The 2025 Trump tax law slightly increased the Child Tax Credit in a way that benefits virtually none of the children who most need help.

Last year’s tax law, the so-called “One Big Beautiful Bill Act” (OBBBA), includes among its many provisions a small increase to the Child Tax Credit (CTC), but it leaves in place many problems with the current credit – namely that it leaves out many of the poorest children from its full benefits. This and other problems with the CTC would be eliminated by a bill known as the American Family Act, which would reinstate and expand upon a version of the CTC that was in effect for one year during the pandemic.

OBBBA increases the maximum CTC for any child from $2,000 (the level it would be if Congress had simply extended the tax rules in effect in 2025) to $2,200, but leaves in place restrictions based on earnings and other income. Notably, the $2,200 credit level is lower than it would be if Congress had simply adjusted the credit for inflation in the 2017 tax law that set the amount at $2,000.

While a handful of children are ineligible for the full CTC because their families are too rich, a much larger number of children are ineligible for the full CTC because their families are too poor. This is because the part of the CTC that can otherwise benefit many low- and middle-income families (the refundable portion) is subject to restrictions that OBBBA left in place and which the American Family Act would eliminate.

This analysis of OBBBA’s Child Tax Credit provision and alternatives to it finds that:

Under the American Family Act, no children would be denied the full Child Tax Credit (CTC) because their families earn too little. Under OBBBA and the rules it leaves in place, many children are barred from receiving the full credit in 2026, including:

- 30 percent of all children in the U.S.

- Virtually all (99 percent) of children among the poorest fifth of Americans, the families who most need help.

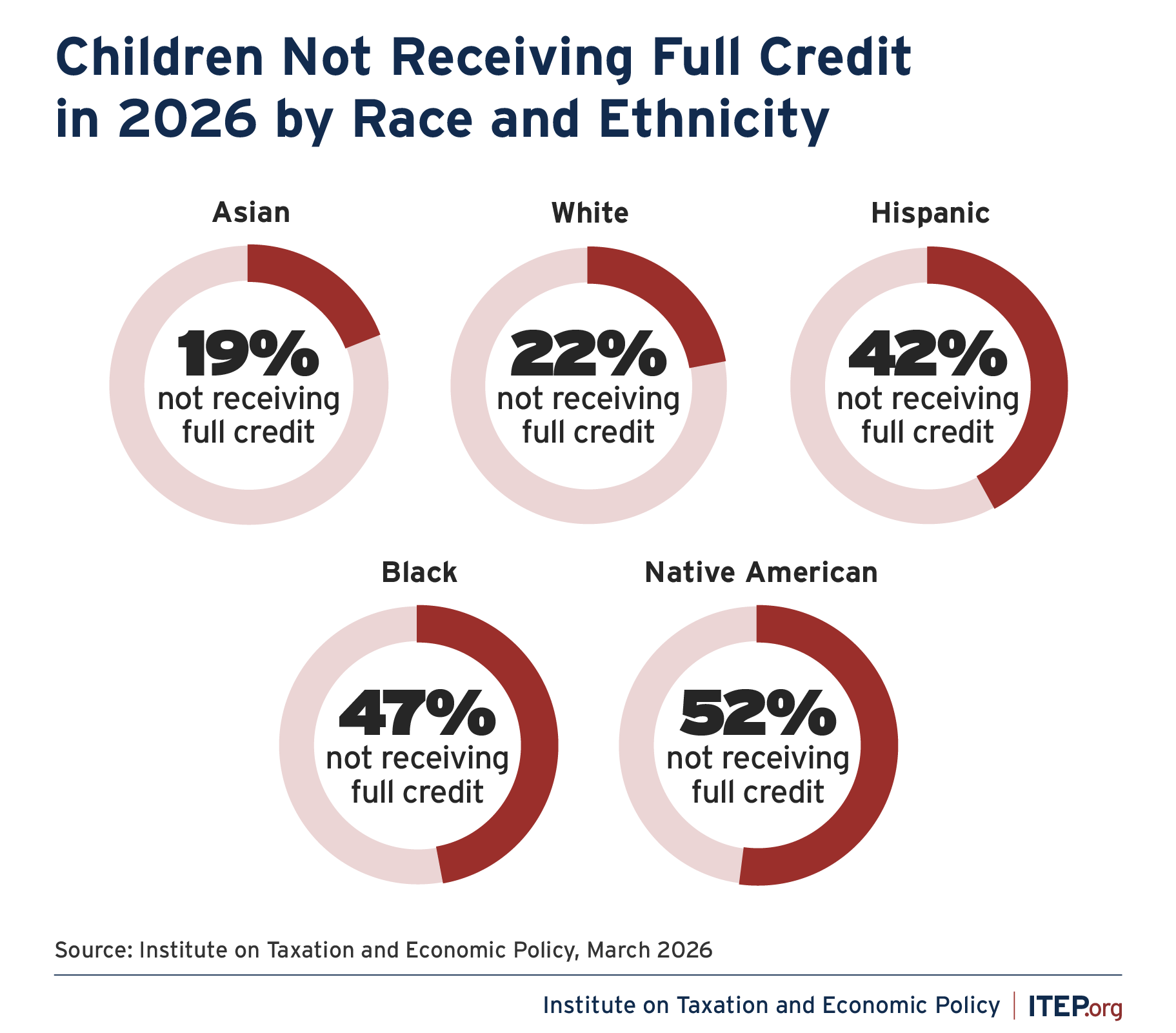

- About 40 to 50 percent of children in Black, Hispanic and Native American families

- About 22 percent of children in white families.

