The ITEP Guide to State & Local Taxes

Tax Guide

ITEP's Tax Guide Research Priorities

How Do Real Property Taxes Work?

Property taxes on land and buildings are the oldest and still the largest major revenue source for state and local governments. They fund schools, health care, public safety, and other services. They are collected mostly by cities, counties, school districts, and other types of local government, but states typically make the rules for assessing the value of property and imposing the tax, with major implications for tax fairness and adequacy.

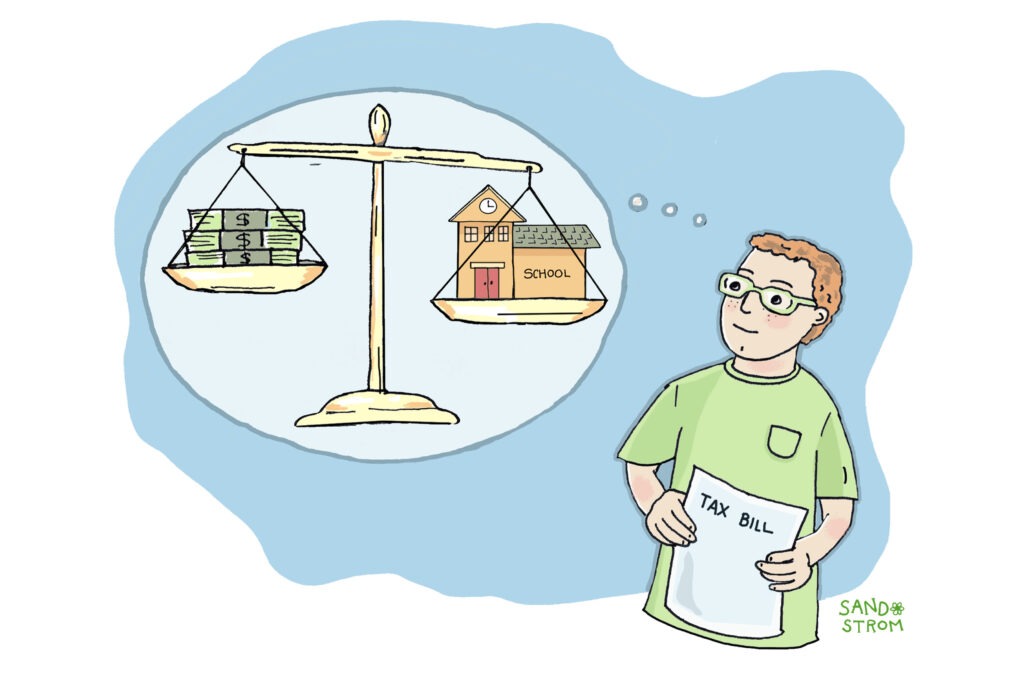

How Do Personal Income Taxes Work?

The personal income tax funds public education, health care, public safety, and other public services provided by state and local governments. If well-designed, it is the fairest major revenue source available to states.

What Principles Should Guide State and Local Tax Policy?

ITEP explains the five core principles of sound state and local tax policy: adequacy, fairness, neutrality, simplicity, and accountability.

