The COVID-19 pandemic is an extraordinarily challenging time, as we see harm and struggle affecting the vast majority of our families, businesses, public services, and economic sectors. No one will be unaffected by the crisis, and everyone has a stake in the recovery and faces tough decisions.

In the world of state fiscal policy, where revenue shortfalls are likely to be far bigger than can be filled by the initial $150 billion in federal aid or absorbed through funding cuts without causing major harm, tax increases must be among those decisions. During the peak year of the Great Recession, states cumulatively faced a more than $220 billion revenue shortfall, and the fallout from this crisis will likely lead to substantially larger gaps.[1] Official shortfall projections in some cases already range up to 20 percent of state budgets or more,[2] with unprecedented sales tax declines leading the way.[3] A recent Center on Budget and Policy Priorities report projects shortfalls could amount to more than $500 billion.[4] Providing significant additional state and local aid should be a top priority of Congress’s next relief package. Even with more federal support, states will need home-grown revenue solutions in the short, medium, and long terms as the crisis and its fiscal fallout intensify, subside, and eventually give way to a new normal. States must balance their budgets, and research shows that they harm their economies when they choose deep funding cuts to vital public investments over increasing tax contributions from those who can afford them.[5]

In addition to these decisions about our future, the crisis also is forcing us to face difficult truths about our present and past. The pandemic’s disproportionate impacts on Black and brown people[6] reflect our collective failure to address race-based inequities throughout our economic and social systems. Its greater effects on low-income workers[7] betray decades of policies that have suppressed workers’ wages, funneled more of our economic resources to the already wealthy, allowed corporations and the rich to avoid taxes and, ultimately, led to neglect for investments that help families and communities thrive. The devastating effect of COVID-19 on state and local budgets is exposing longstanding shortcomings in state and local tax structures, which are in many ways inadequate, inflexible, inequitable, outdated, and upside-down.[8]

Where to Focus State Tax Policy Responses

Follow the Money: State tax policy responses to the COVID-19 pandemic should focus on addressing as many of the issues above as possible, and luckily there are specific policy options to help with many or all of them at once. States should focus first on generating needed revenue through tax increases on households, businesses, and sectors of the economy that continue to have high incomes, profits, and activity even during these troubled times. For states facing catastrophic revenue declines, asking more of taxpayers with a clear ability to pay is far preferable to cutting state budgets, which would lead to mass layoffs, steep cuts in public services, and a downward spiral in the economy.

