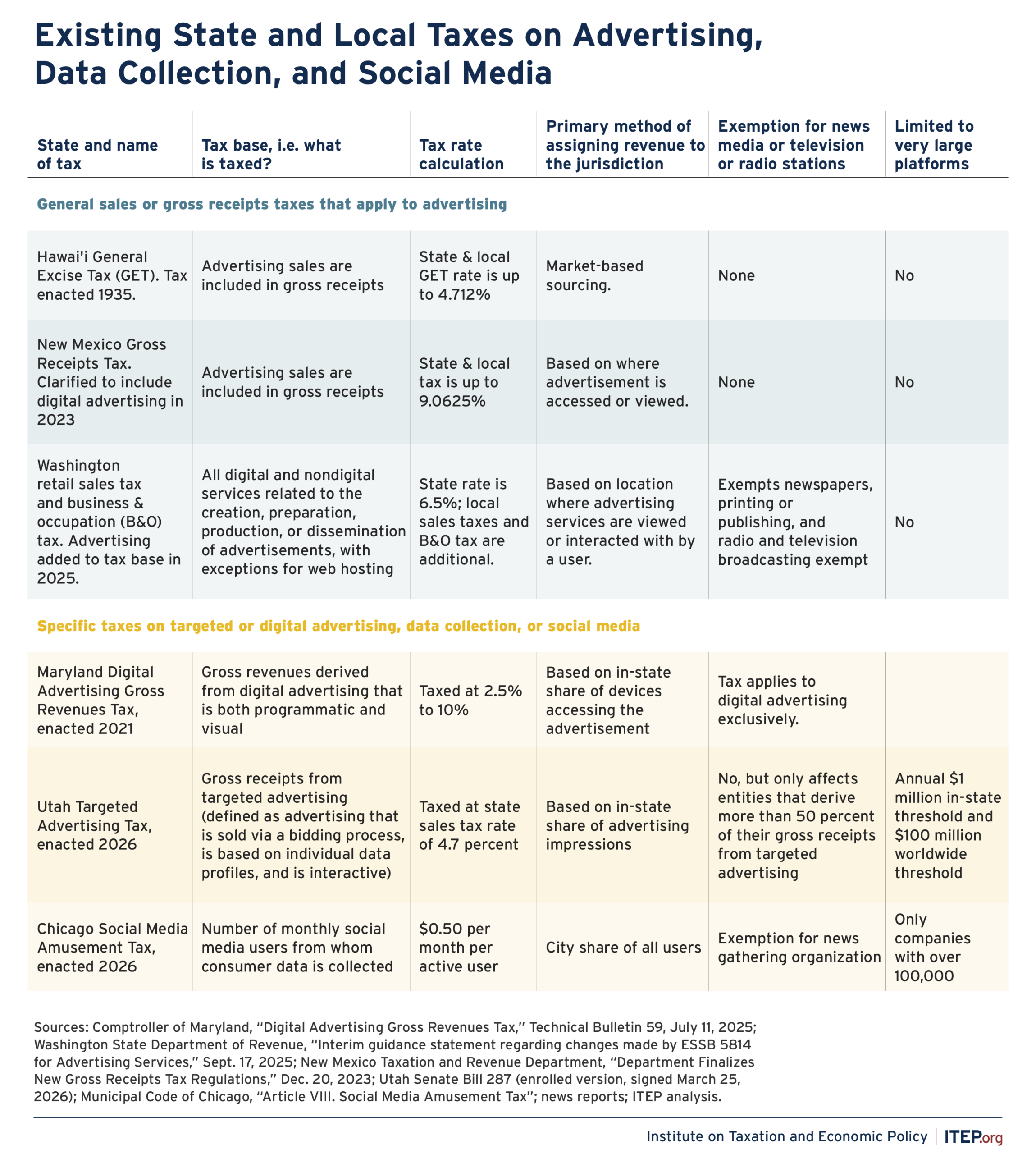

- Extend the state sales tax to include advertising generally. New Mexico historically applied its “gross receipts tax” (essentially a very broad-based sales tax) to all. A 2023 regulation clarifies that this includes digital advertising as well as traditional analog advertising.9 Hawai’i also has for many decades taxed advertising under its sales tax, known as a General Excise Tax. Hawai’i and New Mexico tax many other services, too, but a state would not have to tax all those other services to follow this approach to advertising.