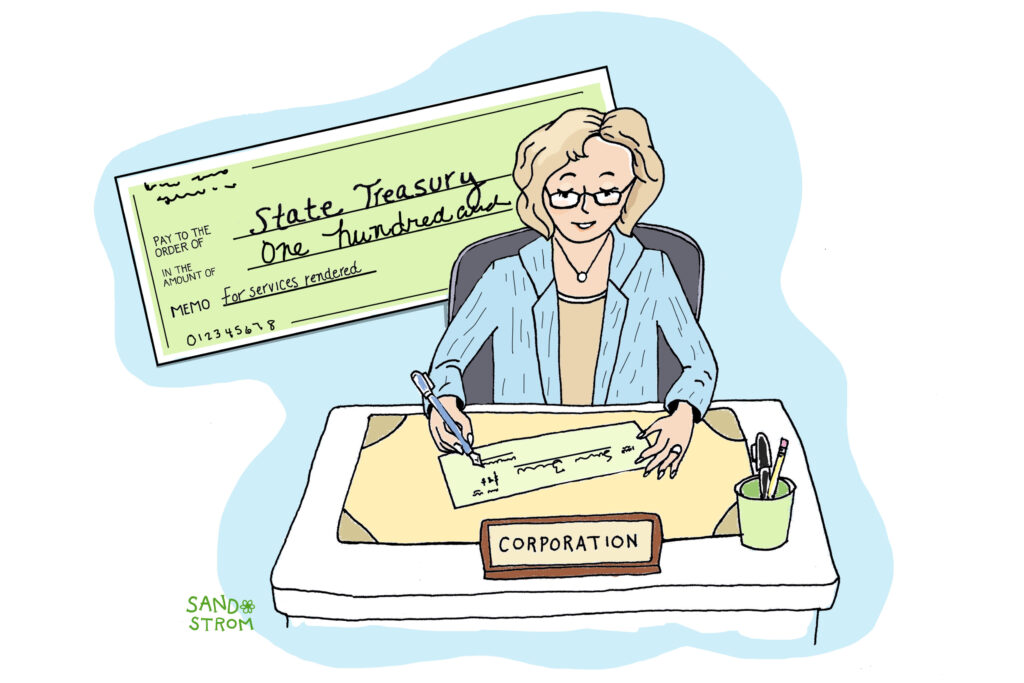

How Do State Corporate Income Taxes Work?

State corporate income taxes apply to C-corporation profits earned in each state. Learn how nexus, apportionment, combined reporting, and tax rates work.

How Do State and Local Tax Systems Affect Racial Justice?

State and local tax codes can narrow or widen racial inequality. Progressive tax policies reduce the racial wealth gap; regressive ones make it worse.

Do Tax Cuts Fuel Growth?

Tax cuts do not reliably fuel economic growth. State and local taxes represent around 2–4% of business costs, and evidence shows public investment in education, infrastructure, and services drives growth more effectively than tax reductions.

