Nearly one year after the Trump tax law was signed, many of the 42 states with income taxes are declining to incorporate significant parts of the new law into their own tax codes. Some states have had contentious debates, and some are yet undecided on whether to conform.

The problem for states is that incorporating Trump tax law provisions into state tax codes would neither boost state economies nor help families make ends meet. And the revenue states would lose from conforming to the tax breaks would reduce money available for services like schools, healthcare, and human services, just as the federal government is cutting support for many of those same things.

Meanwhile, the Trump tax law is delivering enormous federal tax cuts to wealthy families in every state.

In most states, the starting point for state income tax calculations is the federal definition of income, and states incorporate other federal tax rules as well. About half the states with income taxes use “rolling conformity,” meaning that they automatically adopt federal tax changes as they occur. Most of the remainder use “static conformity,” meaning that they conform to the code as of a specific date; historically, these states routinely updated their codes with little debate. Either way, the outcome from conformity to much of the Trump law would be significant loss of revenue.

Several states simply accepted that loss of revenue with relatively little debate. In many other states, however, the degree and nature of conformity to the new federal law is complex. States, if they choose, can order a la carte from the new federal law’s provisions, conforming to some but not others. Many states appear to be doing just that, sometimes in surprising ways. So 12 months after the Trump tax law’s passage, the landscape of state conformity choices is still in flux. A few patterns are emerging, though.

- Many states are rejecting some or all the federal bill’s new corporate tax breaks. The decision to reject the corporate tax breaks crosses party lines. Republican-led states like Florida, Georgia, and Idaho have joined states led by Democrats, like California and Maryland, in rejecting the corporate tax breaks.

- Some states are using this moment to strengthen their corporate taxes through more thoughtful conformity to the shifting realities of the federal corporate income tax. New Mexico and Vermont each adopted innovative approaches to cracking down on corporate profit shifting, while Vermont also repealed a nonsensical deduction for foreign export profits.