- Extend the state sales tax to include advertising but exempt some traditional media. This approach focuses specifically on those emerging advertising mechanisms that over the last 20 years have come to dominate the advertising market. The state of Washington in 2025 extended its general sales tax and its retail business & occupation tax to all advertising, but exempted billboards, newspapers, and television and radio stations. Combined state and local sales tax rates in Washington range from 7.6 to 10.6 percent, depending on the locality, and the business & occupation tax adds another 0.471 percent. Washington expected to raise $422 million in 2026 and $701 million in 2027 in state revenue and $205 million in 2026 and $364 million in 2027 in local revenue from the 2025 base expansion.10

- Design a new tax to focus on targeted advertising on large platforms. Maryland in 2021 enacted a standalone tax on annual gross revenues from digital advertising services, defined as including “advertisement services in the form of banner advertising, search engine advertising, interstitial advertising, and other comparable advertising services.” Companies with over $100 million in global digital ad revenue and over $1 million in Maryland revenue pay tax at rates ranging from 2.5 percent to 10 percent, depending on total global revenue. As of October 2025, Maryland has raised $418 million since the tax was put in place in 2022.11

- Utah passed a targeted advertising tax this year, applying the state’s 4.7 percent sales tax to targeted advertising revenue of companies that raise at least $1 million in such revenue in the state. The Utah tax defines targeted advertising, in part, as interactive ads that are based on individual data and sold through a bidding process. (The allocation of ad space through auctions is known as “programmatic” advertising. For example, frequently when you load a webpage, an automated auction runs in milliseconds where advertisers bid against each other for the right to show you an ad, with the winning bidder’s creative instantly delivered to your screen.) This tax is expected to raise $15.2 million in 2028 and $21.3 million in 2029.12

- A new advertising tax to fund public journalism passed the California Senate in 2024 but died in the House. It would have established a 7.25 percent tax – same as the state sales tax rate – on the gross receipts from any advertising sales that are based on user data, and it would have applied only to companies with more than $2.5 billion in revenue from ads targeted to California residents.

Rather than tax advertising, some states are advancing other ways to tax new information-economy transactions.

- Tax the collection or use of the individual data that allows targeted advertising to occur. Such a tax may be analogized to severance taxes, which are taxes that many states levy on mining, forestry, or other extractive industries.13 Lawmakers in Massachusetts, New York, New Jersey, and other states have introduced “data excise tax” proposals that would require companies that collect personal data on a large number of users (for instance, more than 1 million New Yorkers) to pay a set amount per user – say, $25 per year.14

- Tax social media platforms as a form of entertainment. Chicago enacted a Social Media Amusement Tax on January 1, 2026. This taxes social media companies that collect consumer data on more than 100,000 Chicago users in a calendar year at $0.50 per month per active user. The new tax is expected to raise $31 million a year to fund expanded mental health services.

Table 1 provides an approximate estimate of how much each state could raise with a tax on all advertising at the state’s general sales tax rate, totaling $27 billion in new annual revenue across all states. It also provides an estimate for narrower tax bases – one that just excludes broadcast television, radio, and newspapers, and one that is limited to search engine and programmatic (i.e. auction-based) advertisements. Finally, it estimates the revenue that would be received just from Meta, Alphabet, and Amazon under a targeted advertising tax.