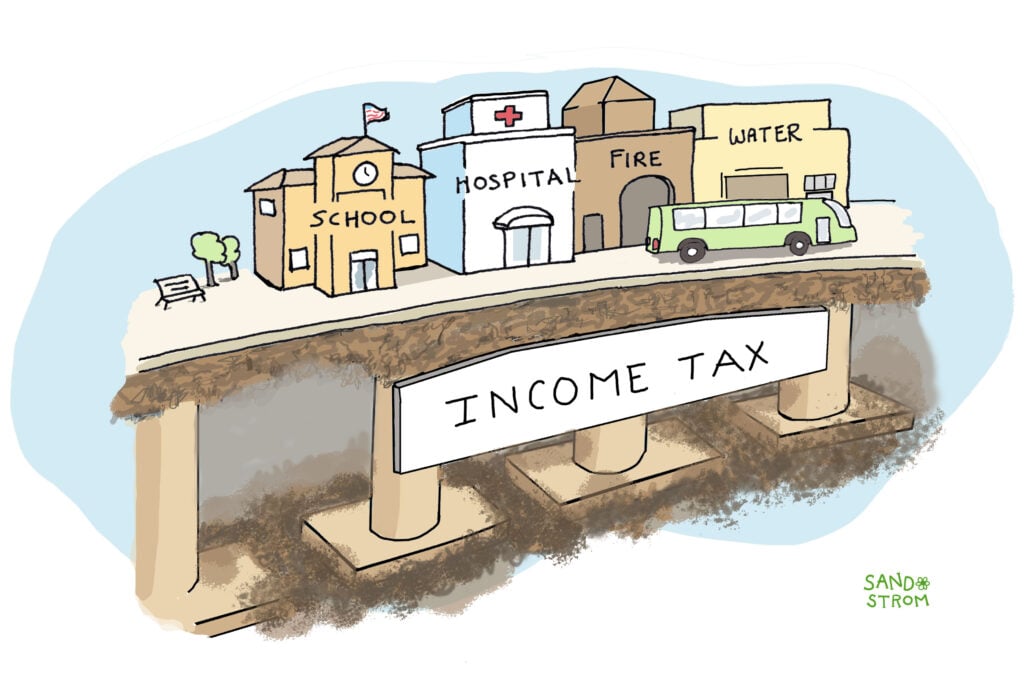

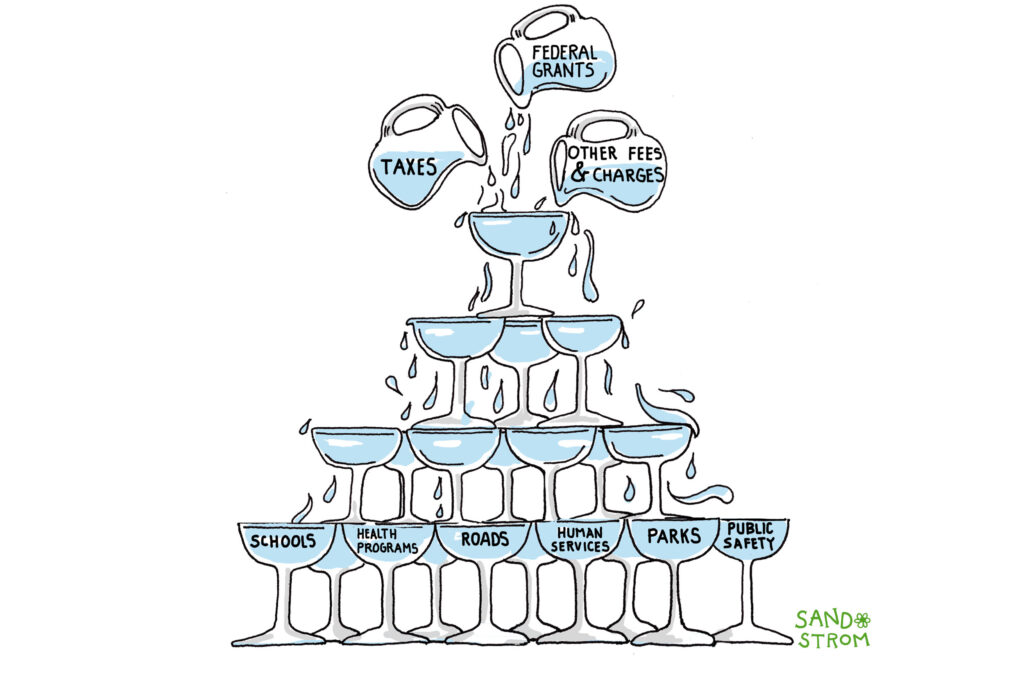

How Do State and Local Governments Raise Funds?

State and local governments play important roles in helping communities thrive. They fund and run schools, roads, parks, health programs, human services, public safety agencies, and other key services. To pay for these services, states and local areas receive money from multiple sources. The main source is taxes, but funds from the federal government and fees people pay to use services are also important contributors.

What Are Tax Bases and Tax Rates?

Taxes equal rate × base. Broader bases allow lower rates. Learn the difference between nominal and effective tax rates in this guide from ITEP.