- A higher share of families with young children.

OBBBA’s $200 increase in the CTC is poorly targeted toward supporting working-class families because larger benefits go to families with higher incomes and smaller benefits go to those with lower incomes. The American Family Act would have the opposite result.

- The largest share of benefits from the OBBBA CTC provision (41 percent) will go to the richest fifth of Americans, declining for each income group until it drops to virtually 0 percent for the poorest fifth of Americans.

- The impact of the American Family Act would be the opposite, with the largest shares going to low- and middle-income children.

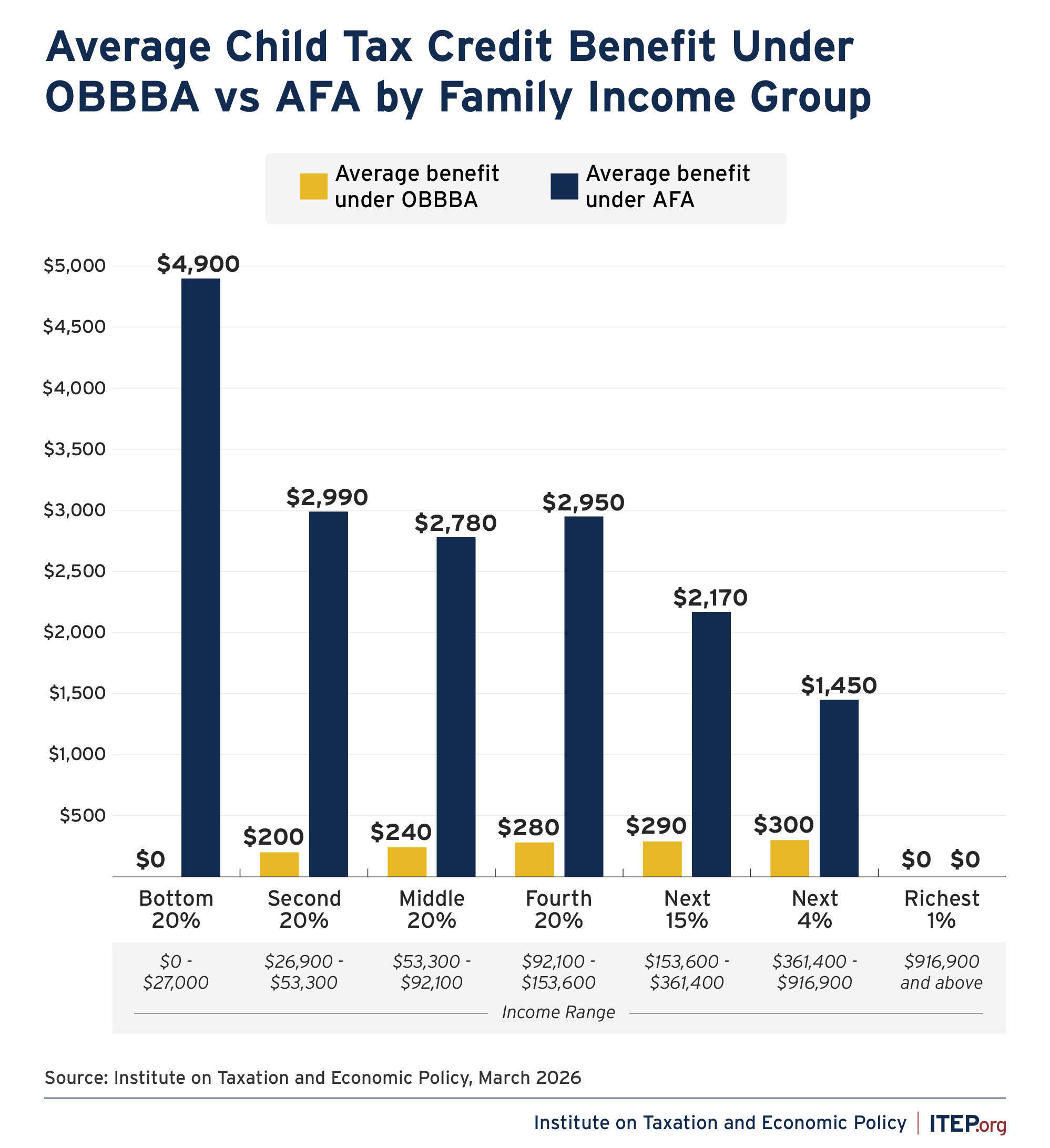

- While President Trump’s tariff policies are estimated to have raised the price of the typical family’s baby products by $400 in the first half of 2025, OBBBA’s average benefit is $0 for the poorest fifth families with children and $240 for the middle fifth of families with children.

