Property Taxes

From Congressional discussions over the so-called "One Big Beautiful Bill Act" to debates on property taxes, ITEP kept busy this year analyzing tax proposals and showing Americans across the country how tax decisions affect them.

His 900-word New York Times op-ed identifies some sensible federal tax reform ideas that would create a fairer, more sustainable tax system.

Texas Property Tax Plan Mimics California’s Damaging Prop 13

December 19, 2025 • By Neva Butkus, Rita Jefferson

This proposal would disrupt the state’s housing market and jeopardize local revenues while doing very little to help workers and families struggling to pay their property tax bills – just as Prop 13 did in California.

Vacancy taxes will not single-handedly solve problems in cities, but they are worth considering to address housing shortages, land use, and building thriving communities.

In 2025, Voters Said Yes to Public Resources and Community Investments

November 6, 2025 • By Rita Jefferson

Important tax measures were on the ballot this week, and the outcomes are clear: many voters support new state and local spending to support critical services in their communities.

Making the Wealthy Pay their Fair Share is the Way to Preserve Vacation Towns

September 10, 2025 • By Rita Jefferson

Rhode Island lawmakers created a new surcharge on second homes worth more than $1 million as part of the budget enacted this spring.

State Tax Action in 2025: Amid Uncertainty, Tax Cuts and New Revenue

July 28, 2025 • By Aidan Davis, Neva Butkus, Marco Guzman

Federal policy choices on tariffs, taxes, and spending cuts will be deeply felt by all states, which will have less money available to fund key priorities. This year some states raised revenue to ensure that their coffers were well-funded, some proceeded with warranted caution, and many others passed large regressive tax cuts that pile on to the massive tax cuts the wealthiest just received under the federal megabill.

Anti-Tax Revolts Backfire: What We’ve Learned from 50 Years of Property Tax Limits

July 15, 2025 • By Rita Jefferson

Across-the-board property tax cuts create less fair local tax systems in the long run. State legislators and local governments should prioritize the residents who can least afford their property taxes, not the residents and businesses who can.

Housing Affordability and Property Taxes: How to Actually Move the Needle

March 19, 2025 • By Kamolika Das, Rita Jefferson

Tax policy alone cannot solve the housing crisis but lawmakers who are focused on tax policy solutions have better options available than sweeping property tax cuts and caps: property tax circuit breakers, renter credits, vacancy taxes, land value taxes, and changes to existing property tax assessments can move the needle on the affordable housing crisis.

Circuit Breakers Are a Better Option for Property Tax Relief

March 13, 2025 • By Brakeyshia Samms

To curb the impact of property taxes on working families, lawmakers should improve or implement a property tax circuit breaker program. The program works like this: when families are overloaded with their property taxes, the circuit breaker kicks in and helps alleviate the pressure these taxes put on family budgets.

A Well Targeted Federal Renter Credit Could Help Reduce Wealth Gaps

March 3, 2025 • By Brakeyshia Samms

While lawmakers often speak about income inequality, less attention is paid to wealth inequality. Wealth is distributed even more unequally than income in the U.S. in ways that reinforce racial divides, leave some households with too little to handle unexpected expenses, and enable some households to pass down enormous intergenerational wealth. A renter tax credit is one tool lawmakers can use to reduce wealth inequalities both within racial and ethnic groups and between these groups. As we show in our new analysis, Black and Hispanic households are more likely to be renters and hold less wealth than white households.

High-Rent, Low-Wealth: Addressing the Racial Wealth Gap through a Federal Renter Credit

March 3, 2025 • By Brakeyshia Samms, Emma Sifre, Joe Hughes

While the federal tax code has some policies focused on raising income of low earners, it contains fewer provisions designed specifically to address wealth inequality. A renter tax credit offers a simple, administratively practical means of reaching low-wealth populations through the federal tax code without requiring a comprehensive measurement of every household’s wealth.

Learn from Prop 13 History to Avoid Repeating Past Mistakes

February 26, 2025 • By Rita Jefferson

Worries about housing costs and property tax bills are leading people to check the history books for solutions, but there’s a danger that they’ll repeat past mistakes. If anti-tax lawmakers carelessly weaken property taxes as they did in the 1970s, as they did with California’s Proposition 13, they will undercut public finances, making municipalities, school districts, and other special districts worse off.

In the face of immense uncertainty around looming federal tax and budget decisions, many of which could threaten state budgets, state lawmakers have an opportunity to show up for their constituents by raising and protecting the revenue needed to fund shared priorities. Lawmakers have a choice: advance tax policies that improve equity and help communities thrive, or push tax policies that disproportionately benefit the wealthy, drain funding for critical public services, and make it harder for most families to get ahead.

Policymakers Unwisely Propose Cutting Property Taxes in Favor of Sales Taxes

January 14, 2025 • By Rita Jefferson

Lawmakers across the country are taking aim at property taxes with a new strategy: raising sales taxes instead. Doing so would create a regressive tax shift that puts unfair burdens on renters and reduces the strength of local government revenues.

