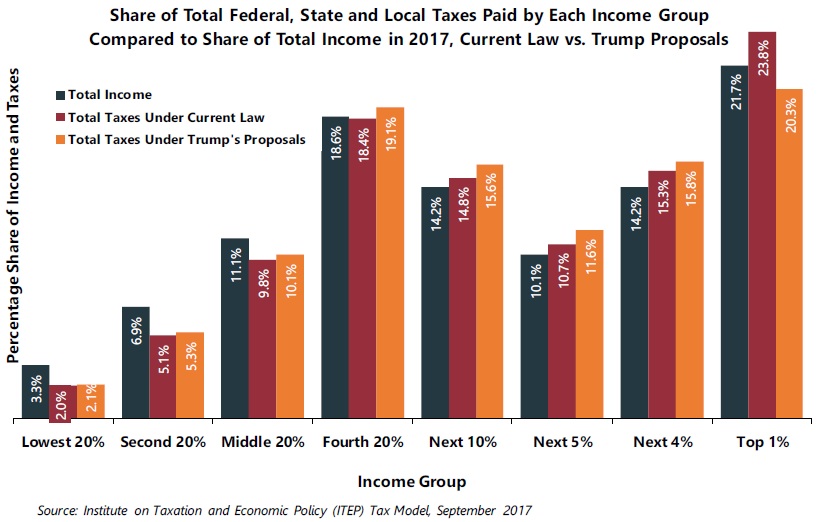

The tax proposals released by the Trump Administration in April would reduce the share of total federal, state and local taxes paid by America’s richest 1 percent while increasing the share paid by all other income groups. This clearly indicates that the tax system would be less progressive under the president’s approach. Although the president’s proposals would cut taxes across the board, tax cuts for lower- and middle-income households would be far smaller, even when measured as a share of household income, than the tax cuts for the rich.

As the graph above illustrates, the Institute on Taxation and Economic Policy (ITEP) tax model projects that the richest 1 percent of Americans will pay 23.8 percent of total federal, state and local taxes in 2017 under current law, but would pay just 20.3 percent of total taxes if Trump’s proposals were in effect. Under current law, the richest 1 percent pays a share of total taxes that is slightly greater than its share of total income. Under Trump’s proposals, this group would pay a share of total taxes that is less than its share of total U.S. income.

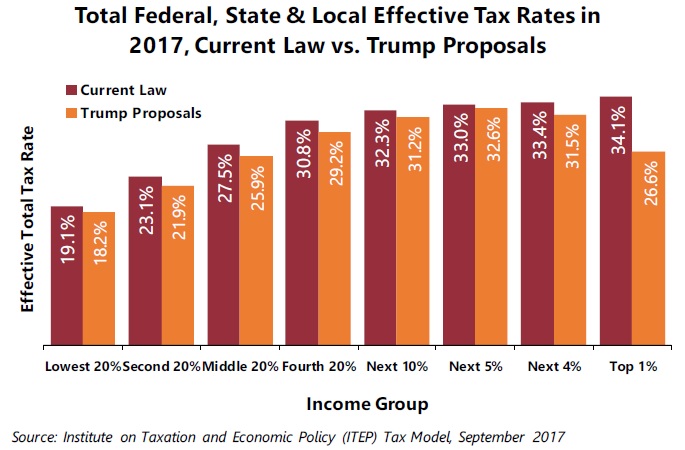

The effective total tax rate (the share of income paid in federal, state and local taxes) would change even more dramatically for the rich, as the graph below illustrates. Under current law, the richest 1 percent, who are projected to have an average income of $1.8 million this year, will pay a total effective tax rate of 34.1 percent, which is at least slightly higher than the rate paid by all other income groups.

But under Trump’s proposals, the richest 1 percent would pay an effective total tax rate of just 26.6 percent, close to the rate paid by the middle 20 percent of Americans, who will have an average income of just $50,500 this year. The tax code would lose the slight amount of progressivity it has at the top end, where it is most needed.

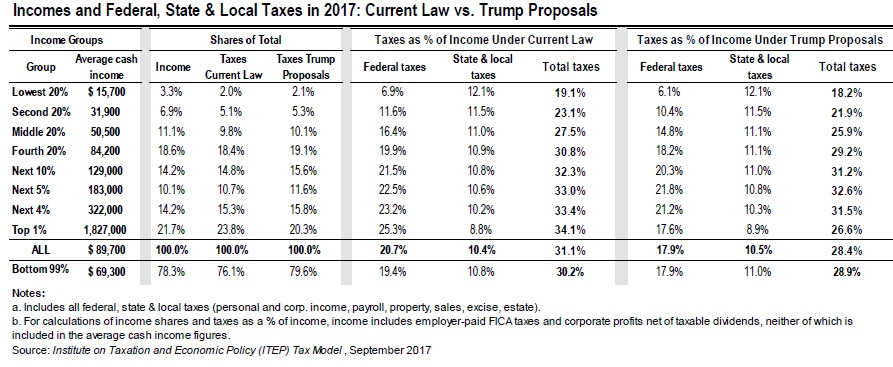

ITEP’s estimates of total taxes paid by different income groups and of effective total tax rates combine all the different types of taxes that Americans pay at the federal, state and local levels. The federal taxes include individual income taxes, corporate income taxes, payroll taxes, estate and gift taxes and excise taxes. The state and local taxes include individual income taxes, corporate income taxes, property taxes, sales taxes and other taxes.

Trump’s proposals would directly change federal individual income taxes, corporate income taxes and estate and gift taxes. These figures estimating the impact of these changes are an extension of ITEP’s previous analysis finding that 61.4 percent of the tax cuts under Trump’s proposals would go to the richest 1 percent of Americans and another analysis finding that 48.8 percent of the tax cuts would go to the half of 1 percent of Americans with income greater than $1 million.

The estimates are based on broad principles for tax policy released by the Trump Administration on April 26, 2017, as well as subsequent statements by administration officials. Because the principles and statements left many unanswered questions, the estimates required some assumptions that are explained in those previous reports. As explained in greater detail in those reports, these estimates include the following Trump proposals:

Repeal of the 3.8 percent tax on investment income for the rich.

Repeal of the Alternative Minimum Tax.

Repeal of personal exemptions and doubling of the standard deduction.

Replacement of current income tax brackets with three brackets, 10 percent, 25 percent, and 35 percent.

Elimination of all itemized deductions except those for charitable giving and home mortgage interest.

Special tax rate (15 percent) for businesses that do not pay the corporate income tax.

New deduction and tax credit for child care.

Repeal of special tax breaks for businesses and reduction in the corporate income tax rate from 35 percent to 15 percent.

Repeal of the estate tax.

This analysis also accounts for the indirect effects that the president’s tax proposals would have on state and local taxes. For example, as illustrated in the detailed table below, the effective state and local tax rate for the richest 1 percent would rise very slightly under the president’s proposals. This would happen because some states’ tax rules allow the same breaks that are available at the federal level, and the president’s proposals to eliminate those breaks from the federal tax code would cause them to disappear from those states’ tax codes as well. But as the table illustrates, the impact of this would be relatively small and completely overwhelmed by the reduction in the effective federal tax rate for the richest one percent.