- Under the American Family Act, the average benefit would be $4,900 for the poorest fifth of families with children and $2,780 for the middle fifth of families with children.

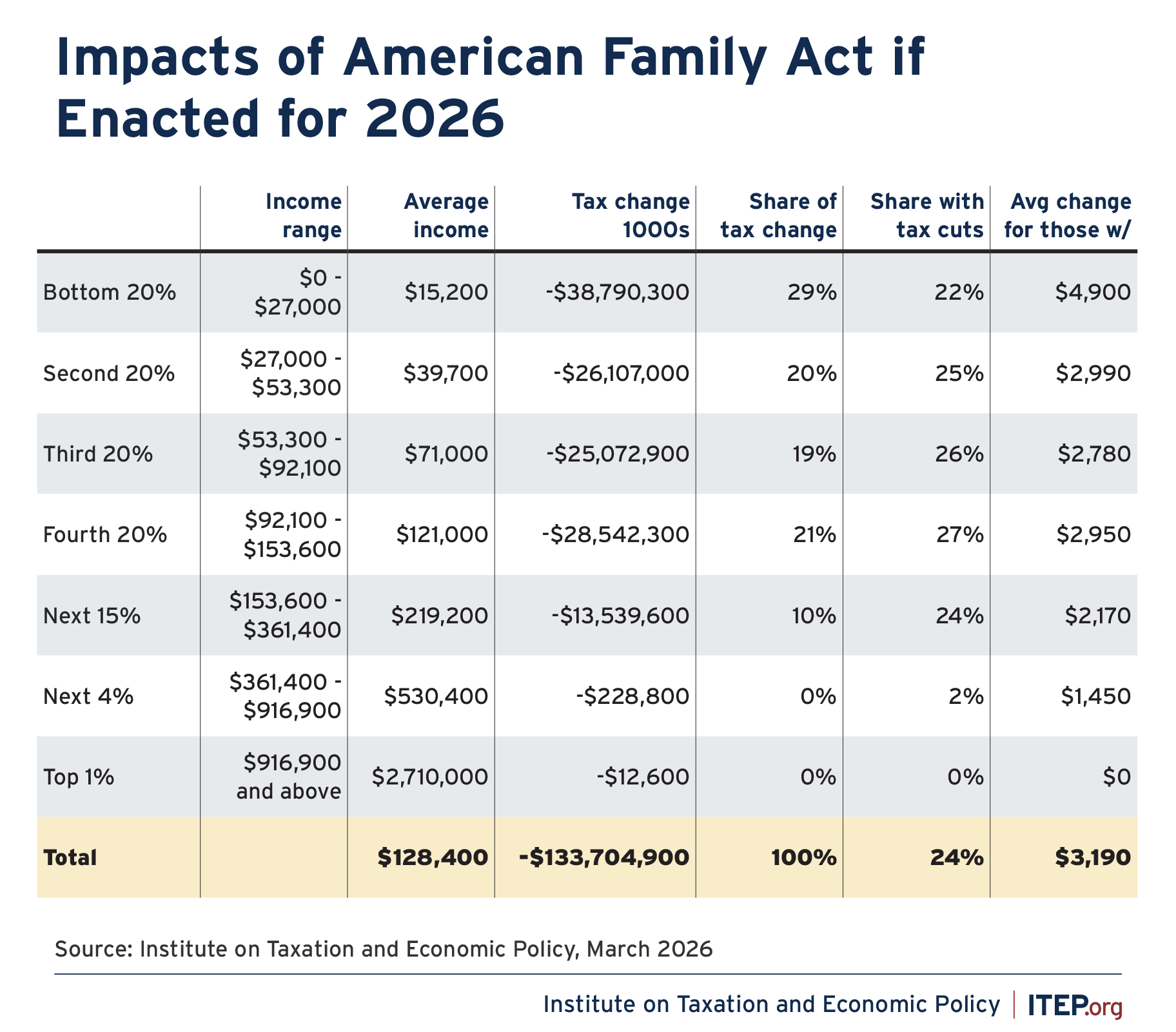

Figure 1

Even if this Congress was reluctant to enact the American Family Act because of its cost, it could have easily pursued the far cheaper CTC expansion that was included in a bipartisan bill that passed the House in 2024 and would have provided far more benefits to low- and middle-income families than OBBBA does.