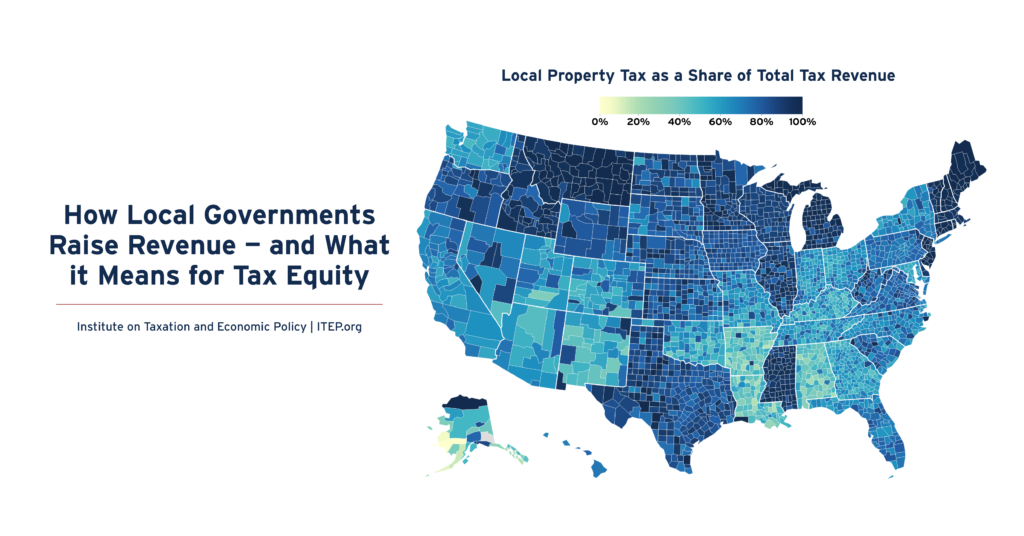

How Local Governments Raise Revenue — and What it Means for Tax Equity

December 5, 2024 • By Galen Hendricks, Rita Jefferson

Local taxes are key to thriving communities. One in seven tax dollars in the U.S.—about $886 billion annually—is levied by local governments in support of education, infrastructure, public health, and other priorities. Three fourths of this funding comes from property taxes, 18 percent comes from sales and excise taxes, and six percent comes from income taxes.

On Election Day, Voters Across the Country Chose to Invest in Their States & Communities

November 19, 2024 • By Kamolika Das

On election day, voters across the country — in states red and blue and communities rural and urban — approved a wide range of state and local ballot measures on taxation and public investment. The success of these measures clearly shows that voters are willing to invest in public priorities that feel tangible and close to home.

Billionaires and businesses have too much power in Washington. Tax revenue is needed to pay for things we all need. If we want economic justice, racial justice and climate justice, we must have tax justice.

2024 Local Tax Ballot Measures: Voters in Dozens of Communities Will Shape Local Policy

October 17, 2024 • By Rita Jefferson

Next month, voters across the country will weigh in on many local ballot measures that will have a profound effect on the adequacy of our local tax systems and whether cities and communities can fund public needs. These are in addition to statewide ballot questions, many of which have local implications this year.

Many cities, counties, and townships across the country are in a difficult, or at least unstable, budgetary position. Localities are responding to these financial pressures in a variety of ways with some charging ahead with enacting innovative reforms like short-term rental and vacancy taxes, and others setting up local tax commissions to study the problem.

Major tax cuts were largely rejected this year, but states continue to chip away at income taxes. And while property tax cuts were a hot topic across the country, many states failed to deliver effective solutions to affordability issues.

Property Tax Circuit Breakers Can Help States Create More Equitable Tax Codes

June 24, 2024 • By Brakeyshia Samms

Well-designed property tax circuit breaker programs allow states to reduce the impact that property taxes have on the upside-down tilt of their tax codes.

Juneteenth is a reminder of the hard-fought victories that helped Black Americans secure their delayed freedom, justice, and suffrage. And in the chapters about tax policy, the tales are no less fraught. From America’s prologue to the last paragraph of the Civil War, governments raised more tax revenue from the taxation of Black bodies than […]

Tax History Matters: A Q&A with Professor Andrew Kahrl, Author of ‘The Black Tax’

April 24, 2024 • By Brakeyshia Samms

In his new book, The Black Tax: 150 Years of Theft, Exploitation, and Dispossession in America, Professor Andrew Kahrl walks readers through the history of the property tax system and its structural defects that have led to widespread discrimination against Black Americans.

Ahead of the ‘Bring Chicago Home’ Vote, Remember That Local Mansion Taxes are Tried and Tested

March 14, 2024 • By Andrew Boardman, Kamolika Das

As Chicago and other localities look for ways to shore up resources for critical public investments, it's important to remember that over a dozen cities and counties have already benefited from policies like mansion taxes.

Institute on Taxation

and Economic Policy

ITEP is a non-profit, non-partisan tax policy organization. We conduct rigorous analyses of tax and economic proposals and provide data-driven recommendations to shape equitable and sustainable tax systems.

Subscribe to ITEP Emails

Tax research and policy news in your inbox.

Promote Fair Tax Policy

Your gift to ITEP promotes tax justice. With your help, we do research that supports taxing millionaires and billionaires, taxing big corporations and raising revenue for the things our people, our communities and our planet need.

Together, we can create a country with more economic justice, more racial justice, more climate justice… and more tax justice.