We’ve said it before, and we’ll say it again: states don’t have to wait for federal lawmakers to make moves toward progressive tax policy. And so far, 2019 has been a good year for equitable and sustainable tax policy in the states. With July 1 marking the start of a new fiscal year for most states, this special edition of the Rundown looks at how discussions in 2019 have been dominated by plans to raise revenue for vital investments, tax the rich and corporations fairly, use the tax code to help workers and families and advance racial equity, and shore up revenues for infrastructure.

Taxing the Rich

Bucking a recent trend of failed trickle-down supply-side economics experiments that have served to enrich wealthy and white households while failing to deliver promised economic growth and widespread opportunity, a number of states made strides this year toward implementing more progressive taxes on their richest residents to improve upside-down tax codes, reduce economic inequality, mitigate racial inequities built into state tax codes and help fund important state priorities.

2019 was a pivotal year for ILLINOIS, for example, where legislators and Gov. J.B. Pritzker are sending a graduated income tax amendment to the ballot in November 2020 for voters to decide on. With enough voter support, the Prairie State will trade in its inadequate flat personal income tax for a graduated rate structure that levies higher marginal rates on incomes over $250,000—including a top rate of 7.99 percent on all income for millionaires (compared to current rate of 4.95 percent)—and increases the corporate income tax rate. The proposed policy changes would generate over $3 billion for vital public investments and do so in a manner that improves tax fairness by requiring the rich and corporations to pay closer to their fair share.

Joining ILLINOIS, other states across the country—from MASSACHUSETTS to NEW MEXICO, HAWAII to NEW YORK—achieved various tax the rich victories led by lawmakers and people’s movements calling for equitable tax reform. In NEW MEXICO these victories included curtailing the exclusion for capital gains income and increasing the income tax rate for high earners. OREGON and WASHINGTON lawmakers enacted business tax increases to try to reach high-income households. CONNECTICUT, NEW YORK, and WASHINGTON raised taxes on those households through “mansion taxes” that apply higher real estate transfer tax rates to the sales of multi-million-dollar homes. And HAWAII strengthened its estate tax on inherited fortunes.

Help for Workers and Their Families

State-level Earned Income Tax Credits (EITCs) are effective tools for boosting incomes to help pay for the cost of living, especially for women and people of color. In 2019, six states made a range of improvements to their credits such as increasing the percent of the federal credit state residents receive, targeting increased credits to families with young children, and expanding eligibility to workers without dependents in the home.

CALIFORNIA lawmakers more than doubled the state’s EITC with three key expansions: eligible families with at least one child under age six will receive an additional $1,000 credit, the amount of the base credit was increased for some beneficiaries, and the income eligibility was increased to allow full-time minimum wage workers to benefit. MAINE took similarly substantive steps to strengthen its EITC for young workers and those without children in the home. Lawmakers lowered the age eligibility threshold for childless workers from 24 to 18 and increased the percentage of the credit for these workers from 5 to 25 percent (recognizing this group receives a fraction of the federal EITC compared to those with children in the home). All other eligible workers will see their credit increased from 5 to 12 percent of the federal EITC.

As part of a major tax reform bill, NEW MEXICO lawmakers increased the state’s Working Families Tax Credit from 10 to 17 percent of the federal credit. OHIO increased its nonrefundable EITC from 10 to 30 percent and removed a cap for taxpayers with incomes above $20,000. Lawmakers enacted these changes to offset the impact of a gas tax increase, however many low-income families were left out because the credit remains unavailable to those without positive income tax liability. In MINNESOTA, the state’s omnibus tax bill included a $30 million EITC expansion. Much of the benefit will go to families with three or more children, as well as workers without children in the home (in the form of both a larger credit and a higher income ceiling), although families with one or two children will also see increases. And in OREGON the EITC was increased from 11 to 12 percent for families with a child under age 3 in the home and from 8 to 9 percent for all other eligible workers.