The Current Child Tax Credit Leaves Out Most Children in Lower-Income Families

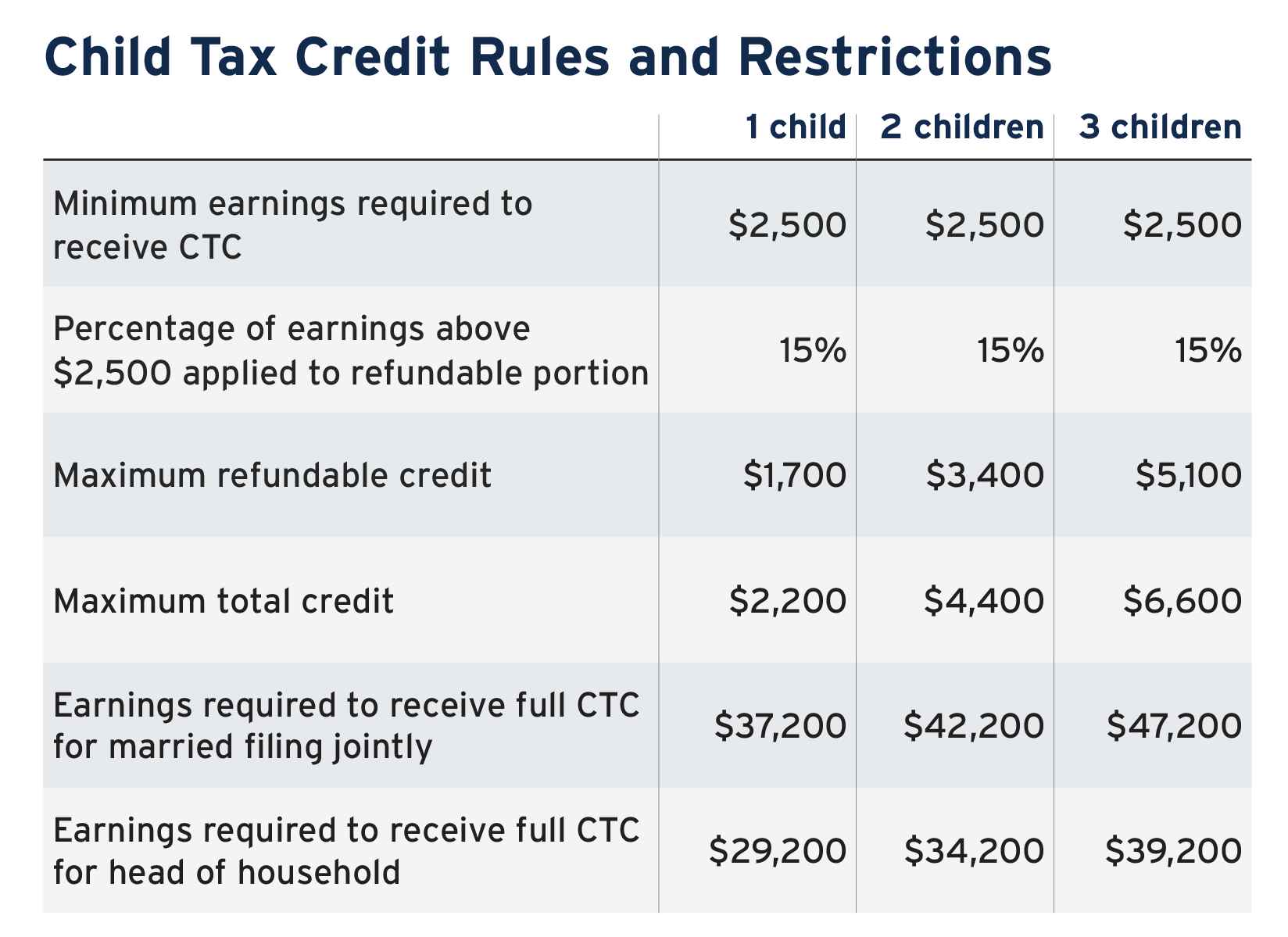

The Child Tax Credit currently contains two income restrictions that prevent poorer families from receiving the full credit amount. The credit is partitioned into two amounts, a non-refundable portion and a refundable portion. The non-refundable portion is the amount that families can use to directly offset their tax liability. The refundable portion is the amount that families can receive on top of their tax refund if they have little to no federal individual income tax liability.

Rules that restrict the refundable portion of the credit result in smaller total credits for families who have modest incomes – families who typically pay payroll taxes, excise taxes, tariffs, and many state and local taxes but do not earn enough to owe much or anything in federal income taxes.

Rules that restrict the refundable portion of the credit result in smaller total credits for families who have modest incomes – families who typically pay payroll taxes, excise taxes, tariffs, and many state and local taxes but do not earn enough to owe much or anything in federal income taxes.

The first restriction is that the refundable portion is limited to a smaller amount per child than the full credit ($1,700 versus $2,200 in 2026).

The second is that the refundable portion includes an earnings-based requirement limiting the credit to a fraction of the family’s earnings above $2,500.

To illustrate how these rules work, the maximum CTC allowed for a family with three children in 2026 is $6,600 (three times $2,200). But the refundable portion for a family with three children cannot exceed $5,100 because the cap on the refundable portion is $1,700 per child and multiplied by three, that comes to $5,100.

