President Biden discussed multiple tax proposals during the State of the Union address to Congress. Several of these proposals appeared in the budget plan he submitted to Congress last year, but at least two appear to be new proposals.

Raise Corporate Tax Rate from 21 Percent to 28 Percent

10-Year Revenue Impact in President’s Previous Budget: $1.3 trillion

The President’s budget would partly reverse the cut in the corporate income tax rate that was signed into law by former President Trump as part of the Tax Cuts and Jobs Act (TCJA). President Biden’s plan would raise the corporate income tax rate from 21 percent to 28 percent, still lower than the 35 percent rate that applied to most corporate profits before TCJA came into effect. As explained below, the arguments in favor of a lower corporate tax rate were always weak and based on misunderstandings of how corporations respond to tax changes.

Corporate Tax Cuts Did Not Make American Companies More Competitive

- Drafters and supporters of TCJA claimed that the rate cut would make the United States more globally competitive. But it is not the case that the pre-TCJA corporate tax code made the United States less competitive than other countries or that the rate cut made the U.S. more so.

- The United States accounts for just over 4 percent of the world’s population and a quarter of global GDP, but American corporations account for 40 percent of the market value and a third of the sales of the Forbes Global 2000, which is an annual list that measures the largest businesses in the world based on sales, profits, assets, and market value.

- These figures were essentially the same in 2017, before the TCJA was enacted and in the years that followed. American corporations had a huge advantage and that has not changed.

Corporate Tax Cuts Benefit Shareholders, Who Are Mostly Wealthy Americans and Foreign Investors