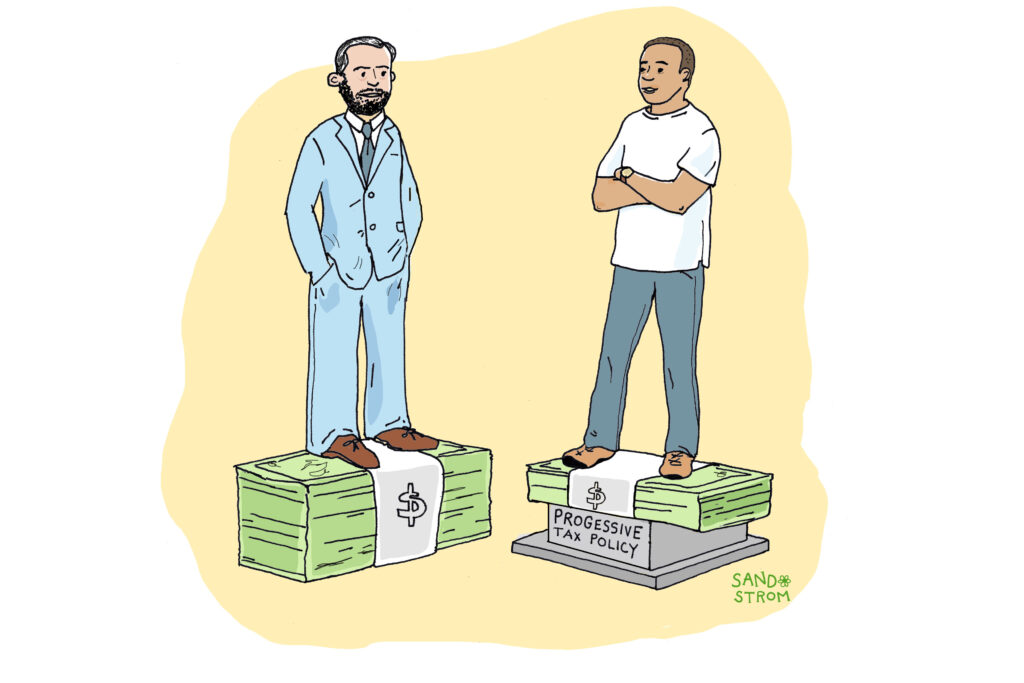

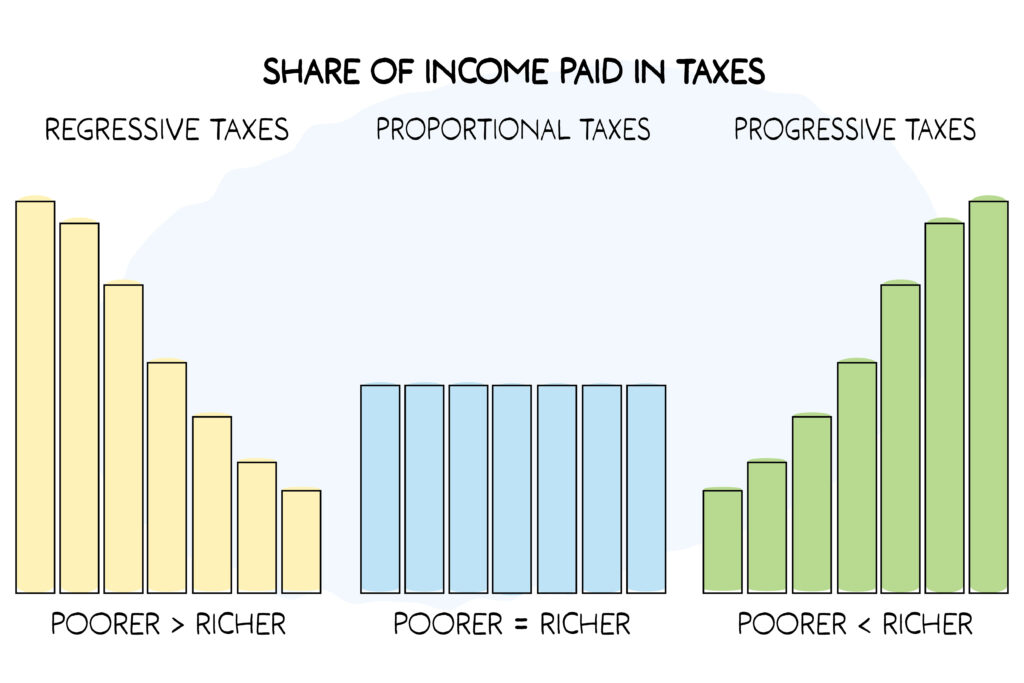

Why Should States and Localities Have Progressive Tax Systems?

Learn why progressive state and local tax systems raise more revenue, reduce poverty, and advance racial equity — and why nearly every state's current tax code falls short.

How Does Federal-State Tax Conformity Work?

Learn how states link to the federal tax code via rolling, fixed-date, or selective conformity — and when they decouple. Includes a 50-state reference table.

What Are Local Governments’ Taxing Authorities?

Tens of thousands of local governments in the United States, from big cities like Los Angeles and New York to rural counties, school districts, and small towns, operate schools, roads, parks, public safety, and other services. To pay for it, they collect roughly $1 trillion in taxes annually and receive another $800 billion in grants from states. But states, not just localities, set many of the rules for local taxes, and sometimes use that authority to undermine local democracy.

How Do State Tax and Expenditure Limits Work?

A Tax and Expenditure Limit (TEL) is a formula written into state law or into a state constitution that constrains government revenue and spending. These measures can undermine governmental accountability, degrade essential public services like health care and education, and create inequitable tax burdens.

Why Does Tax Incidence Matter and How Do We Measure It?

Tax incidence shows who pays taxes and how much they pay. In studying tax fairness, tax incidence specifically looks at how much people at different income levels pay. Tax incidence analysis is a critical tool for assessing the fairness of tax systems and in showing the equity or inequity of tax policy proposals.