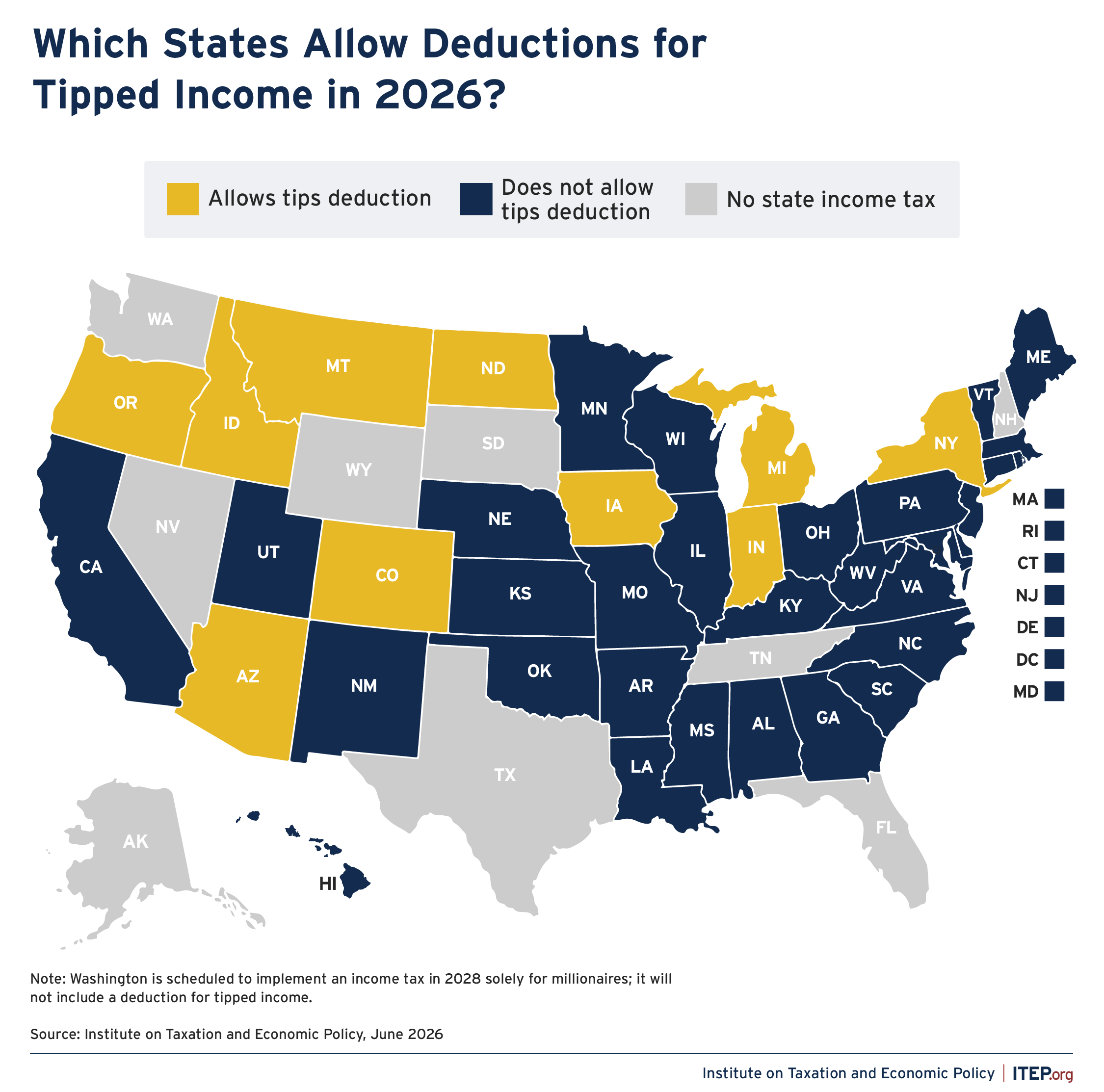

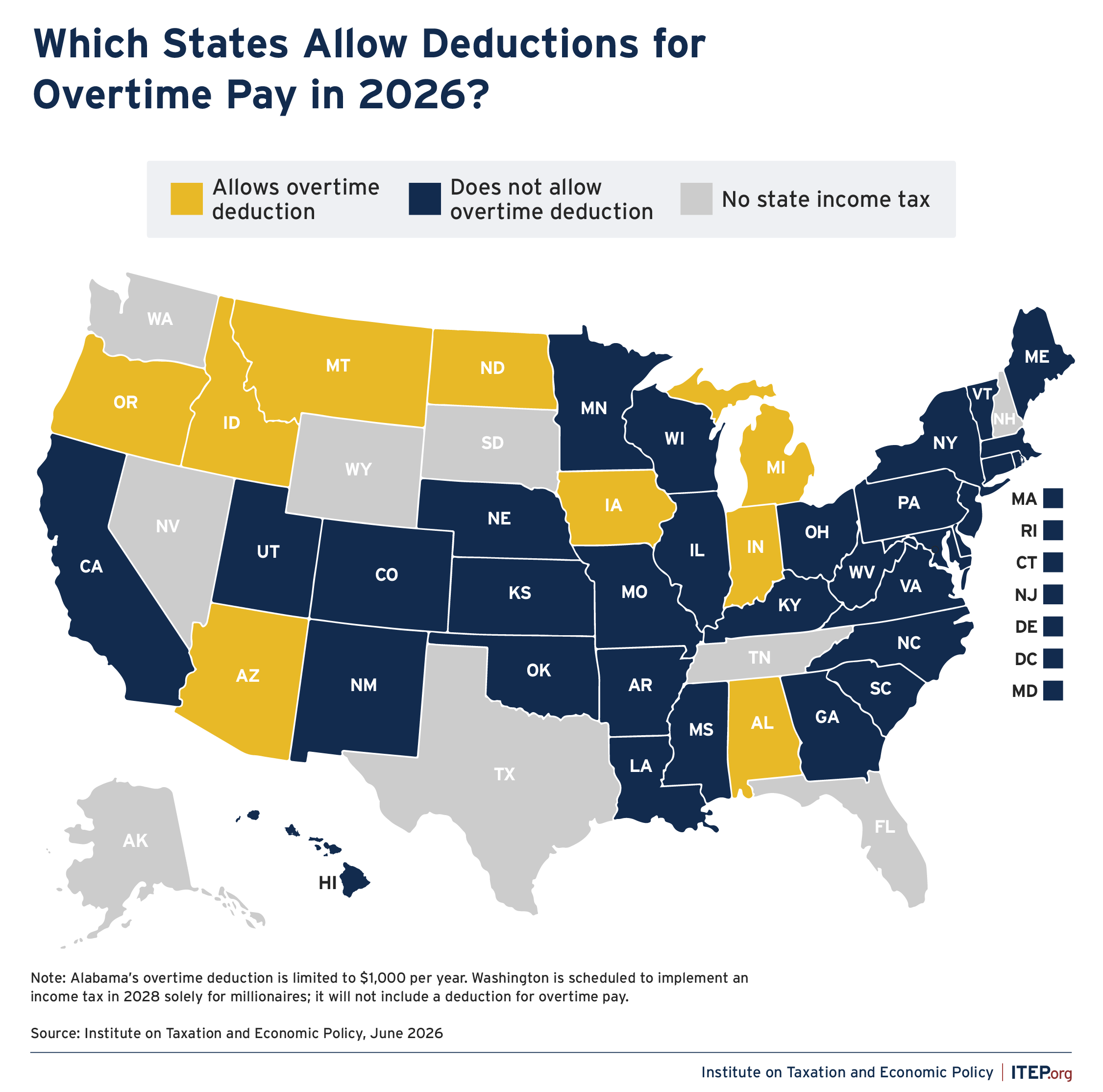

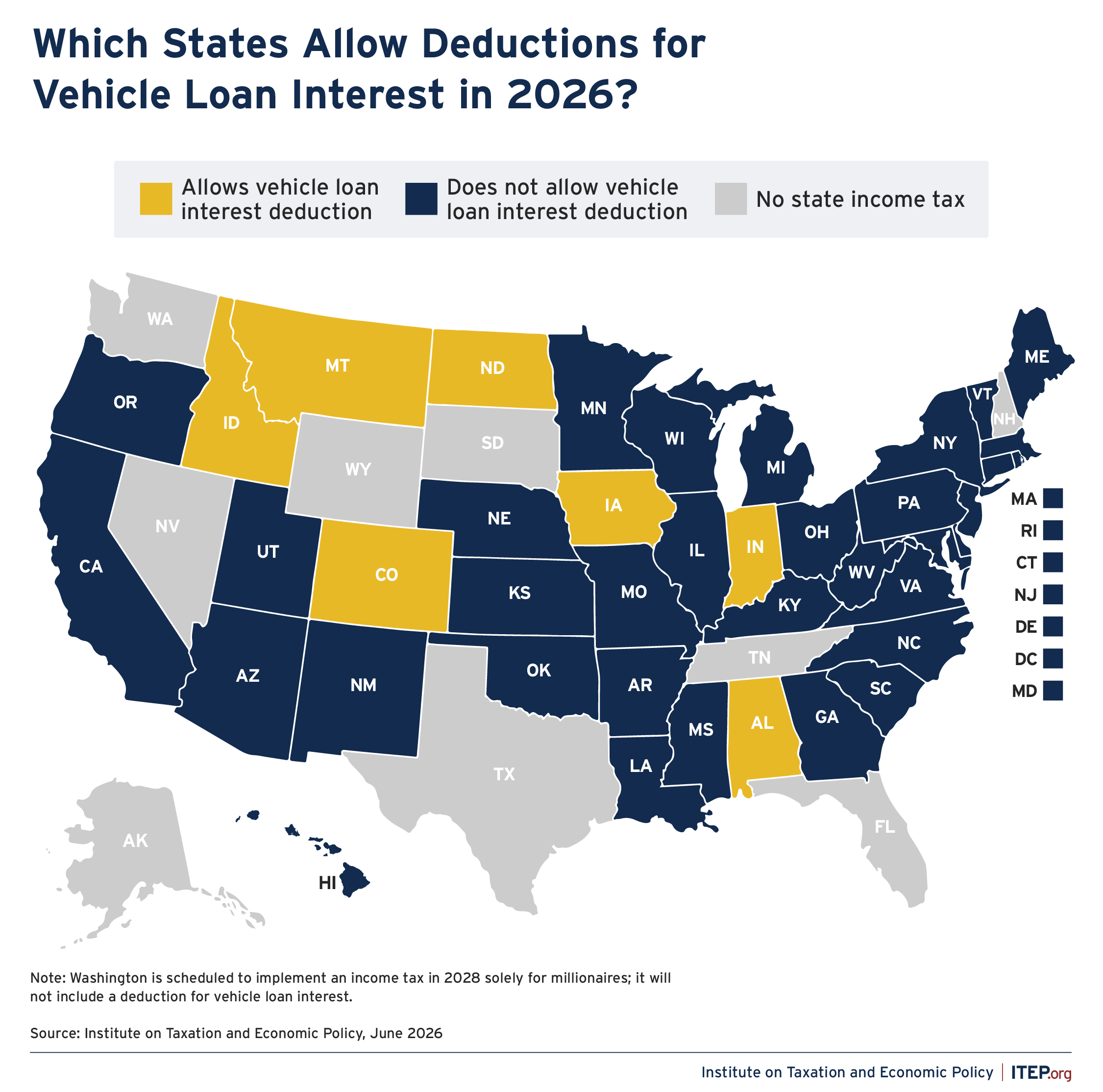

- The federal deductions for up to $25,000 in tipped income, for a similar amount of overtime pay, and for some auto loan payments have not been widely adopted by states. As of late June, only 10 states – a quarter of the states with personal income taxes — have decided to allow the tipped income deduction for tax year 2026, and just nine are allowing the deduction for overtime. Even in states that adopt these rules, many workers who receive these types of income will not benefit from the tax breaks, because their overall incomes are too low to have any income tax liability against which to claim the deductions.

Figure 1

Figure 2

Figure 3

The result is a patchwork of conformity across states as different states conform to different combinations of provisions. For example:

- Michigan, New York, and Oregon will allow taxpayers to deduct tips, as the new federal law does, but they will bar corporations from claiming the Trump law’s immediate write-offs for research and development expenditures and for certain manufacturing plants.

