Recent Work by ITEP

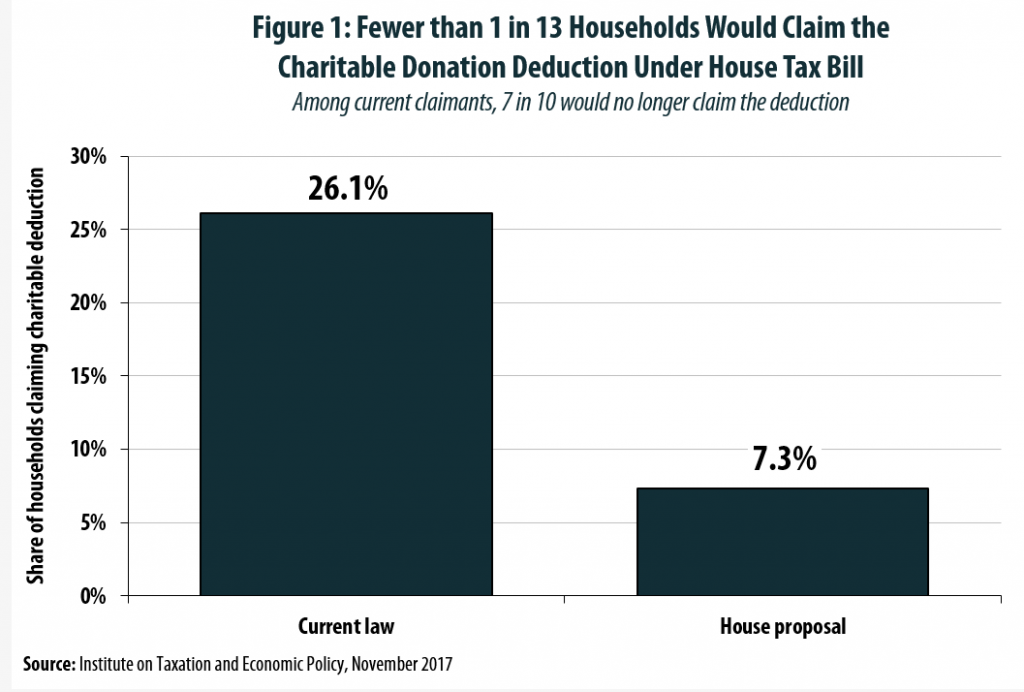

House Tax Bill Would Reserve Charitable Giving Subsidies for a Small Subset of Wealthier Households

November 6, 2017 • By Carl Davis, Steve Wamhoff

In the tax policy framework released in September, President Trump and Congressional leadership insisted that their proposal would retain the tax incentive for donating to charity because doing so helps “accomplish important goals that strengthen civil society, as opposed to dependence on government.” Now that the House has released a more detailed proposal, it is finally possible to evaluate exactly how their plans would impact the incentive to donate to charity.

American Corporations Tell IRS that 61 Percent of Their Offshore Profits Are in 10 Tax Havens

November 5, 2017 • By Richard Phillips

Recent revelations that a Bermuda law firm helped facilitate offshore tax avoidance has heightened awareness of the vast amount of income and wealth flowing into tax and secrecy havens worldwide. The countries through which this firm helped funnel global elites’ assets also act as tax havens for multinational corporations. Recently released data from the Internal Revenue Service show that U.S. corporations claim that 61 percent of their foreign subsidiaries’ pretax worldwide income is being earned in 10 tiny tax haven countries.

Nike earned more than $10 billion in U.S. profits from 2008 to 2015 but only paid 18.6 percent in U.S. federal taxes during this time. This is just over half of the official U.S. corporate tax rate of 35 percent.

Since Facebook became a public company, its annual revenues have increased by 250 percent from around $8 billion in 2013 to nearly $28 billion last year. In the same time period, the company’s before-tax profits shot up four-and-a-half fold to $12.5 billion. But in this time it has also managed to avoid billions of dollars in U.S. taxes.

