Recent Work by ITEP

Tax Avoiding Companies Well Represented at Tax Reform Hearing

May 18, 2017 • By Richard Phillips

Today the House Ways and Means Committee will hold its first tax reform hearing of 2017, which marks the official opening of the tax reform debate in Congress. True tax reform, if the committee sought to achieve it, could create more jobs and ensure companies are paying their fair share by cracking down on the massive offshore tax avoidance that companies engage in. Unfortunately, the panel of witnesses for today’s hearing is largely made up of representatives of various major corporations that are beneficiaries of the loopholes in our current corporate tax laws. Given this, it seems likely that these…

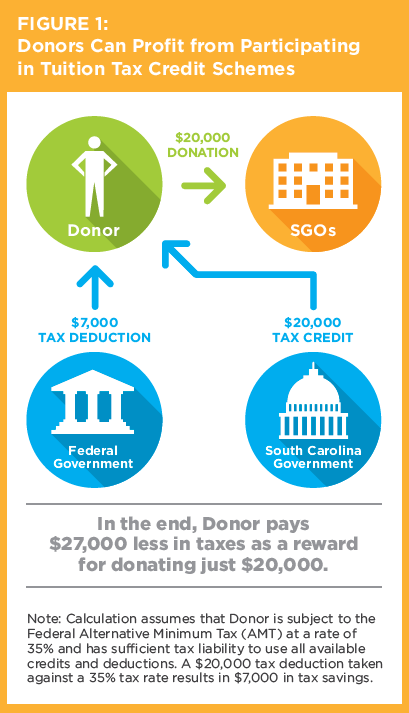

Investors and Corporations Would Profit from a Federal Private School Voucher Tax Credit

May 17, 2017 • By Carl Davis

A new report by the Institute on Taxation and Economic Policy (ITEP) and AASA, the School Superintendents Association, details how tax subsidies that funnel money toward private schools are being used as profitable tax shelters by high-income taxpayers. By exploiting interactions between federal and state tax law, high-income taxpayers in nine states are currently able […]

Public Loss Private Gain: How School Voucher Tax Shelters Undermine Public Education

May 17, 2017 • By Carl Davis, Sasha Pudelski

One of the most important functions of government is to maintain a high-quality public education system. In many states, however, this objective is being undermined by tax policies that redirect public dollars for K-12 education toward private schools.

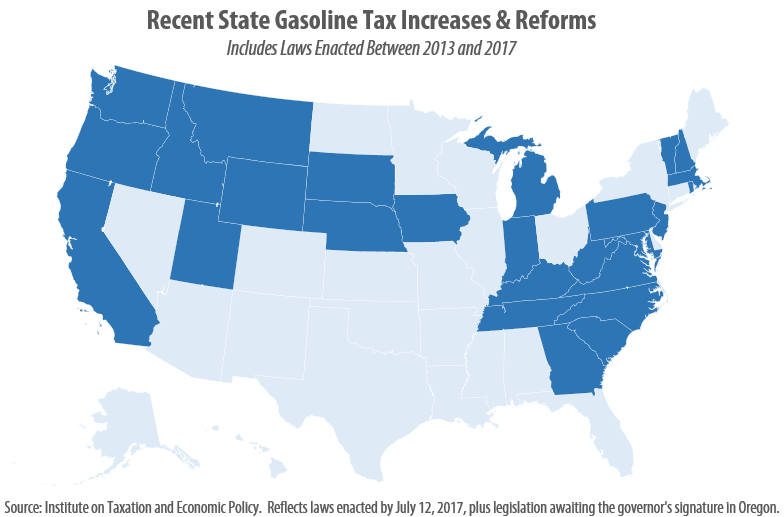

South Carolina’s Gas Tax Deal: Could Have Been Worse, Could Have Been Better

May 12, 2017 • By Dylan Grundman O'Neill

South Carolina lawmakers this week raised the state’s gas tax for the first time in 28 years, a time period that tied for the third-longest in the nation. While the increase was meaningful and hard-fought, the final result remains flawed in ways that could have been easily remedied or avoided. The biggest positive of the […]