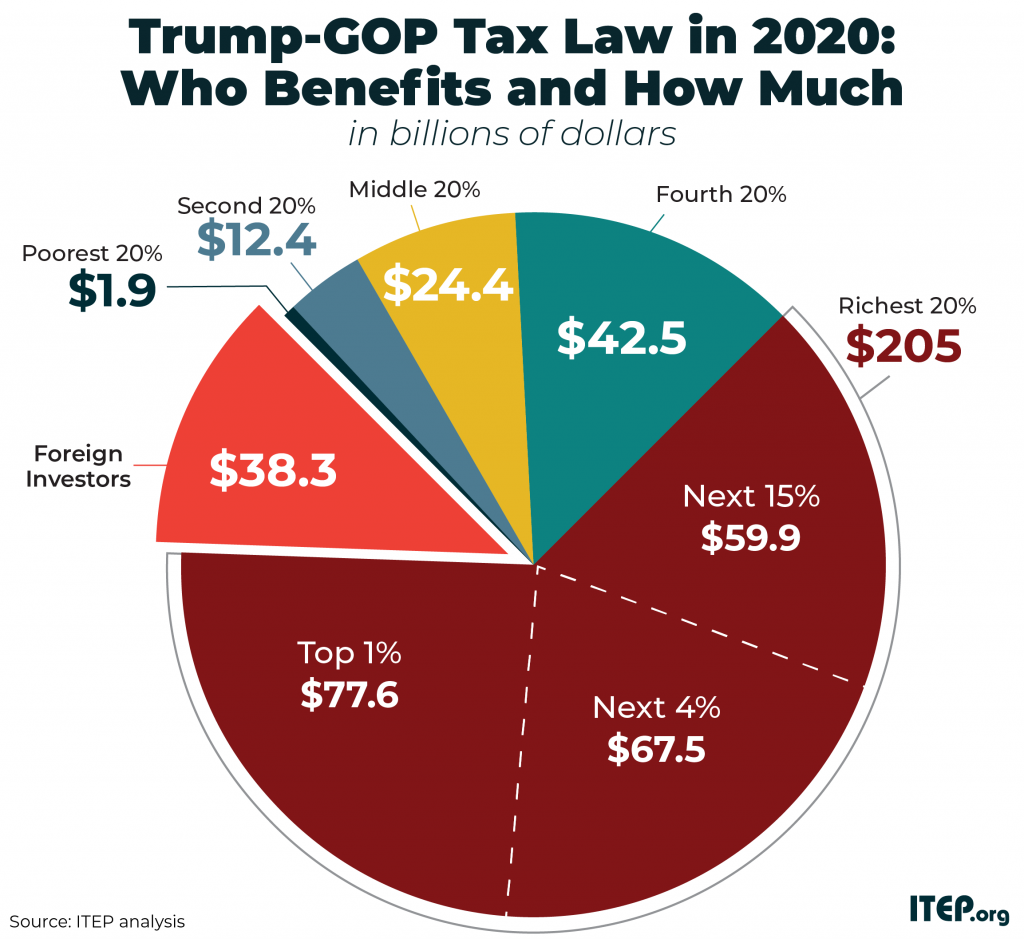

In many cases, the policies that focus on these groups also will modernize and improve state tax codes to address issues that long pre-date the current crisis. States and localities have historically asked the least of high-income households, even as public structures crumbled. ITEP’s 2018 Who Pays? report found on average, the lowest-income 20 percent of taxpayers face a state and local tax rate more than 50 percent higher than the top 1 percent of households. The federal government also recently cut taxes sharply for this group under the Tax Cuts and Jobs Act (TCJA). The top 5 percent of earners, for example, are expected to receive a federal tax cut as high as $145 billion this year from TCJA alone,[9] as well as additional tax cuts under more recent tax legislation. Put another way, states could collectively raise taxes on their richest residents by more than $100 billion this year without causing net tax bills to rise any higher than they would have under pre-TCJA law.

Combine Shovel-Ready Reforms with Laying New Foundations: To be sure, states will at times need to compromise some of these goals in the name of others. States’ current situations and easily achieved options vary greatly. In some states, the “shovel-ready” options—such as raising flat personal income tax rates or sales tax increases—have major flaws such as being embedded in long-outdated realities and leaning unfairly on the very people and communities already suffering the most. Some states may find that they need to fill their budget holes with a mix of imperfect options while laying the foundation for something better. They should not be afraid to start laying those foundations even if it requires a major effort to overcome anti-tax obstacles.

When in a Hole, Stop Digging: Many states enacted misguided tax cuts in recent years, some of which have not taken full effect yet. Similarly, many have coupled to recent federal tax giveaways and many have allowed ineffective business subsidies and other tax expenditures to erode their revenue systems. In these cases, a first step is to simply stop digging their own budget holes deeper, which can be achieved by cancelling or further delaying unimplemented cuts, reconsidering federal conformity decisions, revisiting tax expenditure lists, and reversing certain recent cuts.

Build More Than Sandcastles: The immediate crisis requires immediate action, and emergency measures will no doubt be part of state solutions, but states should not be fooled into thinking temporary measures will suffice. The COVID-19 pandemic is exposing and exacerbating fundamental failures in fiscal policy and beyond, but it is not the root cause of most of those failures.[10] States need bold reforms to address underlying flaws in their tax structures. Strengthening these systems will protect them against the current crisis and shifting tides to come, so that temporary fixes don’t just wash away after the storm.

Personal Income Taxes

Progressive income taxes are the surest way for states to simultaneously raise short-term revenue, prepare for longer-term economic trends, and redress longstanding adequacy and fairness issues in their tax codes. Income taxes adapt to economic shifts automatically because people with low or no income pay little or nothing, while people with higher incomes pay more: when restaurant workers are laid off their taxes decrease, when office workers are able to shift to remote work their taxes are maintained, and when adaptable businesses or pandemic profiteers manage to increase their incomes their taxes generally follow suit. Progressive income taxes have an inherent advantage of applying to the right people at the right time: those who have high incomes when they have high incomes.