Apple is the most valuable public company of all time with a market value of more than $800 billion. Last year, it cleared $45.7 billion[iii] in profits after taxes, making it the most profitable company in the Fortune 500 for the third straight year.

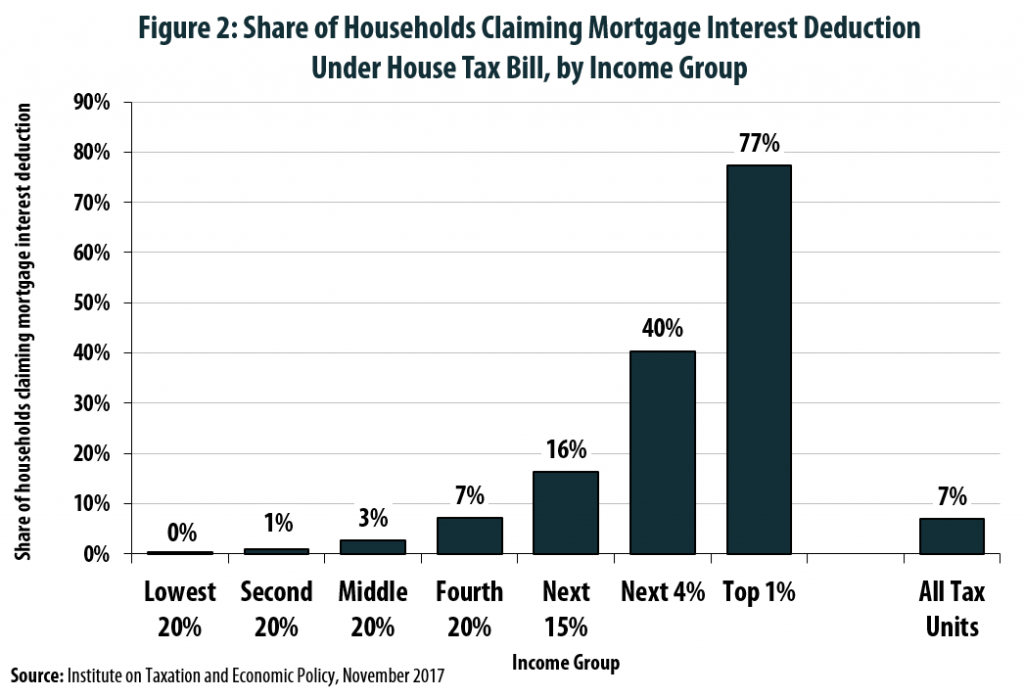

Mortgage Interest Deduction Wiped Out for 7 in 10 Current Claimants Under House Tax Plan

November 5, 2017 • By Carl Davis, Steve Wamhoff

Throughout the ongoing federal tax debate, President Trump and Congressional leadership have insisted that while many tax deductions and credits would be wiped out, the mortgage interest deduction would be spared from the chopping block. But while the proposal recently unveiled by House leaders retains the mortgage interest deduction on paper, the actual substance of this policy would be nearly unrecognizable to today’s homeowners.

