By Jenice R. Robinson and Steve Wamhoff

One of the key challenges of the 11-years-and-counting economic recovery is that the benefits have not been equally shared, even now with unemployment rates at record lows.

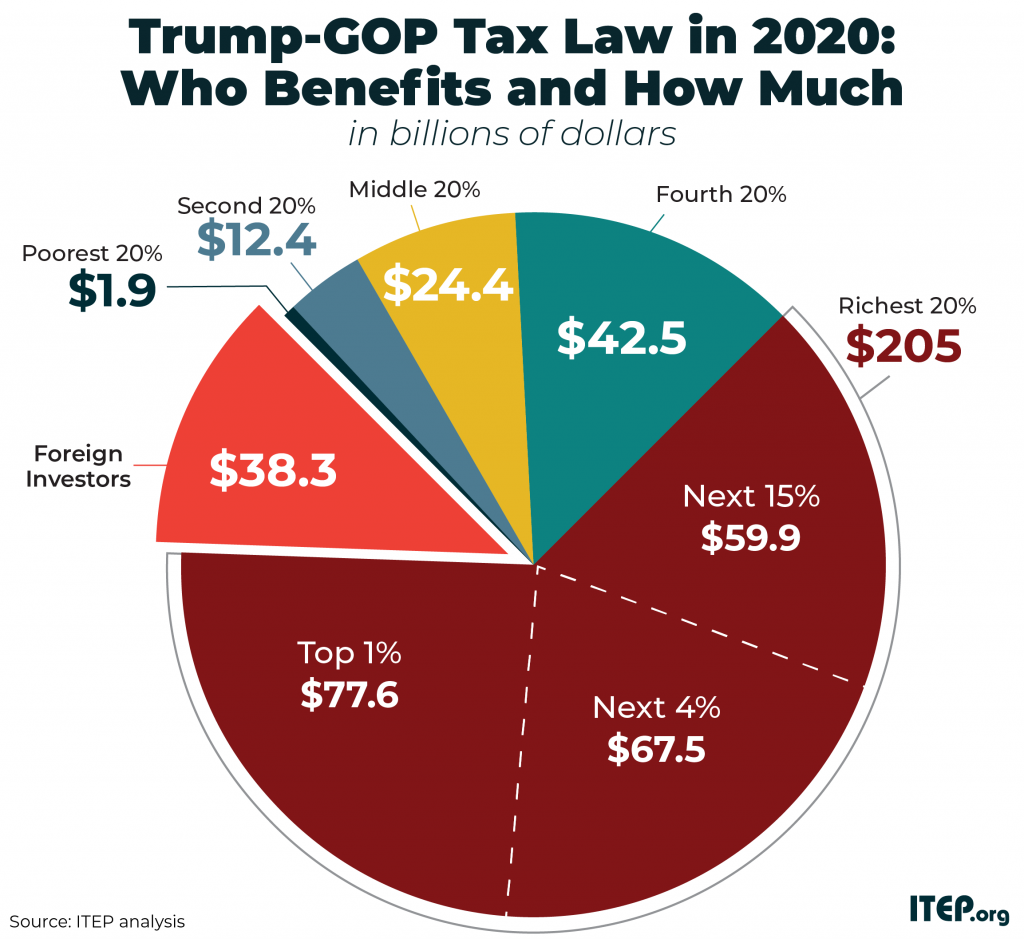

The nation’s richest families recovered from the economic downturn more quickly and built even more wealth, creating an even wider chasm between the richest and poorest individuals and families. The 2017 Trump-GOP tax law exacerbated this trend by reserving most of its tax cuts for wealthy Americans and foreign investors.

Of the tax cuts it showered on Americans, half went to the richest 5 percent and more than a quarter went to the top 1 percent. These lucky households received the biggest tax cuts in dollars and as a share of their income. They particularly benefited from the law’s dramatic tax cuts for corporations, which, in turn, flowed to shareholders in the United States and abroad in the form of stock buybacks.

Now that multiple data points reveal the current administration, which promised to look out for the common man, is, in fact, presiding over an upward redistribution of wealth, the public is being treated to pasta policymaking in which advisors are conducting informal public opinion polling by throwing tax-cut ideas against the wall to see if any stick. But the intent behind these ideas is more transparent than a glass noodle. Proposals floated by administration officials range from a payroll tax cut that would disproportionately benefit the well-off to a capital gains tax break that would almost exclusively benefit the rich.

The latest pronouncement, reported in the Washington Post, would require corporations to pay a minimum tax. As our colleague Matthew Gardner pointed out in a statement, “A White House proposal to follow Trump’s massive corporate tax cuts with a minimum corporate tax would be like shooting a person on Fifth Avenue and then offering them a band-aid.”

And, he also wrote: “Anyone who was serious about tax reform would have proposed fixing the minimum tax, not repealing it (as the 2017 Trump tax law did). And if the administration was serious about bringing it back, they’d agree to be quoted saying so—and maybe sketching out a specific plan.”

The thinking behind a minimum corporate tax, according to the unnamed sources, is that the revenue raised would offset the cost of a new “middle-class” tax cut.

One informal proposal that is being preposterously floated as a “middle-class tax cut” would allow people earning up to $200,000 to invest $10,000 in the stock market, tax-free. This would be in addition to employer-sponsored savings vehicles such as 401ks and also traditional and Roth IRAs.

This proposal reveals that advisors crafting tax policy either have no clue how the other half lives or are determined to make sure the best-off families continue to accrue more wealth.

Households that find it difficult to save and invest are those with working adults who pay federal payroll taxes and state and local taxes but earn too little to owe any federal personal income tax. Almost all of these households have incomes below $50,000. A federal personal income tax deduction or exclusion of any sort will not help these households.

The other obvious problem is that a lot of families earning less than $200,000 a year don’t have an additional $10,000 laying around waiting for another tax incentive to invest. Median household income is $63,179, according to Census data. So, $10,000 would represent nearly 16 percent of a median household’s pre-tax income. Half of that, $5,000, would represent about 8 percent–a substantial share of income for working families.

A Federal Reserve survey on the economic wellbeing of Americans found four in 10 households don’t have $400 to cover an emergency expense, and another worker survey shows one in three families run out of money before their next paycheck, including some households earning $100,000 or more. It’s hard to imagine how a new tax incentive for putting money in the stock market would benefit these families. A tax break for investing in the stock market will only benefit financially secure higher-income households—and corporations.

The thinking behind this proposal represents a warped world view: The non-rich, apparently, are just not good at making responsible decisions with their money. The rich are growing richer in part because of rising corporate profits and asset appreciation. Thereby, the rest of us just need to get on that train and put more money in the stock market. Presto!

And this is a generous interpretation of this proposal. A less generous interpretation would be that the advisors floating this idea know full well that it is simply a way to cut taxes for people who make nearly, but not more than, $200,000.

The public will undoubtedly be treated to more pronouncements of tax cuts for the middle class in the coming weeks and months. Each “proposal” should raise this question: Why did the 2017 tax law prioritize already-rich people and corporations over the rest of us and to the eventual detriment of critical programs and services that working people rely on to achieve economic security?

Policymakers who truly care about helping working people would present formal, targeted proposals and stand behind them. There are some good ideas here: https://itep.org/proposals-for-refundable-tax-credits-are-light-years-from-tax-policies-enacted-in-recent-years/