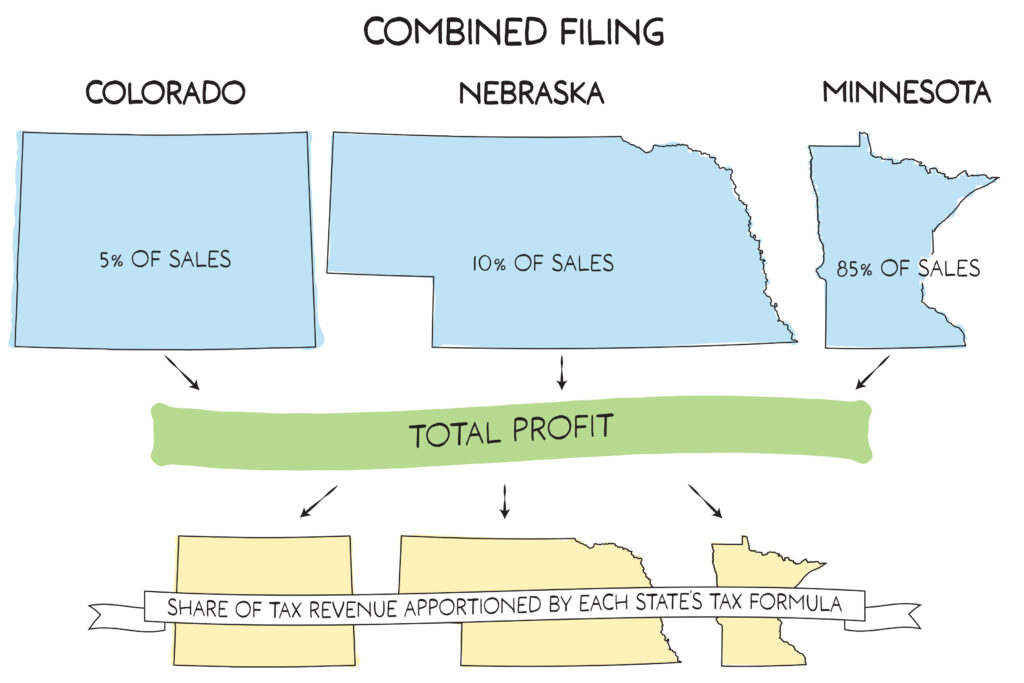

How Do States Use Combined Reporting to Tax Complex Multi-State Corporations?

Combined reporting requires corporations with multistate operations to report all their revenues and expenses together, making it harder for them to avoid state taxes by moving money around. This policy mainly affects very large companies, and it helps those states that use it to collect billions in tax revenue to fund services like education, public safety, and infrastructure that businesses and their employees rely on.

What State and Local Taxes Do Undocumented Immigrants Pay?

Like everyone else in America, immigrants pay taxes, whatever their legal status. The income taxes, property taxes, and sales and excise taxes paid by both documented and undocumented immigrants help sustain American public schools, services, and infrastructure. Undocumented immigrants paid more than $37 billion to states and localities in 2022, and they pay higher effective state and local tax rates as a share of their incomes than our wealthiest citizens.

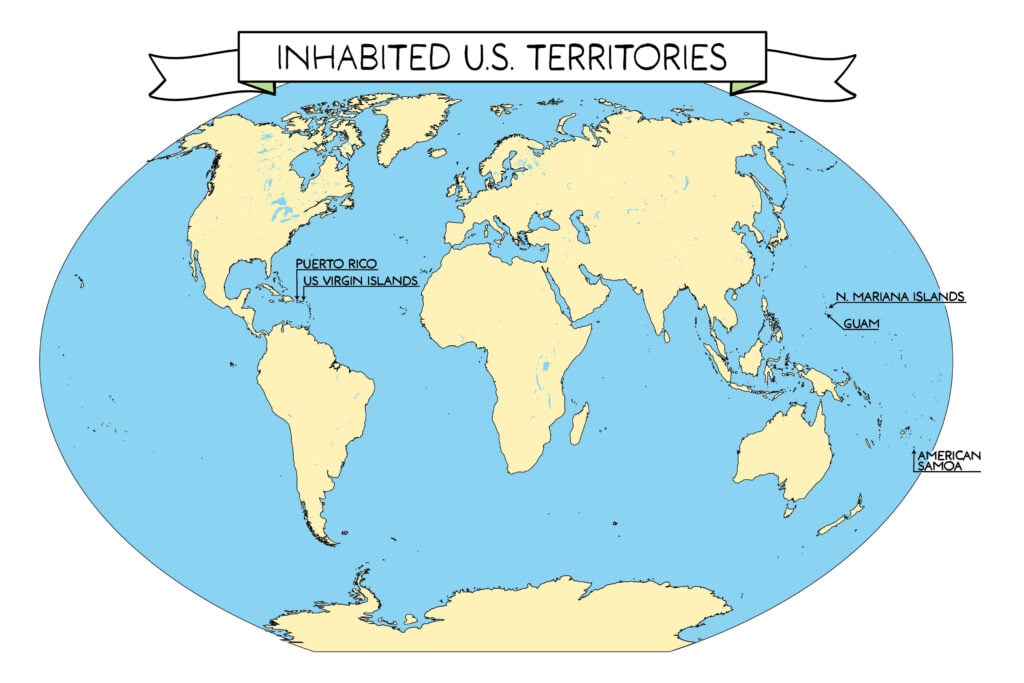

What Taxes Are Paid in Puerto Rico and Other U.S. Territories?

U.S. territories collect taxes to fund schools, roads, health care, and other services, somewhat like states do. They levy income taxes, sales taxes, property taxes, and other typical state and local taxes. These taxes can have important progressive elements, but territorial status poses unique challenges for fair and adequate taxation.

