Key Findings

Trump-Republican tax policy in the first year of the president’s second term will:

- Increase taxes paid by middle-income Americans by an average of $900 in 2026

- Cut taxes for the wealthiest 1 percent by a trillion dollars over the next 10 years

- Result in large profitable corporations paying little or no corporate income tax

- Cut taxes for foreign shareholders in U.S. businesses by $32 billion in 2026

The first year of President Trump’s second term has brought major changes in U.S. tax policy. The president, in concert with Congress, has dramatically increased tariff taxes, enacted large tax cuts that primarily benefit the well-off and corporations, dramatically curtailed IRS enforcement, and issued legally problematic regulations.

These changes have had significant impacts on taxpayers.

In 2026, middle-income Americans will see their taxes go up by an average of $900 relative to what they would have paid had the tax policies that existed at the beginning of 2025 simply continued.

The wealthy, on the other hand, will see substantial tax cuts. Over the next 10 years the wealthiest 1 percent are slated to pay at least a trillion dollars less in taxes than they would have if Congress and the President had done nothing.

The direct effect on corporations has also been substantial as more and more companies are paying little or nothing in federal corporate income tax.

The largess has not been limited to the American wealthy and corporations: foreign owners of U.S. businesses will save $32 billion in taxes in 2026.

These tax cuts have come at a substantial price. The legislated tax reductions passed by Congress and signed by the president in the One Big Beautiful Bill Act (OBBBA) are forecast to add $4.6 trillion to the federal government’s debt over the coming decade. In the same bill, to whittle down that price tag, net spending cuts amount to a $1.2 trillion reduction, with the lion’s share coming from health care.

While much of what has happened under President Trump has been done by duly elected officials, acting within legal bounds, the administration has shown little deference to the rule of law as it has imposed illegal tariffs, illegally implemented regulations, and gutted IRS enforcement initiatives.

Tax Increases for Typical Americans

The biggest change in tax policy affecting most Americans in 2026 is President Trump’s tariff taxes. Although the Supreme Court found many of his initial round of tariffs to be illegal, the administration is quickly finding alternative ways to reimpose them. The tariff taxes in 2026 will likely end up of at least the same magnitude as the ones in effect at the end of 2025.

The other tax policy changes that directly affected typical American taxpayers were a set of choices by Congress.

Without Congressional action, several tax provisions were set to expire at the end of 2025. Most of them were from the tax bill passed in the first Trump administration. One measure, a tax credit to help Americans defray some of the cost of health insurance coverage, was passed during the Biden administration. In both cases the authors of the provisions intended the measures to be continuing. They were passed as temporary measures primarily to minimize the ostensible 10-year costs to comply with Congressional budget rules.

In OBBBA, Congress largely extended the earlier Trump tax bill provisions while it allowed the termination of the Biden health tax credit. In addition to the choices Congress and the President made regarding which expiring provisions to extend and which not to extend, OBBBA added new tax breaks. These new tax breaks included corporate tax cuts and partial exemptions of tips and overtime income.

When added together, all these tax changes result in a tax increase for most Americans. The middle 60 percent of Americans will pay $900 more, on average, compared to what they would have paid if Trump had not increased tariffs and Congress had ensured that the tax policy in effect for 2025, prior to OBBBA, had been left in place. Table 1 shows the average tax increase for the middle 60 percent for each state and the District of Columbia.

Increase in Income Inequality

The 2025 tax policy changes under President Trump and Congress will increase income inequality in 2026.