These estimates do not account for provisions of state sales tax laws that might apply to an advertising tax, depending on how the statute is draft. For example, they do not incorporate estimated impact on local sales taxes, which are typically based on the state sales tax base. Nor do they account for common sales tax provisions like the exemption of purchases by nonprofit organizations, which may reduce the estimates.

Other Countries’ Digital Services Taxes

There may be useful lessons to learn from other countries’ experiences. France, India, Italy, Spain, Turkey, and the United Kingdom, among other nations, have enacted Digital Services Taxes (DSTs), typically at rates of 2 or 3 percent, that apply broadly to revenues from advertising, social media, and other services above specified thresholds; in practice these are mostly taxes on advertising since that’s where the affected companies get most of their revenue.

The United Kingdom in 2020 implemented a 2 percent DST on certain revenues from search engines, social media platforms, and online marketplaces. The goal, according to the UK government, is to ensure that those companies “pay UK tax on their digital services to reflect that they derive value from user-related activities in the UK.”15 The tax applies to corporations with over £500 million global and £25 million UK revenues from digital services. Even at that low 2 percent rate and high threshold, the DST raised about £800 million (roughly $1 billion) in the 2024-25 fiscal year, equal to about £1 for every £400 of the UK’s GDP.16

State and Local Advertising Taxes and Federal Law

Federal law does not bar states from taxing advertising. Hawai’i and New Mexico have done so for decades without controversy.

More recently, some narrower taxes that focus on targeted and/or programmatic advertising or only very large platforms, or that exempt certain types of more-traditional advertising, have attracted litigation or the threat of litigation; the cases have not been resolved as of publication in May 2026.

- The Maryland law has been challenged in court on various grounds. A federal court found that a provision barring companies from itemizing the tax on its invoices violated the First Amendment of the U.S. Constitution, but a broader challenge to the tax itself has not been resolved. Other legal arguments against the Maryland law remain in litigation.17

- Litigation has been filed against the Washington law and the Chicago ordinance and has been threatened against the Utah law.

A common thread across these lawsuits is the allegation that the taxes violate the federal Internet Tax Freedom Act (ITFA). ITFA bars states from enacting “multiple or discriminatory taxes on electronic commerce;” electronic commerce is defined in the law as “any transaction conducted over the internet or through internet access.” “Discriminatory” is a key concept here; taxes that don’t distinguish between internet and non-internet sales do not violate ITFA.

Tech corporations and their lawyers have been quite vocal throughout legislative processes that they will sue to overturn these laws. As a result, executive and legislative counsels have taken significant care in drafting the laws, and they are being aggressively defended by the states. Defenders of these statutes point out that while the dawn of the internet era facilitated the rise of digital advertising, “internet” and “digital” are not identical. They argue the distinction is important for determining ITFA compliance.

For example, as law professor Darien Shanske and marketing professor Kenneth C. Wilbur point out, “The Maryland tax excludes gross receipts of certain ads delivered over the internet (for example, a classified ad on Craigslist) and includes gross receipts of certain ads not delivered over the internet (for example, DirecTV addressable TV ads conveyed to consumers by satellite broadcast signals).”18

Similarly, under the Washington law enacted in 2025, exemptions to the advertising tax are not based on whether a transaction occurs over the internet, but rather on separate legal definitions of newspapers, printing or publishing, and radio and television broadcasting. Ad sales by internet-based versions of newspapers are exempt; on the other hand, direct mail, although not delivered by the internet, is taxed.19

The 2026 Utah law taxes “targeted advertising,” which the law defines narrowly as advertising that is sold via a bidding process, is based on individual data profiles, and is interactive. Such ads can be seen on any medium.

The many unresolved issues may be resolved differently in different states and ultimately the U.S. Supreme Court (or Congress) may weigh in on the issues in different ways. This means the process of achieving certainty is likely to be lengthy, but state legislators will start receiving some useful information before too long. For example, having observed that the courts are inclined to reject the Maryland statute’s approach to invoices, other states have not included such a provision in their bills.