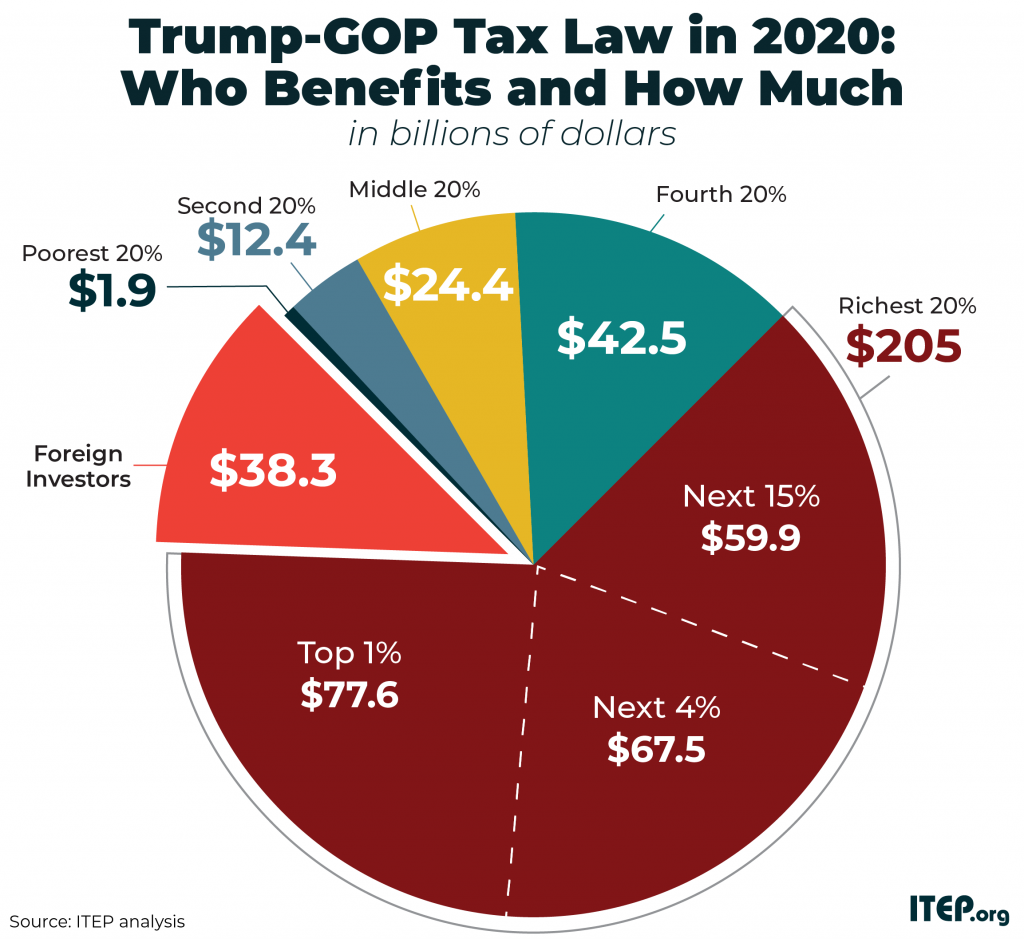

- Congress’s official revenue estimator, the Joint Committee on Taxation, has concluded that most of the benefits from corporate tax cuts flow to the owners of corporate stocks and other business assets, who are mostly wealthy. Recent research has concluded that a great deal of the benefits also flow to foreign investors, who own an estimated 40 percent of the shares of American corporations.

- Altogether, the richest 1 percent of Americans and foreign investors received most of the benefits of the corporate tax cuts enacted under former President Trump.

Corporations Used their Tax Cuts to Enrich Shareholders with Stock Buybacks, Not to Invest and Create Jobs

- In the first four years after these corporate tax cuts went into effect, the largest American corporations collectively spent more on enriching their shareholders through stock buybacks ($2.72 trillion) than on investments in plants, equipment, or software that might have created new jobs and grown the economy ($2.65 trillion).

Corporations Would Not Lobby for Corporate Tax Cuts If They Thought Their Shareholders Were Not the Beneficiaries

- Corporations are created to build wealth for their shareholders, and the CEO and management of a corporation ultimately serve the shareholders. And corporate executives themselves usually own a lot of stock in the company they work for.

- Given how much corporations lobby for corporate tax breaks, it is quite clear that the corporate executives themselves believe that the benefits go to the stock owners.

Revise Global Minimum Tax Rules – Including 21 Percent Minimum Tax on Offshore Profits

10-Year Revenue Impact in President’s Previous Budget: $493 billion

American corporations often use accounting gimmicks to disguise profits earned in the United States (or in a country with a comparable tax system) as profits earned in offshore tax havens, which are countries with no significant corporate tax. This proposal would greatly reduce the tax breaks that corporations can acquire through these schemes.

Enacting these reforms would bring the United States into compliance with the international agreement that the Biden administration negotiated with the Organization for Cooperation and Development (OECD) and most of the world’s governments to create a global minimum tax. Here are some of the most important parts of this proposal:

Reducing the Gap Between Effective Tax Rates for Offshore Profits and Domestic Profits

- When corporations are allowed to pay less on offshore profits than on domestic profits, this encourages accounting schemes that make more profits appear to be earned in low-tax countries.

- The current rules enacted as part of the Trump tax law create this result, allowing American corporations to pay an effective tax rate on offshore profits (10.5 percent) that is half the effective rate they pay on domestic profits (21 percent). The President proposes to reduce this gap by allowing an effective rate for offshore profits that is three-fourths of the domestic rate (21 percent for offshore profits compared to the 28 percent rate he proposes for domestic profits).

- This would be more than sufficient to implement the global minimum tax that the Biden administration negotiated with the international community, which requires participating countries to ensure that their corporations pay an effective tax rate of at least 15 percent on their offshore profits.

Applying the Minimum Tax Per Country to Prevent Corporations from Using High Taxes Paid in One Country to Offset Very Low Taxes Paid in Another Country

- To the extent that the current rules require corporations to pay a minimum tax on their offshore profits, the minimum tax is calculated on worldwide basis rather than a per-country basis, which makes it easier for multinational companies to avoid it.

- For example, a company could have profits in Country A where it pays an effective tax rate of just 5 percent but still be able to avoid the worldwide minimum tax if it pays an effective rate of 25 percent on profits in Country B. Its overall effective tax rate calculated on its offshore profits could be more than the minimum rate required.

- The President’s proposal would calculate the minimum tax separately for each country where the corporation reports that it earns profits.

Eliminating the Exemption for Certain Offshore Profits

- Under current law, some offshore profits of American corporations are not taxed at all because they fall within an exclusion (equal to a 10 percent return on tangible offshore investments like plants and equipment).

- The drafters believed that a 10 percent or less return on investments and personnel is likely to be real profits generated from real business and not the result of accounting gimmicks that merely shift numbers around to make profits to appear to be earned in low-tax countries.