State Rundown 5/10: Spring Tax Debates at Different Stages in Different States

May 10, 2017 • By Meg Wiehe

This week saw a springtime mix of state tax debates in all stages of life. In West Virginia and Louisiana, debates over income tax reductions and comprehensive tax reform are full of vigor. Other debates that bloomed earlier are now settled, such as Florida‘s now-complete budget debate and the more florid debates over gas taxes […]

This post was updated July 12, 2017 to reflect recent gas tax increases in Oregon and West Virginia. As expected, 2017 has brought a flurry of action relating to state gasoline taxes. As of this writing, eight states (California, Indiana, Montana, Oregon, South Carolina, Tennessee, Utah, and West Virginia) have enacted gas tax increases this year, bringing the total number of states that have raised or reformed their gas taxes to 26 since 2013.

Representative John Delaney’s Bills Take the Wrong Approach on Funding Infrastructure

May 9, 2017 • By Richard Phillips

Lawmakers across the political spectrum recognize the need for additional spending to maintain and upgrade our nation’s transportation infrastructure. According to the Federal Highway Administration, there is a backlog of $836 billion in needed repairs and improvements to roads and bridges and an additional $90 billion backlog of public transit projects. Maryland Democratic Representative John […]

President Donald Trump’s tax sketch released in late April is the starting point for federal tax reform discussions. For now, the sketch includes too few details to properly analyze its revenue and distributional impacts, but based on limited information, corporations and the wealthy stand to benefit most. Below are resources ITEP has produced on tax […]

Two states are on the verge of embracing a tried and tested anti-poverty policy, the Earned Income Tax Credit (EITC). In the past two weeks, lawmakers in both Hawaii and Montana passed EITC legislation, which governors in both states are expected to sign. Once officially enacted, these states will join 26 other states and the […]

Nebraska Vote Is Latest Defeat for Tax-Cut “Trigger” Gimmick

May 4, 2017 • By Dylan Grundman O'Neill

Nebraska lawmakers had a long and contentious tax-cut debate this session but ultimately chose the wise path and rejected attempts to give a massive tax cut to the wealthy at the expense of the state’s schools, other public services, low- and middle-income families, and property tax payers. Tax cut efforts in Nebraska last year ended […]

ITEP in the News

The Guardian: Billionaire Fortunes Have Reached All-Time Highs Under Trump. So Has the Movement To Tax Them

The Guardian: Washington State’s ‘Historic’ Millionaire Tax Takes Aim at Super-Rich – Will It Succeed?

Video: ITEP's Amy Hanauer Discusses How to Make the Federal Tax Code Fairer on WHYY

Politico: Governors Forgo Past Response to High Gasoline Prices

Stateline: Gas Prices Rise Again As Some States Consider Tax Holidays

ITEP Work in Action

FACT Coalition: Take the Money and Run – Amidst Oil Price Windfalls, U.S. Oil Majors Continue to Pay Less Tax at Home than Abroad

Brookings: The Caregiving Crisis and the 2026 Vote

Gov. Evers Vetoes Bill Requiring Wisconsin to Opt Into Nationwide Expansion of Private Voucher Schools

Oxfam: The Case for Fairly Taxing the Rich in New York

Economic Policy Institute: How ARPA State and Local Fiscal Recovery Funds Helped Ensure a Swift Post-COVID Recovery

Institute on Taxation

and Economic Policy

ITEP is a non-profit, non-partisan tax policy organization. We conduct rigorous analyses of tax and economic proposals and provide data-driven recommendations to shape equitable and sustainable tax systems.

Subscribe to ITEP Emails

Tax research and policy news in your inbox.

Promote Fair Tax Policy

Your gift to ITEP promotes tax justice. With your help, we do research that supports taxing millionaires and billionaires, taxing big corporations and raising revenue for the things our people, our communities and our planet need.

Together, we can create a country with more economic justice, more racial justice, more climate justice… and more tax justice.