Who Will Ultimately Pay Advertising Taxes?

Like other sales and excise taxes, advertising taxes are remitted to the state by the company selling the advertisements; for example, in the case of targeted ads, that often means a big platform like Google (Alphabet). But, as with other sales taxes, the legal incidence of the tax is often associated with the location of the customer, and advertisements often cross state lines.

This raises both a practical question and a fairness concern. In practical terms, how will a state revenue department determine how much tax is owed from a national or global advertising platform? And should policymakers worry that platforms will simply shift the cost of these taxes onto local consumers?

Administration

The practical issue is that a retailer based in State A might buy an ad from a platform hosted in State B targeted to a consumer based in State C. It can become even more complicated when ad space is resold multiple times. Figuring out which of those states gets the tax revenue requires establishing some guidelines. Fortunately, there is already a large body of law and regulation devoted to answering similar questions.

For most states, sales taxes are collected based on a principal known as “destination-based sourcing.” This means that the tax is collected based not on where the seller is located but rather on where the consumer is located or, more precisely, where the product is delivered for use. In the case of advertising, that will typically mean where the ad is viewed.

So for example, New Mexico collects tax on ad sales if the advertisement is “accessed or viewed” in New Mexico.20 Washington’s revenue department has issued interim guidance explaining that advertisements are taxed “where the result of the advertising services is first used” and providing a series of tests for platforms to determine that more specifically, depending on what information it has on the users.21 Utah’s new law taxes platforms’ targeted ad revenue based on the share of “impressions” delivered to “an audience or individual located in Utah.” In these states, the fact that Google is based in California is largely irrelevant to whether other states can tax Google ads; what matters more is where Google’s users are sitting when they view the ad.

It should not be terribly difficult for a very large advertising platform to come up with a reasonable calculation of which advertisements are intended to be viewed in a state. Most advertising today involves knowing a great deal about the person who is viewing the advertisement and having a great deal of capacity to analyze that information. That’s the whole point of targeted ads. In many cases, it will be straightforward for the purchaser and/or seller of an ad to identify where the end user is and, often, their ZIP code. In cases when they don’t have that information, other sources of data can help them produce reasonable approximations.

In fact, even in the absence of an advertising tax, states and advertisers have been developing tools for identifying the geographic location of the customers for products delivered electronically, as well as rules of thumb to manage situations where those customers’ locations are not known, such as sourcing based on overall population ratios. Most states already tax the sale of at least some digital goods and/or services.22 So states are well down the road toward developing rules that establish where a customer is physically located when they’re receiving a virtual good. The Multistate Tax Commission has long developed model regulations on how to allocate transactions based on where the viewer of an electronic transmission is located, and is now developing a model set of regulations for taxing the sales of digital products that includes sourcing rules.23 These regulations could inform the development of sourcing rules for advertising taxes.

Fairness

There is also a concern that advertising platforms would charge more to businesses who advertise on their platforms, and then those advertisers would compensate by raising prices on consumers.

If both of those things were to happen (advertising platforms raise their prices and then advertisers pass the costs on to consumers), then consumers would bear the final incidence of the tax. Since lower-income households tend to spend a greater share of income on consumption goods than higher-income households do, this new tax could well be regressive, although not necessarily more so than a state’s existing sales and excise taxes.

In particular, targeted advertising is still relatively new, and so it is even less clear what portion of a targeted advertising tax would be passed along to consumers – or to which customers. Facing the prospect of competition from smaller platforms and businesses, the large platforms may opt to absorb some of the cost to maintain market share. And if they don’t, advertisers might opt to shift their ad buys to other, smaller platforms – perhaps non-targeted forms of advertising – that don’t face the tax. Alternatively, advertisers might choose to scale back their advertising budgets and invest instead in product quality or consumer discounts.