In practice, a family with three children will often receive even less than $5,100 because of the additional layer of restrictions based on their earnings. For example, if the family’s earnings are $30,000, then calculating the credit as 15 percent of their earnings above $2,500 would allow them just $4,125 in tax credits. This is about one-third less than the $6,600 maximum available to higher-income families.

A Larger Non-Refundable Credit Means Many Children are Still Left Out

As part of OBBBA, Congress and President Trump increased the maximum non-refundable CTC amount from $2,000 to $2,200 for 2025 and 2026, and indexed that to inflation for subsequent years. They did not, however, address the limits on the refundable portion of the credit. While this means that middle- and upper-income families with children will receive a larger CTC by a few hundred dollars on average, the lowest-income families will not see their CTC change. The richest 20 percent of Americans will receive the largest benefit from this change of any income group in 2026 while the poorest 20 percent will receive nothing.

Figure 2

The income restrictions mean that children in lower-income households are significantly more likely to be left out than those in higher-income households. Ninety-nine percent of children in the poorest fifth of households will receive a reduced credit or no credit at all. Zero percent of children in the richest fifth of households will be left out due to restrictions on refundability, though some will be denied the credit under means test rules established in 2017 because their families’ incomes are very high.

Figure 3

Differences in Effect Based on Race and Ethnicity and Youngest Child Age

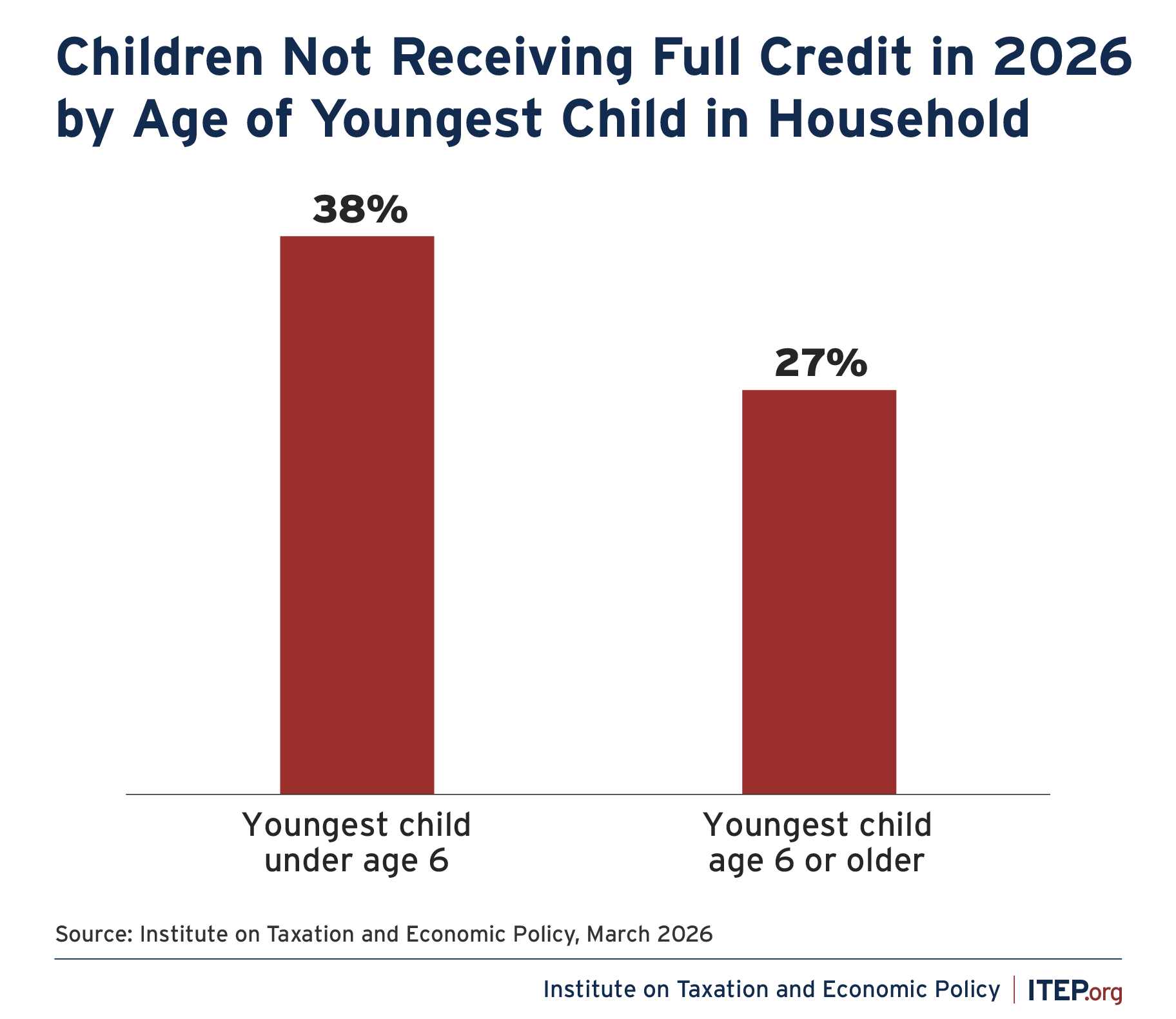

While the income restrictions leave out children of all ages and races, children with certain household characteristics are less likely to receive the full credit than others. Households with older children are more likely to receive the full credit than households with younger children. And white and Asian children are much more likely to receive the full credit than Black, Hispanic, or Native American children.