Shoring Up Revenue for Infrastructure and Modernizing Sales Tax Bases

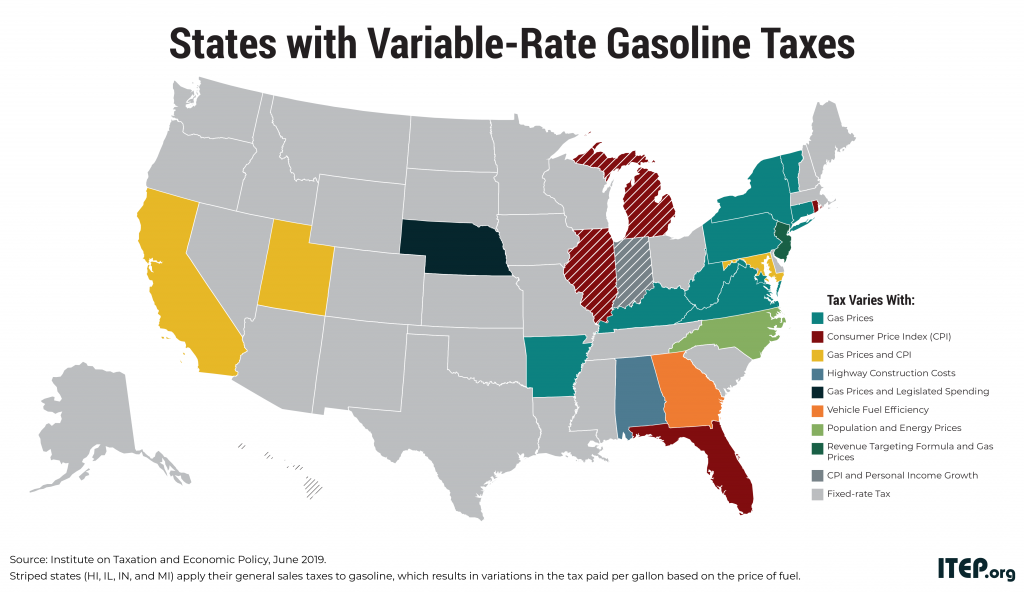

Gas taxes are the single most important revenue source that states use to invest in their infrastructure. A long-running trend toward boosting these taxes continued this year as a bipartisan group of states approved sizeable increases: ALABAMA, ARKANSAS, ILLINOIS, and OHIO. Notably, lawmakers in ALABAMA and ILLINOIS opted to set their gas taxes on a more sustainable long-run path by indexing their tax rates to inflation. OHIO’s increase was also notable because it was paired with an increase in the state’s EITC, which will help offset some of the impact of the tax for many low-income drivers.

Another area where states made progress on a bipartisan basis was in improving their sales tax collection practices as they relate to purchases made over the Internet. Last year the Supreme Court ruled in South Dakota v. Wayfair, Inc. that states can require sales tax collection by e-retailers that lack a “physical presence” within their borders as long as those states’ systems are sufficiently simple for sellers to navigate. In the words of the Court, this ruling ended a “judicially created tax shelter” and will allow for a more “even playing field” between local businesses and out-of-state retailers.

In the wake of that ruling states have moved quickly, but also responsibly, to enact laws and take administrative action requiring tax collection by e-retailers and online marketplaces. As evidence of this, Amazon Marketplace, eBay, and Etsy are each collecting sales tax in more than twenty states as of July 1, and that number is expected to continue growing in the months ahead as more collection requirements take effect.

Toppling Top-Heavy Tax Cuts and Missed Opportunities

The 2019 legislative session saw the demise of many large-scale, top-heavy tax cuts in most states where they were proposed.

Lawmakers in the COLORADO Senate blocked a bill early in session that proposed to cut the state’s flat income tax rate, preventing an annual loss of $280 million in revenue relied on for education funding. The bill not surprisingly would have disproportionately benefited the wealthiest residents and corporations. In MISSOURI, lawmakers defeated a proposal to shift to regressive sales taxes by raising the state sales tax rate nearly 50 percent while slowly cutting the top income tax rate. Other attempts to cut income tax rates in the Show Me State were also blocked this session.