There is also the question of what kinds of goods and services are the subject of various types of advertising. Sellers of high-end consumer goods have historically favored prestige print advertising — particularly glossy magazines — instead of the targeted advertising that dominates most of the ad market. But that gap appears to be narrowing, as market analysts report luxury brands increasingly shift budgets toward digital channels to reach affluent consumers where they spend their time.24

What may matter most is where this new tax will fit in states’ overall revenue structure. Most state tax codes already take a higher percentage of income from poor and middle-income households than from wealthier households. Across all states, for example, low-income taxpayers face an effective state and local tax rate nearly 60 percent higher than the wealthiest households as a share of income, and middle-income taxpayers pay tax 45 percent higher than the wealthiest.25 Sales and excise taxes generally drive this regressivity. If the new tax simply were to increase states’ reliance on sales and excise taxes, the overall structure might become more regressive; but this is not the only approach possible.

Policymakers could, for example, make their tax systems more progressive by using the new revenue from a targeted advertising tax to fund a state Child Tax Credit to help households meet basic needs, or to create a “data dividend” fund to distribute back to state residents similar to how Alaska’s Permanent Fund provides oil revenue dividends to state residents.26

Policymakers could also explore pairing a tax on advertising revenues with other mechanisms to ensure that the shareholders and top executives of big technology corporations profiting the most from the new information economy do pay tax.

- For example, to more directly capture the tremendous wealth that is being generated by companies, especially those earning monopolistic profits, states can enact additional taxes on the profits that any company earns in excess of some basic return on investment.27

- Alternatively, recognizing that corporations are accumulating wealth and power long before they report any taxable profits at all, states can do more to tax the market value of corporations that are highly valuated even though they report little taxable profits.28

- States can decline to conform to new and expanded federal tax breaks that are allowing large tech companies and many others to avoid tens of billions of dollars in taxes on their enormous profits.29

- They can also address the concentration of wealth and power in the hands of individual tech barons and other investors by closing well-known loopholes related to investment income and wealth, including eliminating stepped-up basis, creating higher and more rigorous taxes on capital gains, inheritances or estates, decoupling from federal investor loopholes like the carried interest deductions, adding million-dollar income brackets, and the like.

At a minimum, states should avoid using revenue from targeted advertising taxes – or other sales or excise tax increases, for that matter – to fund reductions in taxes on corporate income or profits. Given the uncertain distributional implications of advertising taxes, such a tax swap might make consumers worse off while simultaneously making profitable corporations and their owners and top executives even wealthier than they already are.

Conclusion

The long-standing exemption in most states of advertising from state sales taxes was always a questionable policy choice, and the rise of data-driven, algorithmically targeted advertising has made it indefensible, partly because of its significant social costs. States that extend their sales taxes to advertising and/or enact an excise tax — whether broadly or with a focus on targeted or programmatic advertising —stand to raise billions in revenue while correcting a structural bias in their tax codes that implicitly subsidizes some of the most profitable corporations in human history. The legal landscape remains unsettled, but the early experience of states like Maryland, Hawaiʻi, New Mexico, Washington, and Utah provides a growing evidence base for legislators willing to move forward. Policymakers who act thoughtfully — attending to questions of tax design, distributional fairness, and legal compliance — can help bring state tax systems into alignment with the realities of a twenty-first century information economy, while funding the public services and social supports that communities will require to thrive in this new economy.

The author would like to thank ITEP Policy Intern Cassidy Sheppard for their contributions to this report.

APPENDIX A

APPENDIX B

APPENDIX C: Estimating Methodology

The revenue estimates in this paper were derived as follows.

First, national estimates of the advertising market were obtained from industry sources.

- The research firm Statista estimates total U.S. advertising market revenue will be $515 billion in 2027.

- Statista estimates broadcast television, radio, and newspaper advertising will total $74 billion in 2027, so all advertising minus traditional broadcast and newspaper would total $441 billion.