- Of course, the 10 percent threshold is arbitrary. Even worse, it could encourage companies to move investment and jobs offshore to claim the exemption for more of the profits they already report to earn offshore. The President proposes to eliminate this exemption.

Increase the IRA’s Minimum Corporate Tax Rate from 15 Percent to 21 Percent

New Proposal – Not Included in President’s Previous Budget Plans

The corporate minimum tax enacted as part of the Inflation Reduction Act (IRA) and which went into effect in 2023 requires the largest corporations to pay federal tax of at least 15 percent of the profits they report to their shareholders. President Biden proposes to increase this corporate minimum tax rate to 21 percent.

- The IRA’s minimum tax was enacted as a backstop to the regular federal corporate income tax which has a statutory rate of 21 percent but allows most corporations to effectively pay much less than that because of its many special breaks and loopholes.

- ITEP’s latest study finds that in the first five years since the corporate income tax rate was set at 21 percent, the Fortune 500 companies and S&P 500 companies that were consistently profitable during that period effectively paid a rate of just 14.1 percent.

- The ITEP study also identified 55 corporations that paid effective rates of less than 5 percent (including several that paid nothing) over the five-year period despite reporting profits to investors and the public each year.

- The IRA’s minimum tax, which went into effect in 2023, will mitigate at least some of this tax avoidance for the very largest companies.

This minimum tax applies to those corporations that report annual profits averaging more than $1 billion over the previous three years. One study found that 78 companies would have been affected by the provision if it had been in effect in 2021.

- President Biden proposes to increase the rate of this minimum tax from 15 percent to 21 percent, which is consistent with his other proposals.

The President proposes to also raise the main statutory corporate tax rate from 21 percent to 28 percent and to enact a 21 percent minimum tax on offshore profits of corporations to crack down on their use of offshore tax havens, as described above.

Increase Stock Buyback Excise Tax from 1 Percent to 4 Percent

10-Year Revenue Impact in President’s Previous Budget: $238 billion

President Biden and Congress enacted a 1 percent excise tax on stock buybacks last year as part of the Inflation Reduction Act. Buybacks are projected to rise in 2024, and the tax had little or no effect on corporations’ decisions to repurchase their own stocks in 2023, which means the tax could potentially collect more revenue at a higher rate.

It also appears that the tax is not high enough to eliminate the tax advantage for stock buybacks over other methods that corporations use to send profits to shareholders. For these reasons, the President proposes to increase the stock buyback excise tax that is effect now under the IRA from 1 percent to 4 percent.

While corporate dividends paid to shareholders are subject to the personal income tax in the year they are distributed, stock buybacks effectively give the same financial benefit to shareholders by boosting stock values but can remain untaxed for years or in some cases forever. The stock buyback tax can reduce that disparity, but its current rate of 1 percent is not high enough to eliminate it.

See ITEP’s more detailed explanation of the stock buyback proposal.

Billionaire Minimum Income Tax

10-Year Revenue Impact in President’s Previous Budget: $437 billion

Most people think of a capital gain as the profit one receives when selling an asset for more than it cost to acquire it. But when an asset becomes more valuable, that asset appreciation can also be thought of as income for its owner, even if they do not sell the asset. Economists consider these “unrealized capital gains” to be income, but the tax code usually does not.

The result is a major tax break for capital gains, the ability of wealthy people to defer paying income taxes on gains until they sell assets. The President’s proposed Billionaire Minimum Income Tax would limit this tax break and would be phased in for taxpayers with a net worth between $100 million and $200 million.

Those wealthy enough to be subject to the proposal would generally be required to pay at least 25 percent of their total income, including unrealized capital gains, each year. (The President included the same proposal in his budget plan last year, except that last year his proposed minimum tax rate was just 20 percent instead of 25 percent.)

When this equals more than they owe under the regular tax rules, affected taxpayers would have five years to pay the difference (nine years for the tax assessed in the first year the proposal is in effect). This gradual payment would smooth out long-term calculations of the tax for someone whose assets fluctuate dramatically in value. If unrealized gains in one year are followed by unrealized losses in another year, only a portion of the minimum tax is paid for the first year and then potentially refunded in the following year. Payments of the minimum tax would also serve as prepayments of the tax that would otherwise be due later when a taxpayer sells an asset or passes it to an heir.