But most state income taxes have not adapted to today’s astronomical economic inequalities. The table below shows that even most states with progressive income tax structures apply their top rates to middle- and sometimes low-income families. Of 42 states with personal income taxes, 27 apply their highest rate for single individuals to income below $100,000.[11] But in most states the vast majority—more than 80 percent—of residents had total 2019 taxable income below that amount, even when including married couples’ combined incomes. And 19 of those states apply their highest rate at taxable incomes below $20,000. Only five states begin their top bracket for single filers between $100,000 and $200,000, four between $400,000 and $1 million, and just two at over $1 million. In other words, there is already a great deal of room for states to update their income tax codes to apply higher rates to the highest incomes.

Raising Rates on Existing Upper-Income Brackets: Several states have income tax structures already in place with brackets spread out enough to allow them to easily ask more of their most fortunate residents simply by raising one or more existing rates. States as diverse as Connecticut, Hawaii, Maryland, Minnesota, New York, North Dakota, and Ohio are some examples where brackets already exist at around $100,000 and around $250,000 (for single filers; brackets for married couples are generally double those amounts) that would allow lawmakers to focus their efforts on roughly the highest-income 20 percent and 5 percent of residents, respectively.[12] In these states, lawmakers should focus on raising existing rates on higher-income earners.

Progressive Bracket Reforms: As explained above, even the states that have progressive income taxes are generally far behind in ensuring that their highest rates apply to only their highest-income residents. Many states have income brackets that represented real differences in incomes when they were established in the 1930s but have been scarcely adjusted for inflation or soaring inequality since. These states can create new upper-income brackets and consolidate some lower brackets to update their tax codes to reflect current realities and adjust them for inflation to ensure they do not fall behind in the future. Again, as a rough guideline, tax brackets starting at around $100,000 for single filers and $200,000 for married couples will generally focus on the most fortunate fifth of state residents, and brackets starting around $250,000 and $500,000 will focus on the top 5 percent of households.

High-Income Surcharges: Similar to adding marginal tax brackets on higher incomes, an income tax surcharge is calculated as a percentage of taxable income exceeding a set amount, such as an additional 3 percent on taxable income over $100,000 and/or an additional 5 percent on income over $1 million. A surcharge is calculated separately from the normal marginal tax rate structure and then added on.

Instituting a Personal Income Tax Surtax: A surtax differs from a surcharge in that it is calculated as a percentage of tax liability instead of a percentage of income. Similar to an automatic gratuity added to the bill for large parties at a restaurant, a state can require high-income taxpayers to calculate their tax bill as they normally would and then increase it by 10 percent, 20 percent, or some other amount. A surtax can also include multiple brackets. North Carolina, for example, applied a small, graduated surtax for two years during the Great Recession.[13]

Raising Flat Income Tax Rates: The nine states that currently have flat income taxes should first look to raise the current flat rate and immediately begin the process of overcoming any procedural or constitutional hurdles needed to convert them to progressive rate structures. (Indiana, Kentucky, and North Carolina can immediately convert to a graduated structure). In the meantime, and in cases where this is politically infeasible, raising flat rates can be somewhat better focused on higher-income households through a few means:

Increased standard deductions and personal and dependent exemptions can help insulate lower-income families from the rate increase.

Eliminating deductions and other benefits for upper-income households as described below expands the base of the tax to ensure that, at a minimum, high-income households are not paying a lower overall rate than low- and middle-income families. Expanding the base also means the rate increase may not need to be as large. For example, many states with flat income tax rates have large exclusions for retirement income that benefit even the states’ wealthiest older taxpayers.

Credits that mimic the effects of graduated rates can be implemented in many flat-tax states as well. Utah’s Taxpayer Tax Credit[14] and Pennsylvania’s Tax Forgiveness credit[15] are two examples of nonrefundable credits that essentially mimic a lower tax bracket. For states where this is an option, the concept could potentially be expanded on to mimic multiple brackets below the flat rate.

Other refundable and nonrefundable credits can be calculated in a myriad of ways to reduce the flat tax for low- and middle-income families.

Eliminating Poorly Targeted Tax Subsidies: Many states offer special tax benefits that predominantly are available to high-income households, such as some itemized deductions,[16] special treatment of “pass-through” business income, and breaks on capital gains. These were already highly questionable and maintaining them should be among the lowest of state priorities in extremely tight budget times like these. Eliminating such unnecessary subsidies can improve the breadth and fairness of tax codes while bringing in small to moderate amounts of revenue to help stave off harmful funding cuts and larger tax increases elsewhere.