- The Internet Advertising Bureau’s “IAB/PwC Internet Ad Revenue Report” provides separate 2005 estimates for programmatic advertising and for search-engine advertising. Combining these numbers and projecting them forward to 2027 based on the average growth rates of the last four years, yields an estimate of $309 billion. This represents an upper-bound estimate of advertising revenue derived from individual user data and real-time auctions.

- Estimates of the U.S. advertising revenues of Meta, Amazon, and Alphabet – the three largest sellers of advertisements in the United States – were derived from their 10k filings with the Securities and Exchange Commission, multiplied by 90 percent to reflect a conservative industry consensus figure of the percentage of digital advertising that is targeted, and inflated forward from 2025 to 2027 to reflect historical growth trends. This yields a national total of $285 billion.

These national estimates then were prorated to each state (see Table 2). The assumption was made that advertising dollars will follow consumption dollars, so we used each state’s share of Personal Consumption Expenditures as reported by the U.S. Commerce Department to allocate the national advertising estimates to each state.

Finally, we multiplied each state’s estimated share of 2027 advertising expenditures by its state sales tax rate, excluding local taxes. We omitted states that already tax some or all advertising as described in the body of this paper – Hawai’i, Maryland, New Mexico, Utah, and Washington. For states without current sales taxes, we used a 3 percent rate. We adjusted the results downward by the tax rate to reflect the possibility that advertisers would reduce their advertising spending to accommodate their tax obligations.

Endnotes

- 1. Institute on Taxation and Economic Policy, “Historical State Tax Rate Data,” File Version 2026.1, January 2026.

- 2. Amanda Parsons, “Taxing Social Data,” University of Colorado Legal Studies Research Paper No. 25-20, July 2025.

- 3. ITEP calculations from firms’ 10k filings, U.S. Commerce Department data, and Statista Market Insights forecast.

- 4. ITEP, “What’s Exempt from State and Local Sales Taxes?” ITEP Guide to State & Local Taxes; Carl Davis, “Pyramids, Cascades, and the Taxation of Business Inputs,” presentation to the New Mexico Revenue Stabilization and Tax Policy Committee, August 2024.

- 5. The majority of states and localities that tax sales of physical goods also tax the same product if it’s sold in digital form. The tax advisory firm Avalara lists only 14 states — California, Florida, Illinois, Kansas, Massachusetts, Michigan, Missouri, Nevada, New York, North Dakota, Oklahoma, South Carolina, Virginia, and West Virginia — as exempting many digital goods from their sales taxes even when their tangible equivalents are taxed. On streaming services specifically, see Richard C. Auxier, “Chicago’s Streaming Tax Is A Bad Tax But It’s Not A ‘Netflix Tax’,” Urban-Brookings Tax Policy Center, June 2019.

- 6. Jennifer King, “By 2026, Worldwide B2B Digital Ad Spend Is Set To Nearly Triple Its Pre-Pandemic Level,” EMarketer, November 2024.

- 7. See for example Yunyu Xiao et al, “Addictive Screen Use Trajectories and Suicidal Behaviors, Suicidal Ideation, and Mental Health in US Youths,” Journal of the American Medical Association, June 2025; Martin Korte, “The impact of the digital revolution on human brain and behavior: where do we stand?” Dialogues in Clinical Neuroscience, 22(2), April 2022; D. De et al, “Social Media Algorithms and Teen Addiction: Neurophysiological Impact and Ethical Considerations,” Cureus Journal of Medical Science, January 2025; and Laurie A. Manwell et al, “Digital dementia in the internet generation: excessive screen time during brain development will increase the risk of Alzheimer’s disease and related dementias in adulthood,” Journal of Integrated Neuroscience, January 2022.

- 8. Michael Karanicolas, “A Shifting Market for Information; a Disappearing Market for Journalism,” in Shearing the Sheep Without Skinning It: Policy Options for Extracting Revenue from Online Platforms, UCLA Institute for Technology, Law & Policy, pp. 1-2.