How Do State Itemized Deductions Work?

Most states that collect income taxes allow taxpayers to claim itemized deductions, which are tax breaks for items such as charitable donations, mortgage interest, medical expenses, and property taxes. These deductions reduce revenues that could otherwise be used for services like schools and health care, and they mostly benefit wealthy families. Because they are so skewed and ineffective, many states either limit itemized deductions or forgo them altogether.

How Do Legal Fines and Fees Work?

State and local governments collect billions each year from legal fines and fees tied to criminal justice and regulatory violations. Learn how fines and fees work, why governments rely on them, and why heavy reliance can worsen economic and racial inequality.

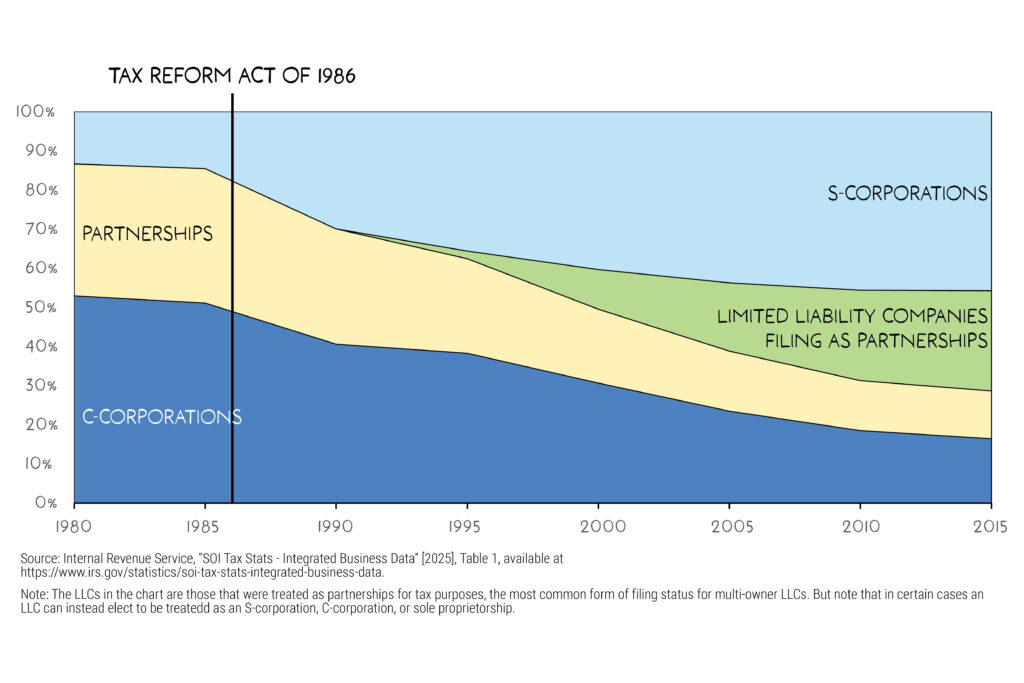

How Do States Tax the Profits of Pass-through Entities?

Learn how states tax pass-through entity profits, including S-corps, partnerships, and sole proprietorships, and why it matters for tax equity.

Tax Policy Glossary: Key State and Local Tax Terms

A glossary of key state and local tax policy terms including AGI, tax credits, nexus, pyramiding, and more. Part of the ITEP Guide to State and Local Taxes.

How Do Personal Property Taxes Work?

The great majority of property tax revenue is based on the value of land and buildings, but states also apply property taxes to certain business equipment, machinery, and supplies, and sometimes also to automobiles. Collectively these taxes are known as “personal property taxes.”