Creating State Income Taxes: It may seem like an improbable uphill battle—and it is—but the nine states without broad-based income taxes should start working now to create and implement them. Nearly all of these states rely heavily on retail sales taxes that have plummeted amid social distancing and job loss. As we discuss below, raising those rates would shift taxes further to low- and middle-income families and would not likely be very effective with spending so low. Moreover, states like Florida, South Dakota, and Nevada supplement their sales tax revenues by heavily taxing tourists through taxes on hotels, rental cars, and so on—all of which also are currently stagnating. Consumption and tourism taxes also will be the first to crash again in the event of a future wave of infection. Alaska and Texas famously rely on oil tax revenues, but those too are sputtering amid an international oil price war, not to mention decreased driving during social distancing.

Enacting personal income taxes would do more than just help them weather the current crisis and better adjust to its lasting effects: it would also bring them in line with the advances in flexibility and fairness that most states adopted decades ago. Of the 42 current broad-based state income taxes, 16 were put in place in the 1930s as the Great Depression exposed how property-tax-reliant systems raised inadequate revenues and failed to target high-income households and profitable businesses. The COVID-19 pandemic could serve as a similar wake-up call for these nine remaining states. Revenues in these states are in immense trouble in both the short and long term, and seven of them are among the “terrible 10” most regressive state tax systems for charging much higher overall tax rates on low-income households. Even if it requires amending state constitutions and overcoming supermajority requirements, the effort will be worth it.

Corporate Income Taxes

Like personal income taxes, corporate income taxes automatically adjust in one very helpful way because they only apply to profitable companies and only in the years when they turn a profit. They are ultimately paid primarily by high-income owners and shareholders. But like personal income taxes, corporate income taxes have been under attack—despite years of booming bottom lines for many corporations—and have declined as a state revenue source. States can enact these taxes if they have none, strengthen and increase them in many states that do have them, and seek straightforward reforms to close loopholes and bring them into the 21st century.[17]

States have a range of ways to strengthen existing state corporate income taxes. They can revisit business tax subsidies and consider limits on them. They can use surcharges and surtaxes similar to those described above. They can increase corporate tax rates—a particularly appealing option in the wake of the Tax Cuts and Jobs Act (TCJA), which cut the federal corporate tax rate from 35 percent to 21 percent. States have options to at least partly roll back this mistake and recoup lost revenue that matters now more than ever. States also could apply a corporate surtax, similar to what we described earlier for personal income taxes. North Carolina took this approach during the Great Recession.

Another option is to return to the traditional “three-factor” formula for determining what portion of each business’s profits should be taxed by each of the states in which it operates, rather than the problematic single sales factor (SSF) apportionment formula that has grown in prominence in recent years. Under SSF, multi-state corporations pay tax based solely on where their customers are located. But companies that have much, or all, of their property and workforce located in a given state, while making most of their sales to customers located outside that state, can end up paying little in state corporate income tax.

Combined reporting is another key reform that would tackle tax avoidance and recoup state revenue. It requires large companies who operate in multiple states to calculate profits of their various branches and subsidiaries into one single report. They then allocate profits to the states in which they operate.

One shorter-term policy states could consider is a special tax on “windfall” or “excess” profits of the few corporations who will receive a business boon during the pandemic. Such a tax last was used federally in the 1940s to help fund war efforts, so the concept would need to be re-imagined to be effective at the state level and reflect today’s economy and business structures but may be worth exploring.[18]

The coronavirus pandemic has devastated many small businesses, whose owners will struggle to make ends meet or reopen their doors. But it’s important to note that corporate income taxes are a tax on profits. When a company is profitable, in any given year, they should pay toward the maintenance of public services and an economy that works for everyone.

Sales and Consumption Taxes

Modernize Sales Tax Bases: Retail sales are currently down across the board, but states can mitigate their losses by updating their tax bases to include goods and services that have been overlooked so far or are likely to become even more important going forward. For example, many states have been lacking in taxation of digital downloads, services, and streaming. And services generally are still undertaxed despite growing as a share of total consumption for decades.