These differences are due to income disparities that persist across racial groups and child age for numerous reasons.

Figure 4

Among households where the youngest child at home is less than six years old, 38 percent of children will not receive the full CTC in 2026. This contrasts with 27 percent of children in households where the youngest child is 6 or older.

Households with younger children typically have younger parents as well, meaning the primary income earners are earlier in their careers and earning lower pay. Additionally, many parents will temporarily exit the paid workforce or reduce their hours when they have younger children at home.

This means that the current CTC is ill-targeted toward helping children during the most critical years of development. Childhood development researchers have long identified ages zero to five as the most important years for long-term outcomes.1

Alternative proposals that provide more inclusion and higher benefits for younger children have been bubbling up from the state level, where 11 of 15 state CTCs are fully refundable, and eight include some degree of tailored benefit for younger children.2

Figure 5

Due to historical factors, Black and Hispanic families, on average, have lower incomes than white and Asian families. Centuries of slavery, segregation, redlining, and exclusion from government programs that helped build wealth (such as the original GI Bill and FHA mortgages) left Black families with far less inherited wealth. The effects of these policies have persisted through generations, and the income from wealth in affected communities tends to be lower than non-affected communities. Many Hispanic families also face barriers tied to immigration and concentration in lower-paid occupations.3

Other Options for CTC Expansion Would Have Helped More Children in Lower-Income Families

While Congressional Republicans ultimately settled on a modest credit increase, there were other options available that would have helped more lower- and middle-income families.

One alternative proposal was the American Family Act, which has widespread support among Congressional Democrats in the House and Senate.4

This bill would remove all refundability restrictions for low-income families and substantially increase the maximum credit amount while adjusting it annually for inflation. While all children would be eligible for a much larger credit than under current law, the credit amount would be highest in the earliest years of a child’s life.

If this proposal had been enacted as part of OBBBA, nearly three-quarters of the benefit would have gone to families earning less than $153,600 (the bottom 80 percent by income). The average tax cut for the poorest fifth of families, those earning less than $27,000, would have been nearly $5,000. Of the three proposals examined in this report, the American Family Act would have clearly gone the furthest in addressing disparities in CTC received based on income, race, and age of youngest child. No child would be left out of the full credit due to their family having too little income.