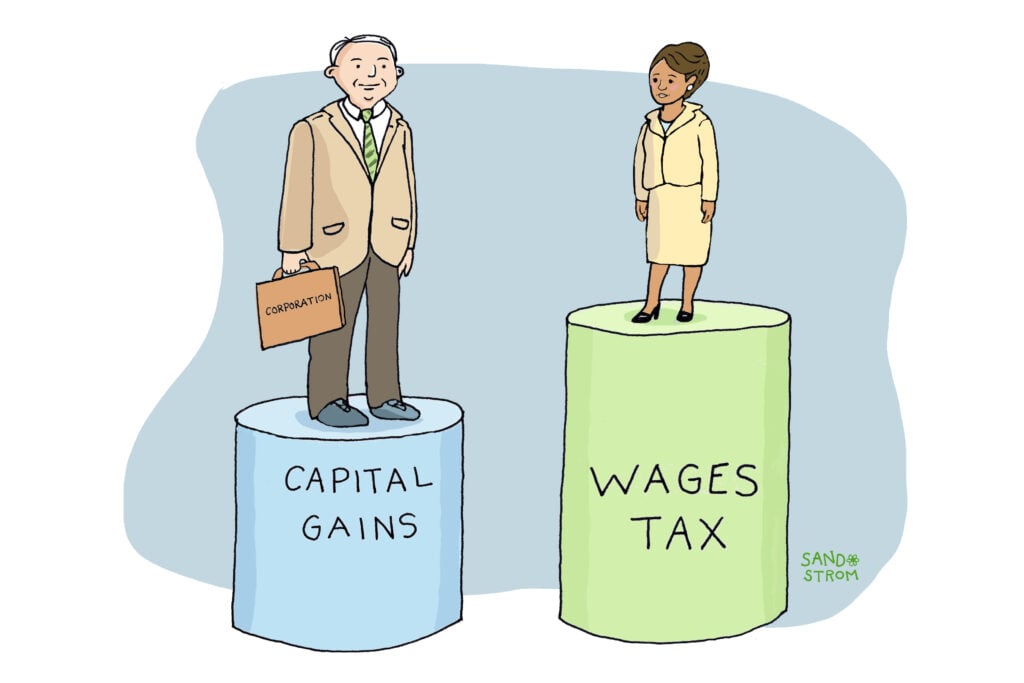

How Do States Tax Investment Income?

State personal income taxes apply not just to wages and salaries but also earnings on investments, like stocks and bonds. Most investments are held by wealthy people, so when states tax investment income at a lower rate than wages, high-income households pay tax at lower rates than middle-income households. By contrast, states that strengthen taxation of investment income can raise substantial revenue while improving economic and racial equity of their tax code.

How Do States Tax Cannabis?

States tax cannabis using sales taxes and special excise taxes based on price, weight, or potency. Learn how these taxes raise revenue and shape cannabis policy.

How Do State Tax Credits for Workers and Families Work?

State-level Earned Income Tax Credits (EITCs) and Child Tax Credits (CTCs) help workers and families make ends meet by reducing their taxes and providing refunds. Research shows these credits are very effective at reducing poverty and creating more equitable tax systems.

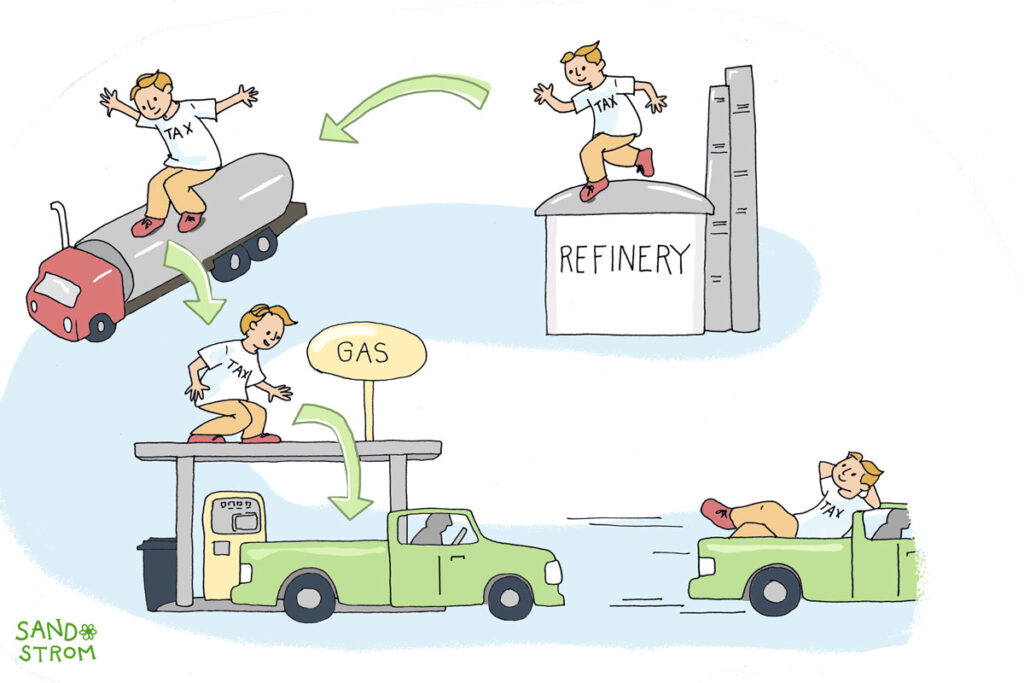

How Do State and Local Excise Taxes Work?