Require Sales Tax Collection by E-Retailers and Large Online Marketplaces: Most states have adopted laws to enforce sales taxes on online sales, but Florida and Missouri still need to do so. And those two states along with Kansas, Louisiana, and Mississippi still need to require collection by large online marketplaces like Amazon Marketplace, eBay, and Etsy.[19]

Update Excise Taxes: Some state excise taxes on products like alcohol, tobacco, and gasoline have fallen far out of date. Because these taxes are charged as a certain dollar or cent amount per unit (gallon, pack, pound, etc.), they steadily lose value if they are not adjusted for inflation or periodically increased. But 10 states have gone more than two decades without a gas tax update,[20] and similar periods have elapsed for other state excise taxes.

Mitigate Regressive Tax Increases with Refundable Credits Where Possible: Raising sales tax rates should not be the first place lawmakers look for new revenue. Sales taxes are highly regressive, have been decimated by stay-at-home orders, and will not be a particularly effective revenue generator for the foreseeable future. But states with major obstacles to enacting income taxes may find that they have few readily available alternatives that can be implemented in time to deal with the looming revenue crisis. States that must rely on sales taxes to keep public services and institutions operating should broaden the tax base as described above instead of, or alongside, any rate increase. And any state raising sales taxes, even those without income taxes in place, should use refundable tax credits to offset these taxes on the lowest-income and most vulnerable families. These groups are already paying the highest overall taxes in nearly every state, and particularly so in the states relying most heavily on sales taxes.

Removing Anti-Tax Straitjackets

Many states face statutory, procedural, or constitutional restrictions on their ability to implement the options listed here, such as constitutional bans on income taxes and supermajority provisions requiring higher vote thresholds for tax increases.[21][22] As states seek revenue solutions, they can look to overcome or remove these unnecessary impediments, which often have been put in place by anti-tax interests to lower taxes on their favored groups and remove lawmakers’ and residents’ flexibility to respond nimbly when revenues turn downward, forcing them instead to slash funding for shared priorities or lean even harder on low- and middle-income families to fund them.

Local Revenue Options

State laws determine the revenue options that local governments like cities, counties, and school districts get to choose from. In most states those options are limited to slightly regressive property taxes, harshly regressive sales taxes, and similarly regressive fines and fees. States often also impose caps on how high local tax rates can be and how much they can grow. Localities suffering pandemic-related budget issues will therefore largely be forced to turn to regressive revenue sources unless states grant them flexibility to pursue more equitable options. These options include empowering localities to: progressively tax income through graduated local income taxes or income surtaxes calculated as a percentage of state income taxes; tax mansions, second homes, or commercial property at higher property tax rates; and tax large corporations through various means.[23]

Conclusion

Of the many challenges the COVID-19 pandemic forces us to face, one is a reckoning with wealth and power and their influence on our political systems. History and public policies have provided social and economic advantages to the wealthy and powerful while denying opportunity to others, particularly communities of color. This has created an unequal structure whose imbalances and inequities are being laid bare in this historic moment. While everyone is affected by the crisis, this unequal structure has equipped higher-income taxpayers with the means to remain economically secure throughout this crisis. State tax policies have historically advantaged the richest among us by allowing them to pay a lower effective tax rate than the poorest 20 percent. Policy responses must keep these structural challenges in mind and demand a fair contribution from those most fortunate residents while building a stronger and more equitable foundation going forward.

[1] Naomi Nix. “Governors Seek $500 Billion For Shortfalls as Congress Squabbles,” Bloomberg, April 11, 2020. https://www.bloomberg.com/news/articles/2020-04-11/u-s-governors-request-500b-for-budget-shortfalls-from-virus.

[2] Center on Budget and Policy Priorities. “States Start Grappling With Hit to Tax Collections,” April 2, 2020. https://www.cbpp.org/research/state-budget-and-tax/states-start-grappling-with-hit-to-tax-collections.

[3] Meg Wiehe and Carl Davis. “Sales Taxes and Social Distancing: State and Local Governments May Face Their Steepest Sales Tax Decline Ever,” Institute on Taxation and Economic Policy, April 2, 2020. https://itep.org/sales-taxes-and-social-distancing-state-and-local-governments-may-face-their-steepest-sales-tax-decline-ever/.

[4] Elizabeth McNichol, Michael Leachman, and Joshuah Marshall. “States Need Significantly More Fiscal Relief to Slow the Emerging Deep Recession,” Center on Budget and Policy Priorities, April 14, 2020. https://www.cbpp.org/research/state-budget-and-tax/states-need-significantly-more-fiscal-relief-to-slow-the-emerging-deep.