Some other proposals, like Sen. Ron Wyden’s “Billionaires Income Tax” create something closer to a “mark-to-market” system of taxation, which would treat unrealized gains as income each year. The President’s proposal is different because it is structured as a minimum tax, ensuring that very wealthy people pay at least 25 percent of their total income, including the unrealized gains that escape taxation under current law.

See ITEP’s more detailed explanation of these proposals.

Limit Capital Gains Breaks for Millionaires

10-Year Revenue Impact in President’s Previous Budget: $214 Billion

The President also proposes to sharply limit two other tax breaks for capital gains.

First, current rules tax capital gains (when they are realized) at lower rates than other types of income. In effect this means that people who live off of their investments can pay lower tax rates than people who work for their income.

Currently, income from capital gains and dividends is taxed at a top personal income tax rate of just 20 percent, compared to a top rate of 37 percent for ordinary income (39.6 percent under the President’s budget). The White House proposes to tax all income over $1 million at the top ordinary personal income tax rate regardless of whether it is capital gains, dividends, or some other type of income.

Second, current rules entirely exempt capital gains on assets that a taxpayer does not sell before the end of their life. In other words, unrealized capital gains on assets passed to heirs are never taxed.

This break is sometimes called the “stepped up basis” rule. When assets are passed on, the heirs receive those assets at a basis (original value) set to the date at which the assets are inherited. For example, if some asset is originally purchased at a value of $50 million and is then passed to an heir at a current value of $100 million, the heir can immediately sell the asset for $100 million without reporting any capital gain. This rule allows an enormous amount of capital gains to go untaxed.

The President’s budget would partially address this problem by treating unrealized gains as taxable income for the final year of a taxpayer’s life. Still, generous exemptions would apply. This proposal would exempt $5 million of unrealized gains per individual and effectively $10 million per married couple. The President also proposes allowing any family business (including farms) to delay the tax if the business continues to be family-owned and -operated.

$1 Million Limit on Corporate Deductions for Compensation to Employees

New Proposal – Not Included in President’s Previous Budget Plans – 10-Year Revenue Impact Reported to Be $270 Billion

More details are needed to understand exactly what the President is proposing, but it would appear to strengthen the tax code’s section 162(m), which limits deductions that corporations take for compensation to $1 million in certain situations.

Until recently, section 162(m) had an exception for performance-based pay (like stock options) and only applied to the top five executives in any given company. TCJA removed the exception for performance-based pay (but grandfathered in existing stock options). And ARPA generally expanded the number of employees covered from 5 to 10. But any employees beyond that are not covered. Also, section 162(m) applies only to publicly traded companies.

According to press reports, the President is proposing to expand section 162(m) to apply to all employees of a corporation, regardless of whether it is a publicly traded or privately owned corporation.

Limit Tax Breaks for Corporate and Private Jets

New Proposal – Not Included in President’s Previous Budget Plan

More details are needed to understand exactly what the President is proposing but it appears that he would address a couple of different problems with how the use of jets by the wealthy is undertaxed.

One problem is that private jet travelers pay less in taxes to support infrastructure that makes aviation possible than regular commercial air travelers.

- According to a study by the Institute on Policy Studies, “private jets make up approximately one out of every six flights handled by the Federal Aviation Administration (FAA) but contribute just 2 percent of the taxes that make up the trust fund that primarily funds the FAA.”

- The IPS study finds that “commercial passengers pay a 7.5 percent tax on the prices of their tickets plus a passenger facility charge of no more than $4.50… Meanwhile, private jet fliers only pay fuel surcharge taxes — roughly $0.22 per gallon of jet fuel.”

- Taxpayers are also largely funding, through the FAA, small airports used mainly by the wealthy few who fly in private jets.

Another problem is that very wealthy people often illegally claim business tax deductions for jets that are really being used for personal use.

- ProPublica has reported that several extremely wealthy individuals have taken bonus depreciation (writing off the full cost of equipment the year it is purchased) under the Trump tax law for jets that are almost entirely for personal use, despite the fact that bonus depreciation is limited by statute to the cost of business equipment.

- The IRS has recently announced that it plans to crack down on this type of misuse of tax deductions for corporate jets that are really jets for personal use.