- 9. New Mexico Taxation and Revenue Department, “Department Finalizes New Gross Receipts Tax Regulations,” December 2023.

- 10. Fiscal Note for ESSB 5814 as enacted, Washington Department of Revenue, May 2025.

- 11. News release, Comptroller of Maryland, Dec. 12, 2025, p. 2.

- 12. Fiscal Note for SB 287, Utah Legislative Fiscal Analyst Office, March 2026.

- 13. As University of Tennessee law professor Andrew Appleby points out, “Data has emerged as the modern economy’s most precious resource – a ‘new gold’ that is fundamentally transforming how businesses create and capture value.” Appleby, “Data Extraction Taxes,” University of Tennessee, Knoxville – Winston College of Law Research Paper, October 2025.

- 14. Robert Plattner, Michael Mazerov, and Darien Shanske, “A Model Tax on the Collection of Consumer Data by Commercial Data Collectors Based on New York’s Senate Bill 4489, 2025-2026 Legislative Session,” SSRN, April 2026.

- 15. HM Treasury, Digital Services Tax Review, November 2025.

- 16. The Trump Administration has opposed these taxes and successfully pressured Canada to abandon a similar tax, but it is not entirely clear whether the opposition is on policy grounds or on the grounds of not wanting foreign countries to tax large U.S.-based companies, so it is not clear whether the Administration would oppose similar taxes if levied within the United States.

- 17. Some of the legal arguments against the Maryland law do not apply to the laws and proposals in other states. For example, opponents of the Maryland law argue that it violates of the U.S. Constitution’s Commerce Clause because it uses a company’s global gross revenue to determine the tax rate, which they say penalizes out-of-state activity. The Washington law and proposals in other states levy the same rate on all in-state advertising, so that argument doesn’t apply.

- 18. Darien Shanske and Kenneth C. Wilbur, “Better Arguments Still Favor Maryland’s Digital Ad Tax,“ Tax Notes State, Oct. 27, 2025. Shanske is a member of ITEP’s board of directors.

- 19. See Washington State Department of Revenue (DOR), “Advertising Services” and “Interim guidance statement regarding changes made by ESSB 5814 for Advertising Services,” September 2025.

- 20. New Mexico Administrative Code 3.2.213.13, effective Dec. 19, 2023.

- 21. Washington State DOR, “Interim Guidance,” September 2025.

- 22. The majority of states and localities that tax sales of physical goods also tax the same product if it’s sold in digital form. The tax advisory firm Avalara lists only 14 states — California, Florida, Illinois, Kansas, Massachusetts, Michigan, Missouri, Nevada, New York, North Dakota, Oklahoma, South Carolina, Virginia, and West Virginia — as exempting many digital goods from their sales taxes even when their tangible equivalents are taxed.

- 23. Multistate Tax Commission, Model General Allocation & Apportionment Regulations, July 2018, pp. 65-74, and “Sales Tax on Digital Products Project Description,” accessed April 2026.

- 24. See for example Amra & Elma, “Luxury Marketing Statistics,’ 2023.

- 25. ITEP, Who Pays? A Distributional Analysis of the Tax Systems in All 50 States, Seventh Edition. 2024.

- 26. For more detail on state CTCs, see Neva Butkus, “State Child Tax Credits Boosted Financial Security for Families and Children in 2025,” Institute on Taxation and Economic Policy, updated February 2026.

- 27. Reuven S. Avi-Yonah and Tamir Shanan, “Rethinking Taxing Excess Profits,” University of Michigan Public Law Research Paper, April 2024.

- 28. Emmanuel Saez and Gabriel Zucman, “A wealth tax on corporations’ stock,” Economic Policy, April 2022.

- 29. Matthew Gardner, “Four Big Tech Companies Avoid $51 Billion in Taxes in Wake of One Big Beautiful Bill Act,” Institute on Taxation and Economic Policy, February 2026.