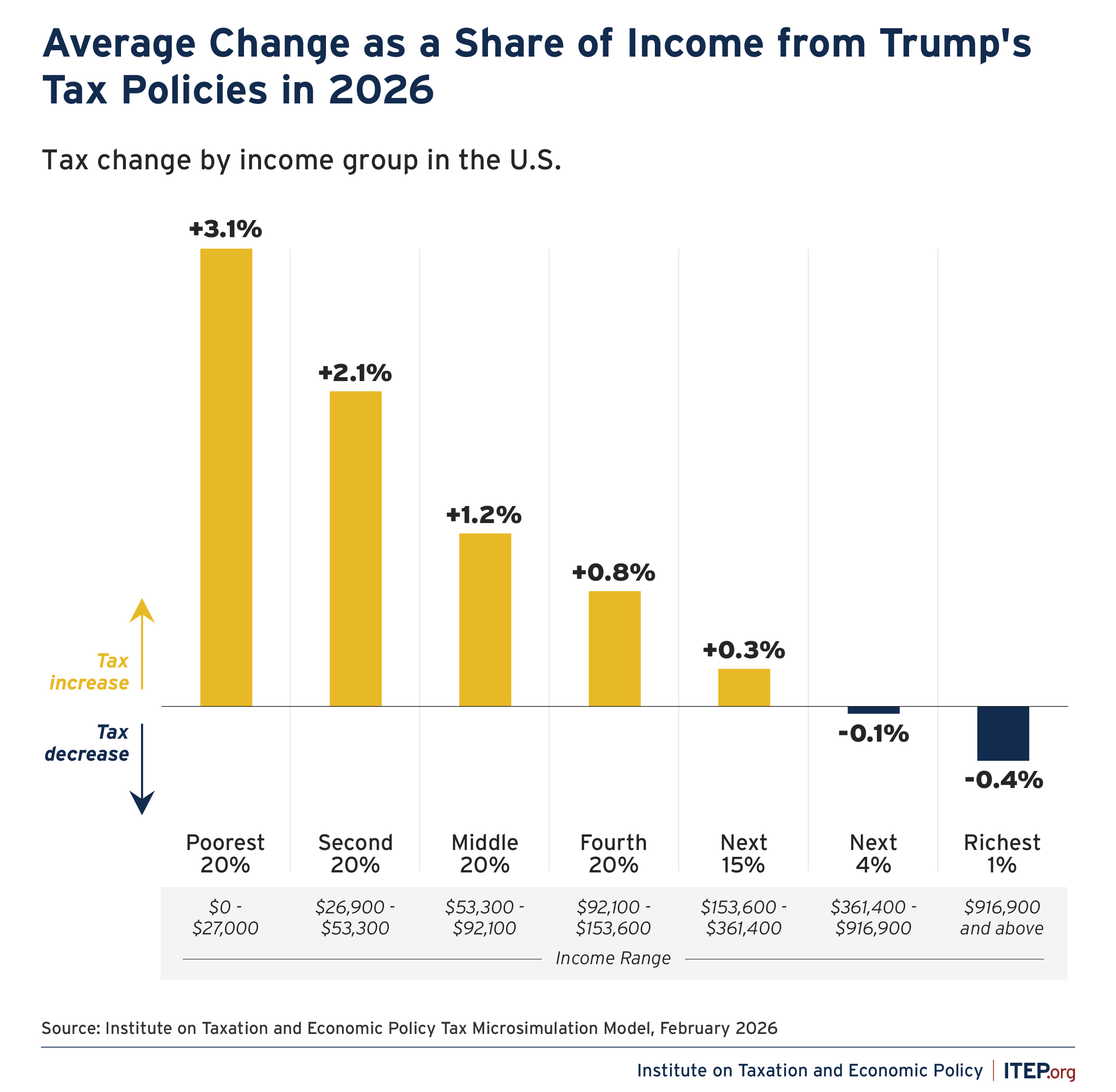

The actions and inaction described in the previous section will cause taxes overall to go up on average for those in the lower income 95 percent of the population. For the top 5 percent, however, taxes will go down on average. Although tariffs do affect higher-income Americans, they claim a smaller share of their income. The OBBBA tax cuts favoring investors are much larger for high-income taxpayers than their added tariff bill. The net impact across all incomes can be seen in Figure 2. The top 1 percent sees a net tax cut equal to 0.4 percent of their income, the middle 20 percent sees an increase equal to 1.2 percent of their income, and the poorest 20 percent sees a tax hike equal to 3.1 percent of their income.

Figure 2

More detail and national and state-by-state tables can be found here.