Excise taxes are sales taxes on specific goods such as gasoline, tobacco, and alcohol. Learn how state and local excise taxes work, why governments use them, and the policy issues they raise.

How Do State Estate and Inheritance Taxes Work?

Estate and inheritance taxes are taxes on wealth passed on after someone’s death. They are a common way for states to tax the inheritances of wealthy individuals. These taxes ensure that those very large estates help pay for public services like schools, hospitals, and parks.

How Can Communities Collect Property Taxes from Exempt Nonprofits?

Payment in Lieu of Taxes (PILT or PILOT) programs allow local governments to collect revenue from nonprofits that otherwise would not be contributing to the cost of providing local services.

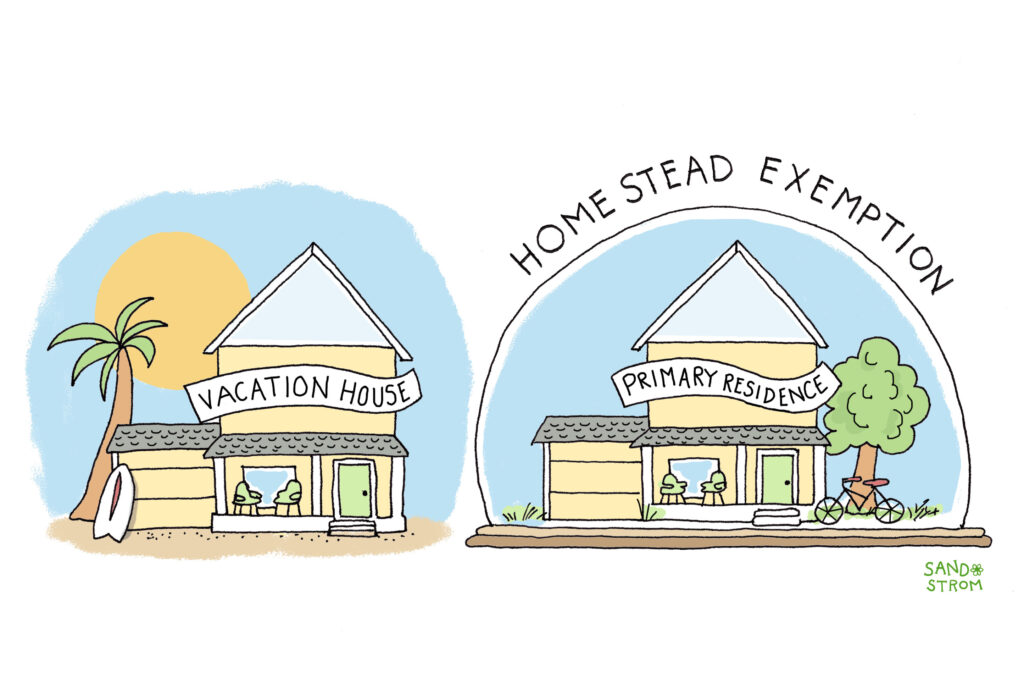

How Can Cities and States Reduce Property Taxes for Homeowners and Renters?

To reduce the cost of property taxes for homeowners and renters, many places offer homestead exemptions, circuit breakers, and deferrals. Such provisions are more cost-effective alternatives to broad tax cuts or tax limitations.

What’s Exempt from State and Local Sales Taxes?

Some purchases are exempt from state and local sales taxes. Learn which goods and services are commonly exempt, why exemptions exist, and how they affect tax fairness and revenue.

How Do State and Local Sales Taxes Work?

Sales taxes are the second largest source of revenue for state and local governments. In nearly every state they are an important way we pay for public education, health care, public safety, and other services. But they are also typically the costliest tax for low-income families.

Guide to State and Local Taxes

How do state and local taxes work? ITEP's free guide explains income taxes, property taxes, sales taxes, and other revenue sources. It is a detailed primer on state and local tax policy, explaining a wide range of tax concepts and specific levies that states and localities use to fund public services.

Institute on Taxation

and Economic Policy

ITEP is a non-profit, non-partisan tax policy organization. We conduct rigorous analyses of tax and economic proposals and provide data-driven recommendations to shape equitable and sustainable tax systems.

Subscribe to ITEP Emails

Tax research and policy news in your inbox.

Promote Fair Tax Policy

Your gift to ITEP promotes tax justice. With your help, we do research that supports taxing millionaires and billionaires, taxing big corporations and raising revenue for the things our people, our communities and our planet need.

Together, we can create a country with more economic justice, more racial justice, more climate justice… and more tax justice.