Rhode Island’s new budget makes the state’s tax system fairer, responsibly raises and protects revenue, and provides additional funding to support working-class families in the state. The spending plan, signed into law by Gov. Dan McKee today, features:

- A new millionaires’ tax

- The state’s first, permanent child tax credit

- Expanded eligibility for its Social Security exemption

- Strategic decoupling from federal business tax provisions

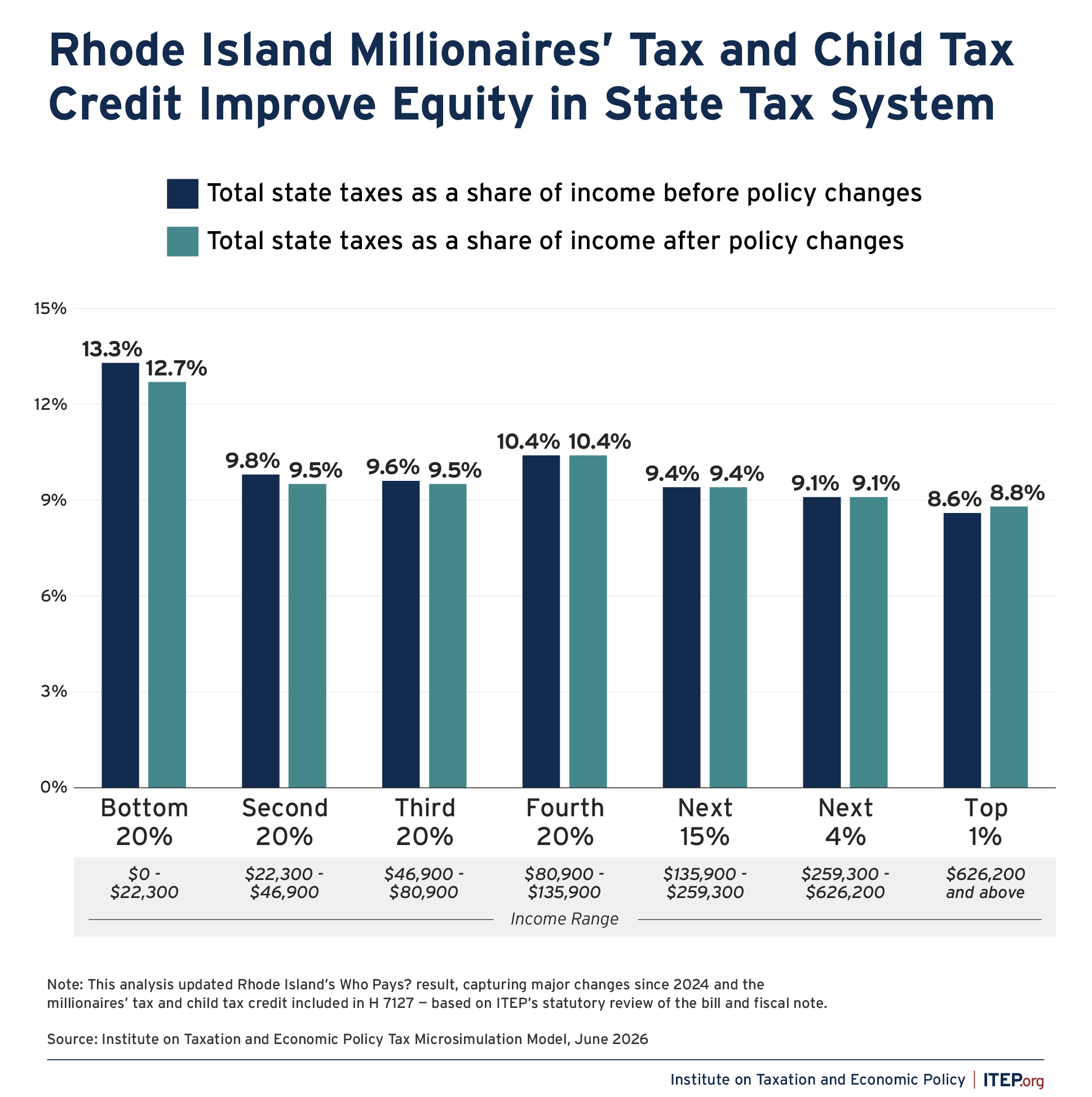

These changes will reduce the regressivity in Rhode Island’s tax system. Prior to this legislation, the bottom 20 percent of households paid an effective tax rate over 1.5 times higher than the top 1 percent. Rhode Island’s millionaires’ tax, coupled with the other progressive tax changes in this budget, help address that inequity. Rhode Island now joins Washington, Maine, and Hawai’i in enacting new taxes on high-income households in their states this year.

Figure 1

The new millionaires’ tax is a 3 percent surcharge on income over $1 million that will gradually phase in over the course of three years, by 1 percentage point per year, starting in 2027. This is estimated to raise more than $150 million a year once fully implemented. Rhode Island will also join 15 other states in providing its first permanent child tax credit, which will reduce poverty and boost economic security for the state’s children and their families. The fully refundable credit provides $330 per child age 18 and under and begins to phase out starting at incomes of $88,500 for single filers and $110,640 for married filers starting next tax year. Gov. McKee’s original proposal converted the state’s dependent exemption to a refundable tax credit since many low- and moderate-income families are unable to benefit from the dependent exemption. The final budget takes it one step further, maintaining the dependent exemption and allowing families to benefit from both – bringing real aid to families. The total annual benefit to families is estimated to be $46.6 million.

Breakdown of Child Tax Credit and Dependent Exemption Benefits

| Income group | Income range | Average benefit | ||

|---|---|---|---|---|

| Lowest 20% | $0 – $22,300 | $850 | ||

| Second 20% | $22,300 – $46,900 | $880 | ||

| Middle 20% | $46,900 – $80,900 | $1,130 | ||

| Fourth 20% | $80,900 – $135,900 | $630 | ||

| Next 15% | $135,900 – $259,300 | $450 | ||

| Next 4% | $259,300 – $626,200 | $290 | ||

| Top 1% | $626,200 and above | $0 | ||

| Total | $765 | |||