Figure 6

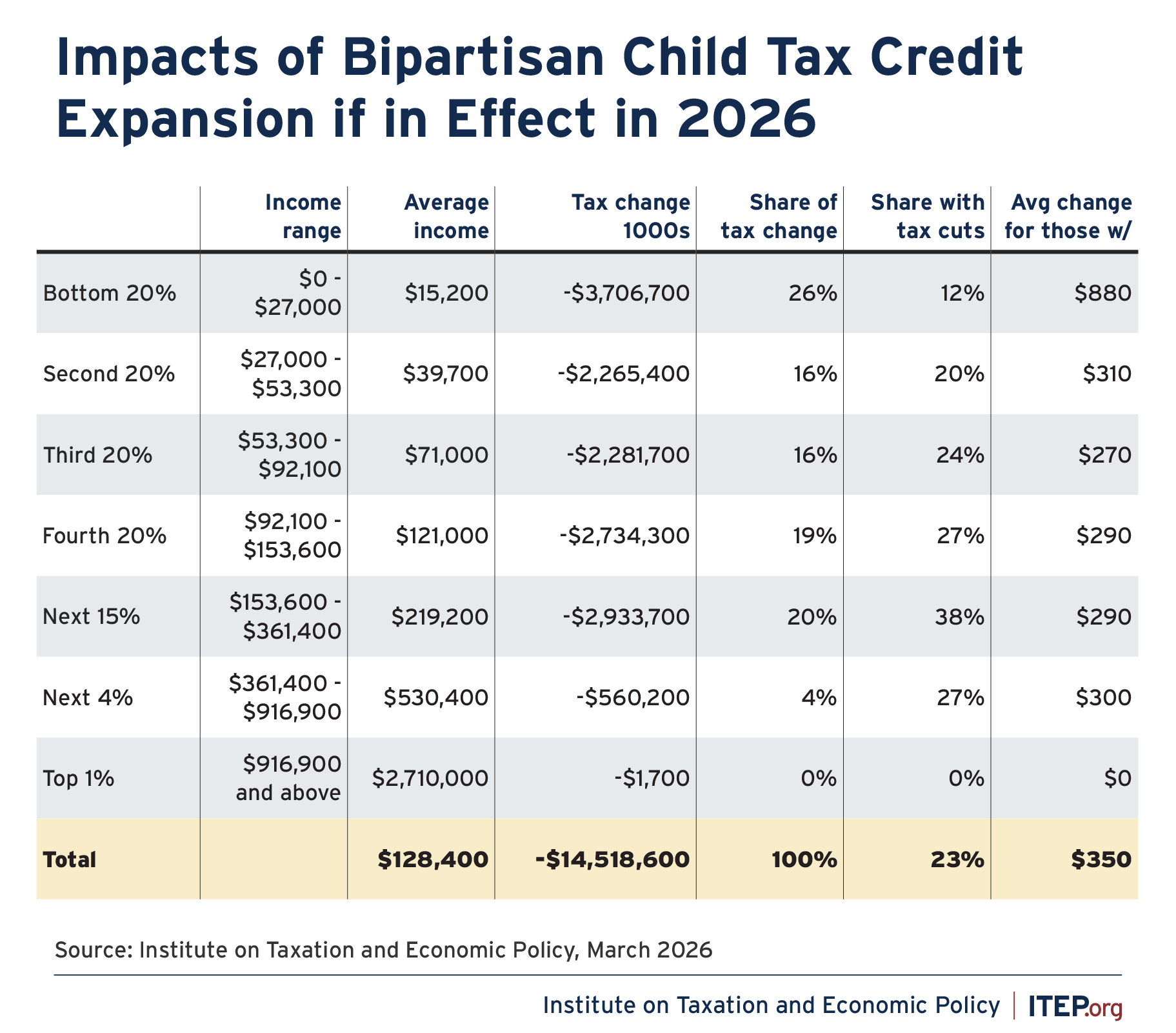

While Congressional Republicans have shown little interest in that proposal to date, House Republicans in 2024 voted overwhelmingly in favor of a bipartisan agreement to increase the maximum credit amount and relax the limits on the refundable portion of the credit.5

The Tax Relief for American Families and Workers Act, which passed the House of Representatives with broad support before failing in the Senate, would have increased the full credit amount each year for inflation. If that bill had passed then and been extended into 2026, the maximum credit would be the same $2,200 as included in OBBBA.

More importantly for working-class families, the bill would have loosened restrictions on the refundable portion of the credit, although it would not have eliminated those restrictions as the American Family Act would.67