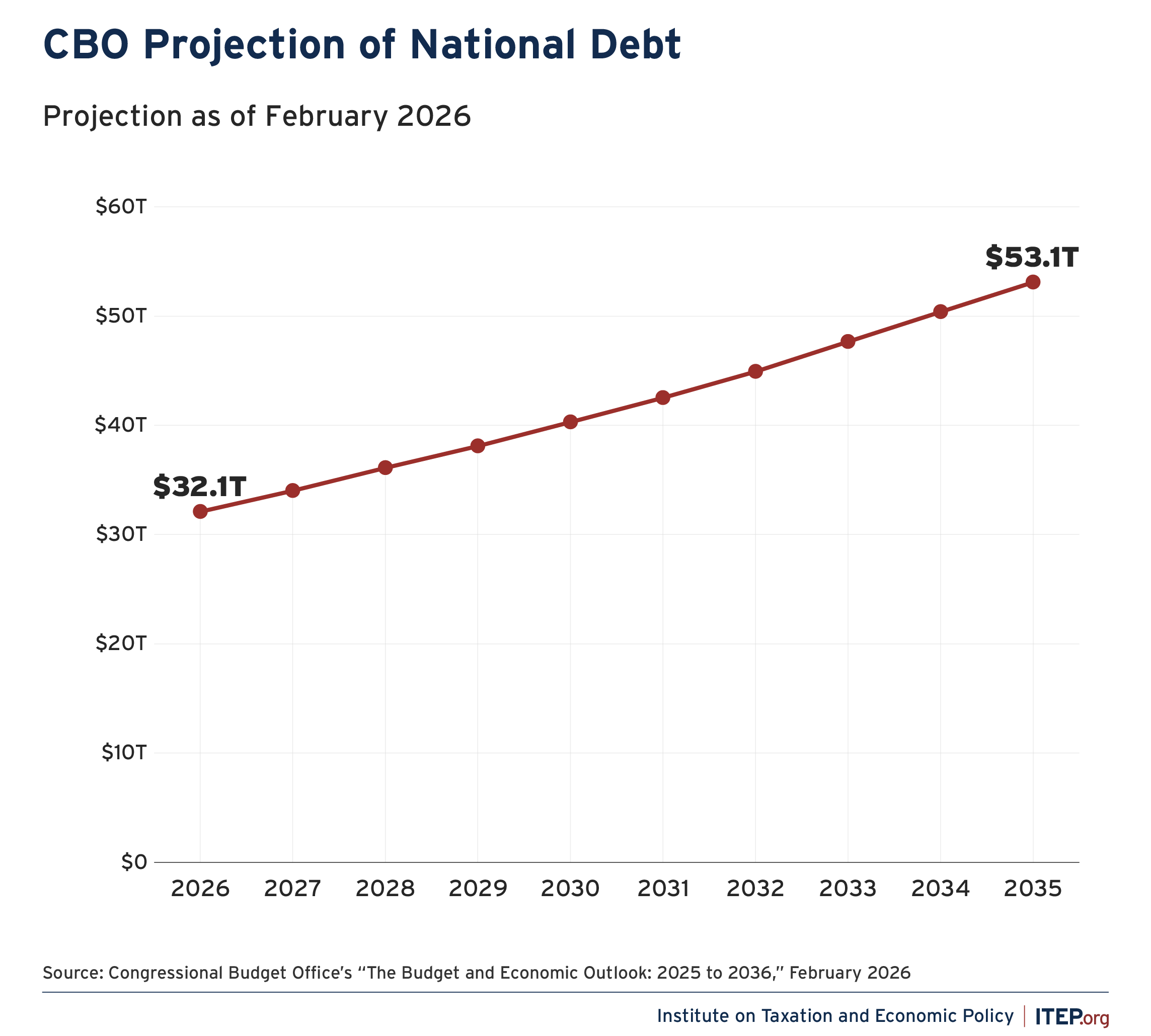

Big Tax Cuts Fuel Growing National Debt

When official budget scorers project budget deficits and the national debt, they assume that law will remain unchanged. That means that they assume that tax provisions that are set to expire will actually expire—even if that doesn’t reflect the genuine intent of policymakers or political reality. As a result of OBBBA’s extension of expiring tax provisions and additional tax cuts, official estimates of future deficits and debt are substantially higher. As of February 2026, the Congressional Budget Office projects federal budget deficits to be a cumulative $22 trillion in the 10 years from 2025 through 2034. The OBBBA tax cuts are responsible for $4.6 trillion of that.1

There is much debate as to the level of debt which the country can accrue before there are significant economic problems. Some things are, however, not in serious dispute.

First, whether we know the exact level or not, there is a point at which the debt starts to cause significant economic problems, whether that is in the form of rising interest rates, high inflation, or other consequences.

Second, the higher the debt, the more debt service eats away at other priorities. In 2026, interest on the debt is slated to be 14 percent of federal spending, rising to 18 percent by 2035. The trillion dollars of interest projected for 2026 is more than the projected spending on defense, Medicaid, and almost every other individual government agency or program.

Third, the country has looming spending obligations that will be harder to manage with higher debt. Social Security and Medicare are the most widely noted but there are many other unmet needs and areas of rising costs.

In short, this was not the time to add $4.6 trillion in debt by cutting taxes for people and companies that don’t need it.