[5] Nicholas Johnson. “Budget Cuts or Tax Increases at the State Level: Which Is Preferable When the Economy Is Weak?,” Center on Budget and Policy Priorities, April 28, 2010. https://www.cbpp.org/research/budget-cuts-or-tax-increases-at-the-state-level.

[6] Emma Coleman. “Black Americans Face Higher Rates of Coronavirus Infection,” Route Fifty, April 7, 2020. https://www.routefifty.com/health-human-services/2020/04/race-data-coronavirus/164428/.

[7] Derek Thompson. “The Coronavirus Will Be a Catastrophe for the Poor,” The Atlantic, March 20, 2020. https://www.theatlantic.com/ideas/archive/2020/03/coronavirus-will-supercharge-american-inequality/608419/.

[8] Institute on Taxation and Economic Policy. “Who Pays? A Distributional Analysis of The Tax Systems in all 50 States,” October 2018. https://itep.org/whopays/.

[9] Institute on Taxation and Economic Policy. “TCJA by the Numbers, 2020,” August 28, 2019. https://itep.org/tcja-2020/.

[10] Jenice R Robinson. “Returning to the Economic Status Quo After COVID-19 Crisis Should Not Be an Option,” Institute on Taxation and Economic Policy, April 6, 2020. https://itep.org/returning-to-the-economic-status-quo-after-covid-19-crisis-should-not-be-an-option/.

[11] Nine of these are flat rates

[12] These figures are based on 2019 incomes. While income levels in 2020 and beyond are unknown, with incomes likely to be generally lower at least in 2020, policies that focus on the highest-income groups based on 2019 incomes will likely apply to even smaller groups in 2020.

[13] North Carolina Department of Revenue. “Income Tax Surtax.” https://www.ncdor.gov/income-tax-surtax.

[14] Utah State Tax Commission. “Taxpayer Tax Credit.” https://incometax.utah.gov/credits/taxpayer-tax-credit.

[15] Pennsylvania Department of Revenue. “Tax Forgiveness.” https://www.revenue.pa.gov/GeneralTaxInformation/Tax%20Types%20and%20Information/PIT/TaxForgiveness/Pages/default.aspx.

[16] Carl Davis. “State Itemized Deductions: Surveying the Landscape, Exploring Reforms,” Institute on Taxation and Economic Policy, February 5, 2020. https://itep.org/state-itemized-deductions-surveying-the-landscape-exploring-reforms/.

[17] Aidan Davis. “Five Ways States Can Recoup Corporations’ Massive Federal Tax Giveaway,” Institute on Taxation and Economic Policy, March 2, 2018. https://itep.org/five-ways-states-can-recoup-corporations-massive-federal-tax-giveaway/.

[18] Reuven Avi-Yonah. “It’s Time to Revive the Excess Profits Tax,” The American Prospect,” March 27, 2020. https://prospect.org/coronavirus/its-time-to-revive-the-excess-profits-tax/.

[19] Institute on Taxation and Economic Policy. “A Visual History of Sales Tax Collection at Amazon.com,” April 1, 2020. https://itep.org/a-visual-history-of-sales-tax-collection-at-amazon-com/.

[20] Carl Davis. “How Long Has It Been Since Your State Raised Its Gas Tax?,” Institute on Taxation and Economic Policy, February 26, 2020. https://itep.org/how-long-has-it-been-since-your-state-raised-its-gas-tax/.

[21] Center on Budget and Policy Priorities. “State Supermajority Rules to Raise Revenues,” February 5, 2018. https://www.cbpp.org/sites/default/files/atoms/files/PolicyBasics-StateSupermajorities-4-22-13.pdf.

[22] National Conference of State Legislatures. “Supermajority Vote Requirements to Pass the Budget,” November 9, 2018. https://www.ncsl.org/research/fiscal-policy/supermajority-vote-requirements-to-pass-the-budget635542510.aspx.

[23] Daniel Beekman. “Seattle City Council sends proposal for tax on big businesses to its budget committee,” April6, 2020. https://www.seattletimes.com/seattle-news/politics/seattle-city-council-sends-proposal-for-tax-on-big-businesses-to-its-budget-committee/.