Update (October 2023): Massachusetts Gov. Maura Healey signed a CTC increase into law. The legislation will increase the state’s child and dependent tax credit from a maximum credit of $180 to $440 in 2024 ($310 for the current tax year) and eliminate the existing two-dependent cap. This is not included in the numerical counts in this brief.

Key findings

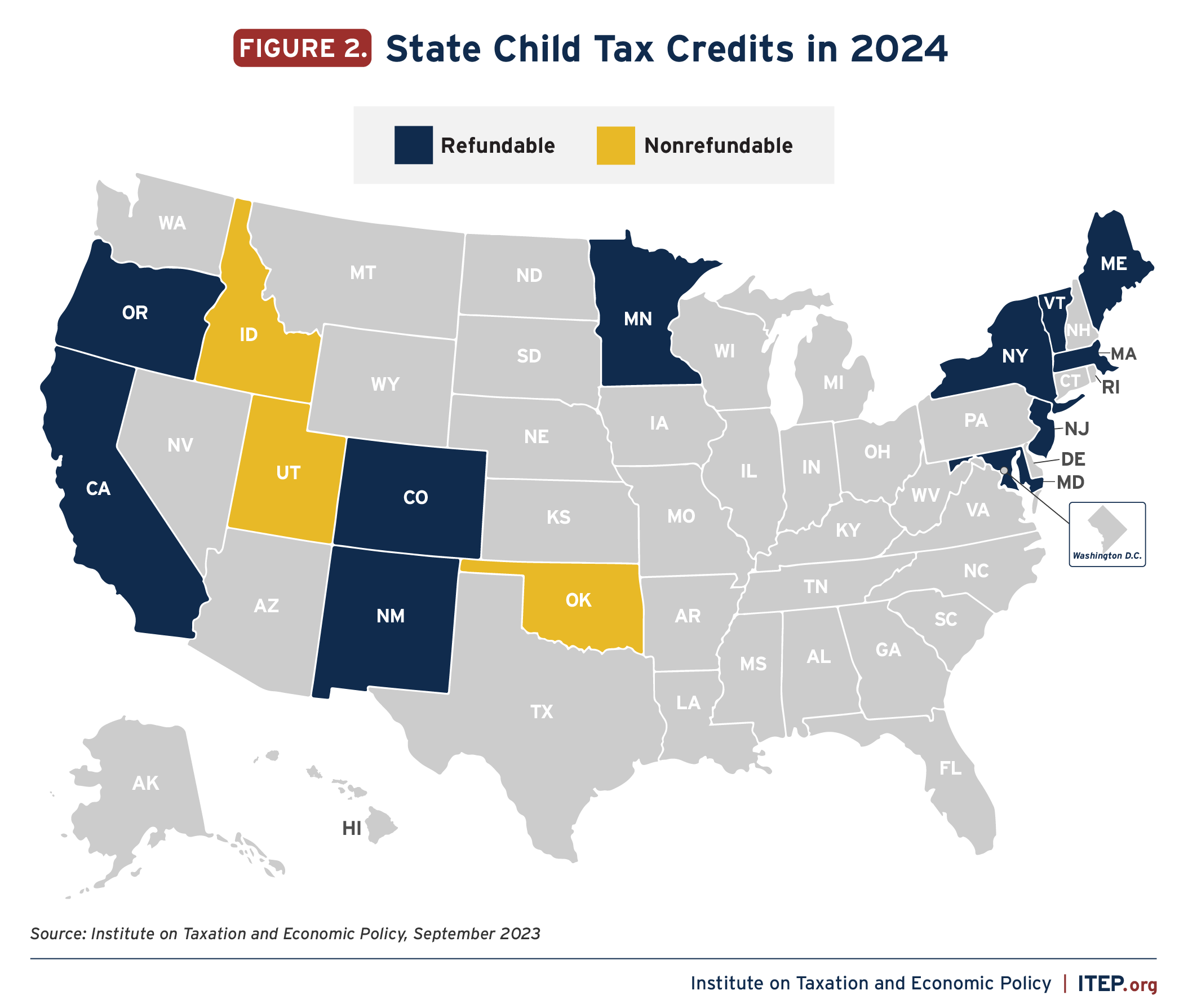

- Fourteen states provide Child Tax Credits to reduce poverty, boost economic security, and invest in children. States with fully refundable Child Tax Credits in 2024 are California, Colorado, Maine, Maryland, Massachusetts, Minnesota, New Jersey, New Mexico, New York, Oregon, and Vermont. Idaho, Oklahoma, and Utah offer nonrefundable credits.