Figure 3

Tax Contributions by the Wealthy Plummet

In 2026 the highest income 20 percent get a $380 billion tax cut with $117 billion going to the richest 1 percent alone. The tax cuts for the top 1 percent over the next 10 years add up to a trillion dollars. To put the $117 billion going to the top 1 percent in 2026 in perspective, it is more than the federal government will spend in 2026 on the combined budgets of the Department of Education, Department of Transportation, Department of Justice, the State Department, the National Aeronautics and Space Administration, the Environmental Protection Agency, the National Endowment for the Humanities, and the National Endowment for the Arts.

Or, put in another context, that $117 billion could buy every Major League Baseball team (all of them together) or pay for the combined cost of every wedding in the country for a year, as we described in July along with other comparisons.

In addition to the hundreds of billions in tax cuts from OBBBA, the wealthiest have also saved many billions with the elimination of more than $40 billion over 10 years in IRS tax enforcement funding that was aimed specifically at cracking down on tax evasion by the wealthy. The Trump administration has also, administratively, strangled IRS enforcement initiatives targeted at high-wealth tax sheltering.

More Corporations are Paying Little or Nothing in Taxes

OBBBA included large tax cuts for corporations, and the administration has added on to the benefits of these tax cuts with legally doubtful regulatory changes. Many of the corporate income tax cuts in OBBBA are retroactive, reducing companies’ 2025 tax bills and resulting in more and more corporations disclosing that they had very low income tax liability, or none at all, for the year.

For example, Amazon paid just 1.4 percent of its $89 billion in U.S. profits in federal corporate income tax while Meta paid 3.6 percent on $2.8 billion in profits and Tesla and Palantir paid nothing on their combined $7.2 billion. Table 3 shows a list of prominent companies that have, as of April 1, made their annual disclosures.

These companies’ ultra-low tax bills are just the tip of the iceberg of what has been done to business taxes in the first year of President Trump’s second term. From OBBBA alone, corporations and other businesses will pay $234 billion less in 2026 and $1.7 trillion less over 10 years.

Foreign Investors Get Big Tax Cuts Too

With the extensive foreign ownership of companies doing business in the U.S., foreign shareholders are significant beneficiaries of the corporate tax cuts under OBBBA. A total of $32 billion in tax savings from OBBBA will go offshore in 2026. Many foreign shareholders are likely to end up paying zero U.S. corporate tax despite benefiting from the U.S. economy and the role of the government in sustaining it.