- By contrast, Massachusetts, Ohio, and West Virginia are taking the opposite approach. Each of these states has declined to adopt the tips deduction but is allowing those federal corporate write-offs, although Massachusetts is phasing them in rather than allowing them immediately.

Further muddying the picture, some states are conforming partially by tweaking the federal rules. Indiana and Michigan taxed tips and overtime income in 2025 but will allow the federal deductions for those items in 2026. Alabama is allowing only the first $1,000 of overtime to be exempt. Minnesota is allowing the federal research and experimentation tax write-offs for businesses that are structured as S corporations, limited liability companies, partnerships, and sole proprietorships, but disallowing it for those structured as C corporations.

Tips, overtime, and business deductions are only a few of the conformity issues that face states. States are also considering decoupling from the federal expansion of Section 529 education savings plans for private elementary and secondary schools, from the federal “QSBS” and Opportunity Zone exemptions for wealthy investors, from certain write-offs for multinational companies, and from other measures.

Conformity debates have dragged on in some states. Conformity legislation that passed the South Carolina House was rejected by the state Senate in favor of even larger and more regressive tax cuts. The District of Columbia passed legislation to decouple, and then the U.S. Congress voted to override the District’s law, although District officials contend Congress failed to act within the requisite window of time. Wisconsin’s governor and legislative leadership had reached agreement on a budget deal that would have included conformity, but the budget deal has not yet passed as of late June.

Eventually the dust will settle. But conformity debates will return to many states in 2029 if not sooner. That’s when some provisions in the Trump bill begin expiring, likely prompting a new wave of conformity or decoupling decisions in the states.