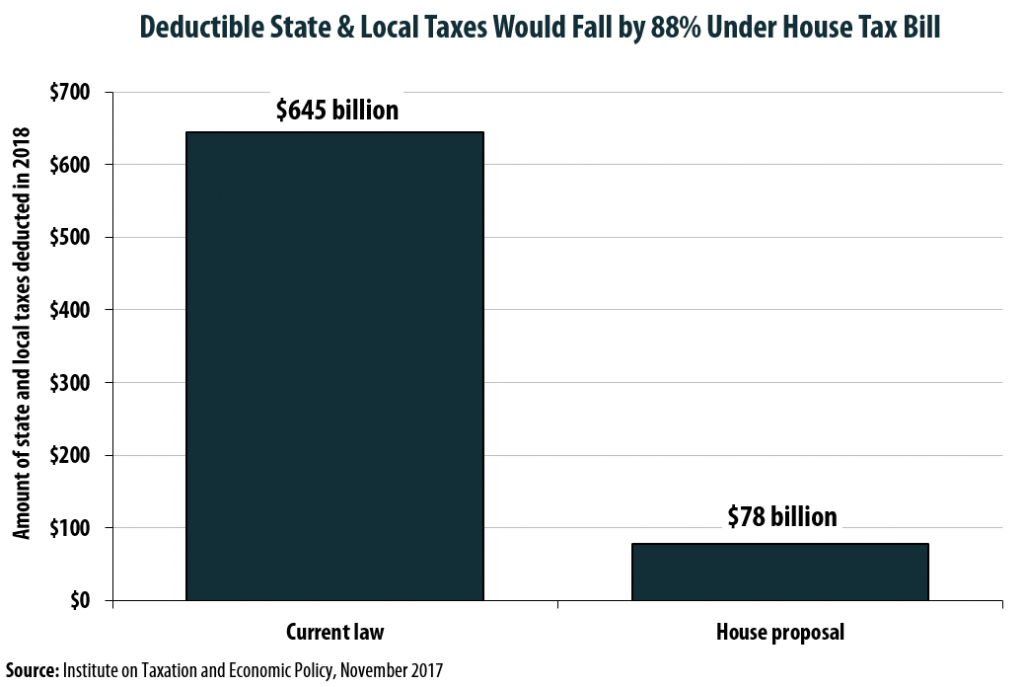

House Plan Slashes SALT Deductions by 88%, Even with $10,000 Property Tax Deduction

November 3, 2017 • By Carl Davis, Steve Wamhoff

One of the most contentious issues in the current federal tax debate is over what to do with the deduction for state and local taxes paid (the SALT deduction). Since the deduction’s benefits vary by state, the House proposal to drastically scale it back has led to an outcry among lawmakers from states such as New York, New Jersey, and California whose constituents would be impacted most dramatically by the change. In an attempt to address those concerns, House leadership agreed to partially retain the deduction for real estate property taxes paid (up to $10,000 per year) while still repealing…