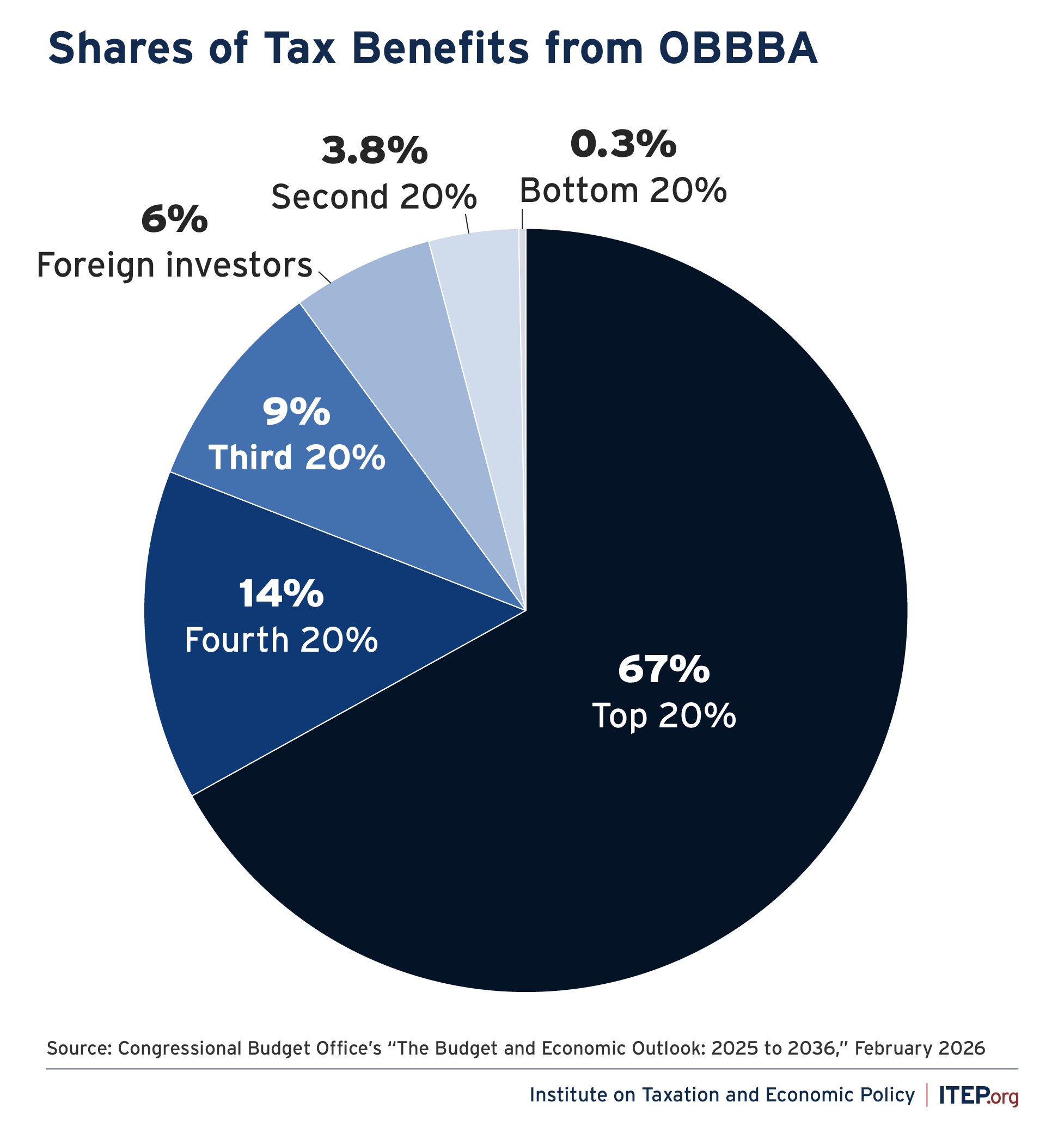

As Figure 6 shows, foreign investors get a larger share (6 percent) of the OBBBA tax cut than the lowest income 40 percent of the American population (4.1 percent). Not living here, of course, they also do not pay the tariffs that Americans are paying. The highest income 20 percent of the U.S. population, plus foreign owners/shareholders of U.S. businesses, garner 73 percent of the total tax reductions of OBBBA.

Figure 6

The Rule of Law Has Been Undermined

The Trump administration’s initial tariffs were ruled illegal by the Supreme Court. The tariffs that have initially replaced them are also illegal.

The Trump administration has also issued regulations that have significantly cut taxes for corporations. These too were done without a proper legal basis. Unlike with tariffs and other illegal administration activity, the courts may not block lawless regulations that reduce taxes. Some case law suggests that federal courts may deny “standing,” the right to sue, to anyone who isn’t affected in a very concrete, negative way, by an illegal regulation. Regulations that cut taxes may not negatively affect anyone sufficiently directly for the courts to grant standing.

The administration also put taxpayer privacy at risk with its IRS-ICE arrangement.

Finally, when the administration isn’t itself violating the law, it is making it easier for others to do so. The drastic cuts to IRS enforcement encourage the spread of lawlessness from within the Trump administration to the taxpaying public. Those who can afford to engage in complicated, hard to detect tax evasion schemes are well-positioned to evade taxes more than ever.

Conclusion

The Trump-Republican tax policies of the first year of President Trump’s second term have adversely affected most Americans while benefiting the wealthy and foreign shareholders. This has been accomplished through a mix of legislative action and illegal executive actions by the administration.

Unfortunately, it could get worse. The administration is being heavily lobbied to add to its unlawful regulatory record by indexing capital gains for inflation—which would be a benefit hugely skewed to the wealthy. In addition, the congressional Republican Study Committee has a tax plan that would, likewise, be of substantial benefit to those with the highest income and wealth.

Methodology

The methodologies for the numbers in this report can be found in the methodologies in the hyperlinked reports where they were initially published. Income tax analysis is conducted using the ITEP Microsimulation Tax Model. The tariff calculations use the consumption tax module of the ITEP model calibrated to forecasts and analysis by the Congressional Budget Office, UBS bank and a paper by Cavallo, Llamas and Vazquez on the 2025 tariffs. Tariffs are distributed by consumption, residential investment, shares of rising costs for state and local governments and business ownership—reflecting the direct effects on prices of consumer goods, the impact on costs associated with residential property ownership, the higher prices faced by state and local governments and the reduction in profits in the cases where businesses do not pass through the full amount of the tariffs to their customers.

Endnotes

- 1. OBBBA also included spending cuts and spending increases. These net $1.2 trillion, so the net increase in deficits from OBBBA is $3.4 trillion.