Figure 7

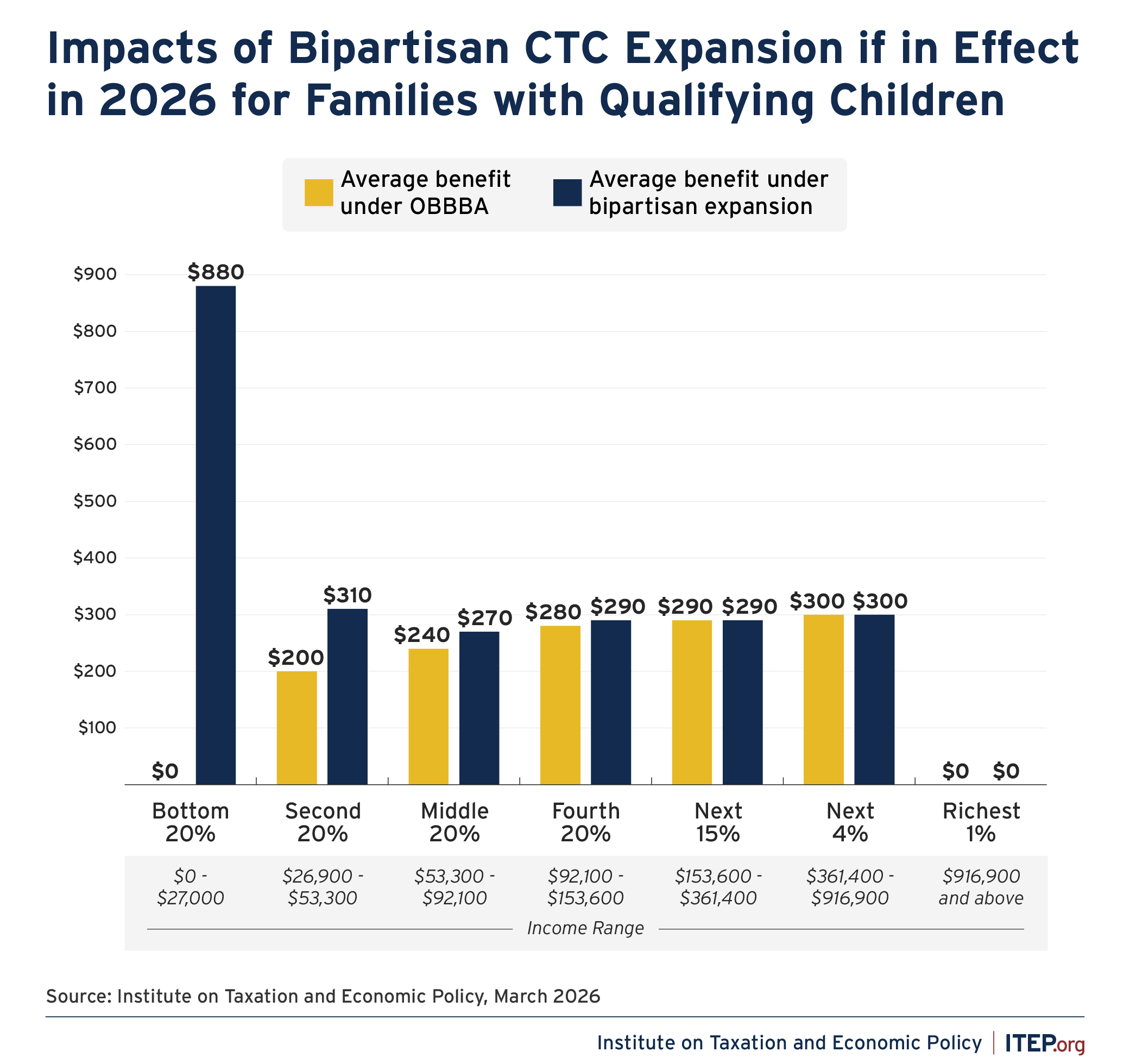

If the administration and Congress had pursued this proposal instead of the one included in OBBBA, lower- and middle-income families would have received much larger tax cuts. The average benefit for the poorest fifth of families with children would be $880 under the bipartisan proposal (compared to $0 under OBBBA) and would be $270 for the middle fifth of families with children (compared to $240 under OBBBA).

Figure 8

Other Restrictions in OBBBA Leave Out Millions of Children Based on Parents’ Immigration Status

This analysis does not account for restrictions added to the CTC that leave out children based on their immigration status, but other analyses have shown up to 2.7 million children might lose access to the credit due to these policy changes. Prior to OBBBA, children were required to have Social Security Numbers (SSNs) to be eligible for the CTC. A new restriction in OBBBA requires not only the child but also at least one parent or guardian to have an SSN.

As ITEP has previously reported, undocumented immigrants, who work and pay taxes despite not having an SSN, paid nearly $100 billion in federal, state, and local taxes in 2022. 8

Figure 9

Appendices

- State-by-state data on Child Tax Credit changes in One Big Beautiful Bill Act vs. proposed American Family Act

- State-by-state data on children left out of full Child Tax Credit under One Big Beautiful Bill Act in 2026

Endnotes

- 1. “Early Childhood Development and Education,” Office of Disease Prevention and Health Promotion, U.S. Department of Health and Human Services. https://odphp.health.gov/healthypeople/priority-areas/socialdeterminants-health/literature-summaries/early-childhood-development-and-education

- 2. Neva Butkus, “State Child Tax Credits Boosted Financial Security for Families and Children in 2025.” Institute on Taxation and Economic Policy, September 11, 2025. https://itep.org/state-child-tax-credits-2025/

- 3. Ken-Hou Lin, Carolina Aragão, and J. Adam Cobb, “Women, Minorities, and Non-Union Workers Continue to Dominate Low-Wage Markets, and Experience Job Insecurity and Limited Upward Mobility,” Population Research Center The University of Texas at Austin, November 2020. https://repositories.lib.utexas.edu/server/api/core/bitstreams/b8d43d20-1b10-45c2-8096-54c8bdc229dd/content

- 4. “DeLauro, DelBene, Torres Introduce Legislation to Make Permanent the Expanded, Monthly Child Tax Credit,” Press Release, April 9, 2025. https://delauro.house.gov/media-center/press-releases/delauro-delbene-torresintroduce-legislation-make-permanent-expanded

- 5. “H.R.7024 – Tax Relief for American Families and Workers Act of 2024,” 118th Congress, January 17, 2024. https://www.congress.gov/bill/118th-congress/house-bill/7024

- 6. The maximum refundable portion would have increased by $100 each year between 2023 and 2025, bringing it closer to the maximum non-refundable portion. The earnings restriction would also have changed to allow the credit to phase in more quickly for families with more than one child. Under current law, the total amount that a family can receive phases in as one sum rather than per child. This means that larger families may receive a smaller credit per child than smaller families at the same income level.

- 7. As the Tax Relief for American Families and Workers Act of 2024 would only apply to years before 2026, it is unclear if the refundable portion would increase in 2026 if extended. For purposes of this analysis, we assume the refundable portion would be capped at $2,000 in 2026.

- 8. Carl Davis, Marco Guzman, and Emma Sifre, “Tax Payments by Undocumented Immigrants,” July 30, 2024. https://itep.org/undocumented-immigrants-taxes-2024/