| Source: Institute on Taxation and Economic Policy Tax Microsimulation Model, June 2026 | ||||

The new budget also eliminates the age requirement to now include low-income seniors who elected to receive their Social Security benefits early because they may have had few or no other options for income as opposed to mandating they be 67 to benefit. Seniors still must have incomes under $107,000 for single filers and $133,750 for married filers in tax year 2025, to qualify. The final agreement wisely stops short of the original proposal to phase in a full exemption of all Social Security income from taxation regardless of income. That would have overwhelmingly benefited the wealthiest households in the state (about 90 percent of the nearly $42 million in tax cuts would have gone to the top 20 percent, according to our estimates).

Rhode Island will also decouple from some of the federal tax changes in the 2025 Trump tax law, protecting much-needed state revenue and ensuring the state’s tax policies are supporting Rhode Island residents and businesses. In Rhode Island, the federal tax law provided an estimated $58,840 in annual tax cuts to the richest 1 percent along with deep funding cuts to programs like SNAP and Medicaid.

In the budget, the state decoupled from federal corporate tax deductions for immediate and retroactive write-offs for research and development expenses, the expanded qualified small business stocks exclusion, which disproportionately benefit multimillionaire and billionaire venture capitalists, and the business interest limitation, which allows corporations to excessively leverage debt to reduce their tax bills. These deductions would have resulted in an estimated $22.6 million in lost state revenue each year that would have largely subsidized corporate investment in other states. The state could still go further to save millions more in revenue by completely decoupling from other problematic federal tax subsidies such as FDDEI and Opportunity Zones.

Nationwide, wealth inequality continues to grow unabated and has been amplified under the federal tax bill. However, Rhode Island’s latest budget demonstrates a growing trend across the country to claw back the massive federal tax giveaways to the wealthy, ask more of those with the most ability to pay, and responsibly invest in children and families. Through these tax policy decisions, Rhode Island made meaningful progress in improving the fairness of the state’s tax system and raised needed revenue to best support its communities.