NEBRASKA lawmakers quickly dismissed attempts to drive down income tax rates using arbitrary revenue “triggers” and then engaged in a long fight to also defeat proposed tax shifts that would have brought down property taxes by raising and expanding regressive sales taxes. And in WEST VIRGINIA, a bill that started out as exempting all Social Security income regardless of a person’s total income—resulting in a generous tax break for the state’s high-income retirees—passed a targeted income tax cut that applies only to taxpayers with income under $100,000.

Talk of tax cuts wasn’t curtailed in all states, however. ARKANSAS enacted top-heavy personal and corporate income tax cuts while missing the opportunity to enact a state EITC that would have targeted cuts to low- and middle-income working families who already pay a higher share of their income in taxes compared to the wealthiest state residents.

In WISCONSIN, lawmakers ultimately passed an income tax cut that, while targeted more to the middle-class than the top 1 percent, fails to make the tax fairness improvements Gov. Tony Evers’s tax cut plan would have made; his proposal would have provided more significant cuts to typical families and required the wealthy to pay a fairer share. And ARIZONA lawmakers ultimately signed off on a plan that conforms to federal tax changes while also making $386 million in permanent tax cuts, rather than reinvesting the funds to help close longstanding gaps in education and road funding or the state’s Rainy Day fund.

Limbo Land

Five states rolled into the new fiscal year without budgets in place, stymied in large part due to different tax policy priorities. MICHIGAN also fits this bill, but their new fiscal year doesn’t start until October so they have more time before the clock runs out (though certainly many issues are still in dispute). This marks the ninth straight year MASSACHUSSETTS lawmakers have not finalized a budget before the start of the new fiscal year, but there are no major hang ups of note.

OHIO legislators haven’t reached a budget deal to send to the governor’s desk and time is running out as an interim budget is set to expire on July 17. Disagreement on how much or whether at all to roll back two $1 billion plus business tax loopholes is the major hold-up. How much to spend on across-the-board personal income tax cuts is another sticking point. Unfortunately, it appears Governor DeWine is urging lawmakers to back away from any changes to the business tax loophole, a disappointing development since both the House and Senate had previously supported eliminating the special 3 percent rate on pass-through income.

NORTH CAROLINA Governor Roy Cooper vetoed the state’s legislative budget objecting to the exclusion of Medicaid expansion, too little investment in public education, and the inclusion of deeper corporate tax cuts. As of this week, lawmakers appear to be at an impasse as the House is likely short of the votes it needs to override the veto and legislative leaders have rejected the governor’s compromise plan, which included a request for lawmakers to rethink their proposed corporate tax cuts and stance on Medicaid expansion. A stop-gap budget passed the House unanimously, so a government shutdown is not immediately looming. NEW HAMPSHIRE Gov. Chris Sununu also vetoed his state’s legislative budget, in part because he was opposed to rolling back corporate tax breaks to expand funding for public education. He is meeting with Democratic lawmakers this week to start working out an agreement.

The Work Continues

The end of state legislative sessions often marks the end of a hectic work season for lawmakers and policy wonks. As ITEP state policy staff transition to July-December work plans (and fit in some much needed summer reading!), we can look back on 2019 as a year of significant state policy progress and as a jumping-off point for continued momentum towards fairer tax systems, improved public investments, and greater economic opportunity and racial equity.

While most state legislative sessions are over, the work ever continues. To aid that work, consider adding to your summer reading list ITEP’s report, Moving Towards More Equitable State Tax Systems, which is rich in policy recommendations for elected officials, advocates, and residents. And keep reading the Rundown, as we’ll be tracking and reporting biweekly on tax policy developments in the states over the summer, returning to our weekly publication schedule in the fall.