A Chart Book on the U.S. Tax System

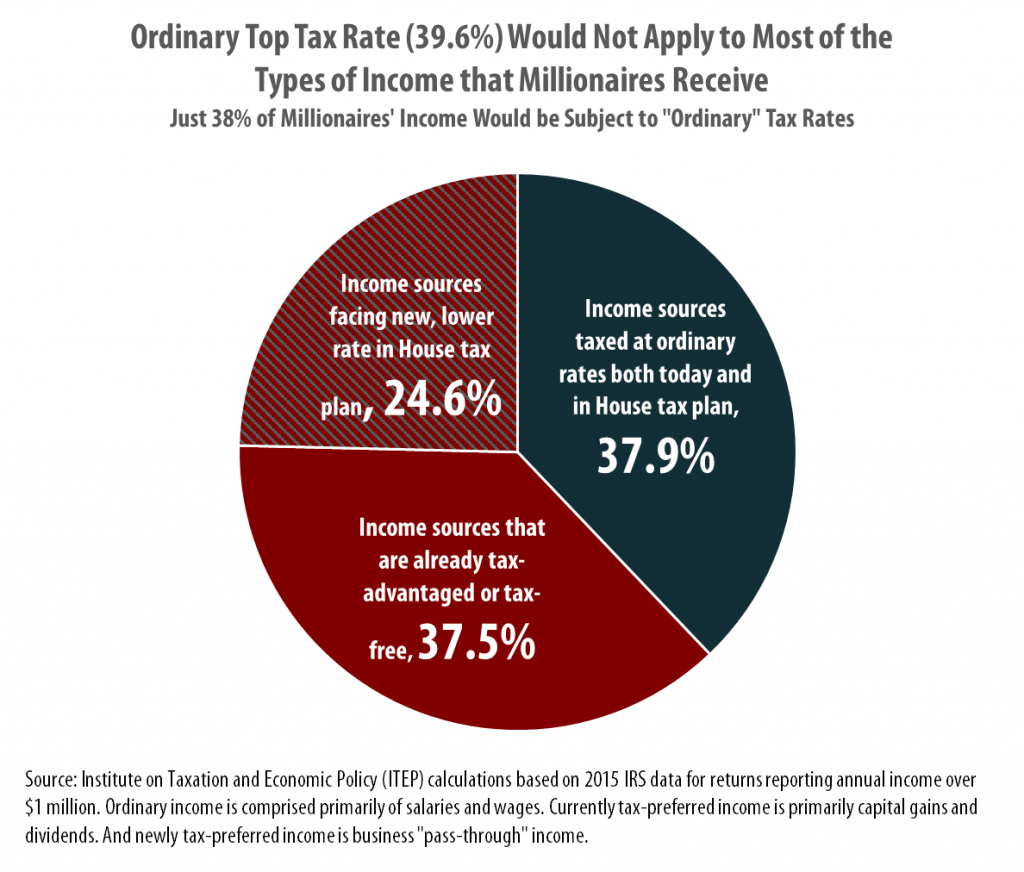

House Tax Plan Will Keep 39.6% Top Rate, But That Won’t Matter for Most Types of Income Going to the Rich

November 1, 2017 • By Carl Davis

In recent days, news that House tax writers will not seek to cut the top personal income tax rate below 39.6 percent on taxable income above $1 million has led some to question whether the newest iteration of the Trump-GOP tax plan will provide a major windfall to the wealthy—a fact that has so far been widely understood. Unfortunately, this second-guessing is unnecessary.

State Rundown 11/1: Connecticut Balances Budget, Leaves Tax Code Out of Whack

November 1, 2017 • By ITEP Staff

This week a "historic" but highly problematic budget agreement was finally reached in Connecticut, Michigan lawmakers banned localities from taxing any food or beverages, and Nebraska and North Dakota both got unpleasant news about future revenues. Also see our "what we're reading" section for news on 11 states that have run up long-term fiscal deficits since 2002 and the impacts of flooding on local tax bases.

ITEP in the News

CBS News: The One Big Beautiful Bill Act is 1 year old. Here are the winners and losers.

Yahoo News: Hawaii’s new ‘millionaire tax’ rivals top tax rate among other states

Lexington Herald-Leader: How are gas prices set in KY? From oil to the pump, here’s what to know

Wall Street Journal: Coke Takes on IRS With $20 Billion at Stake

Reuters: Hawaii Considers Gasoline Tax Suspension as Pump Prices Soar

ITEP Work in Action

Senator Chris Van Hollen: Van Hollen, Pettersen Lead Lawmakers in Introducing Legislation to Bring Transparency to Corporate Abuse of Tax Havens, Job Offshoring

Center on Budget and Policy Priorities: Missouri Tax Amendment Likely to Seriously Harm Services, Shift Taxes Onto Working Families

California Budget and Policy Center: Should Voters Approve Prop. 3? How Top Tax Rates Have Helped Californians

Migration Policy Institute: Rooted in the Valley: Immigrants in Napa County’s Communities and Economy

The Bell Policy Center: Colorado Ballot Guide 2026

Institute on Taxation

and Economic Policy

ITEP is a non-profit, non-partisan tax policy organization. We conduct rigorous analyses of tax and economic proposals and provide data-driven recommendations to shape equitable and sustainable tax systems.

Subscribe to ITEP Emails

Tax research and policy news in your inbox.

Promote Fair Tax Policy

Your gift to ITEP promotes tax justice. With your help, we do research that supports taxing millionaires and billionaires, taxing big corporations and raising revenue for the things our people, our communities and our planet need.

Together, we can create a country with more economic justice, more racial justice, more climate justice… and more tax justice.