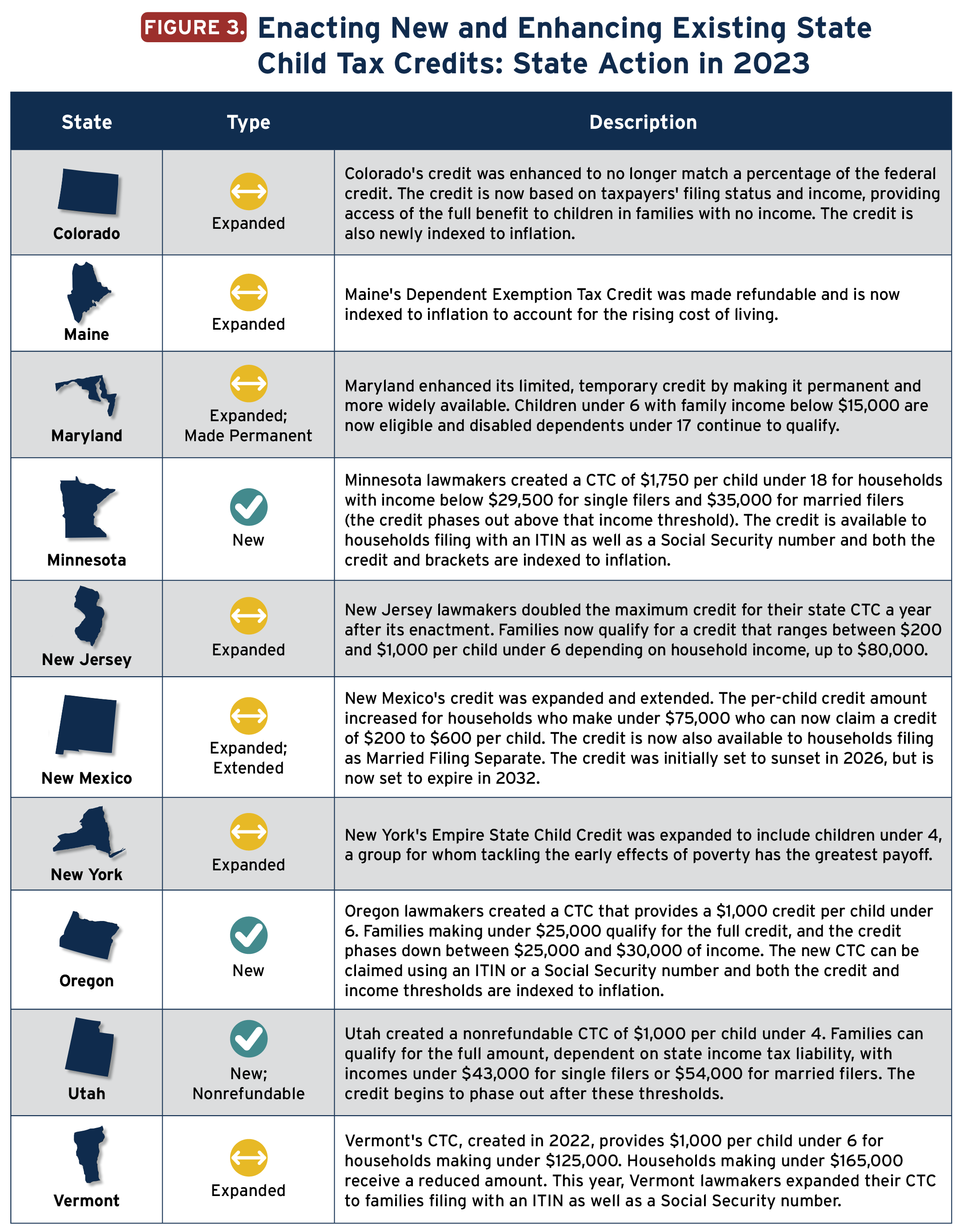

- This year alone, lawmakers in three states – Minnesota, Oregon, and Utah – created new Child Tax Credits while lawmakers in seven states expanded existing credits. Meanwhile, Arizona lawmakers created a one-time nonrefundable child tax rebate.

- State Child Tax Credits are larger than ever before, with five states – Colorado, Minnesota, New Jersey, Oregon, and Vermont – offering refundable credits at or above $1,000 per qualifying child. In all states collectively, these credits amount to a multibillion-dollar investment in children.

- To maximize impact, lawmakers should consider making their credits fully refundable, not including an earnings requirement, setting a maximum amount per child instead of per household, setting state-specific phase-out ranges that target low- and middle-income families, indexing to inflation, and offering the option of advanced payments.

Child Tax Credits (CTCs) are an effective tool to bolster the economic security of low- and middle-income families and position the next generation for success. When designed well, they counteract some of the deficiencies in the federal CTC and lead to meaningful reductions in child poverty and deep poverty.[1]

More state lawmakers are choosing to help families in this way: in 2024, 14 states will provide Child Tax Credits, many of which are targeted to those who most need them and made refundable so that children in the lowest-income families are not excluded from the full benefits. Together these credits constitute an annual multibillion-dollar investment in the next generation. As more states consider creating or strengthening these credits, lawmakers should design them for maximum impact.

Child Tax Credits: A Critical Tool to Help Families Make Ends Meet

Refundable Child Tax Credits boost the after-tax incomes of qualifying families and offset some costs of raising children. These policies are especially important for the economic security and stability of lower-income families, helping avert unexpected hardship that can threaten basics like housing, food, and utilities. Child Tax Credits are associated with reduced poverty, higher financial and household stability, improved child and maternal health, better educational achievement, stronger future economic outcomes, and more.[2] These benefits are stronger with well-designed credits.

CTCs can boost the after-tax incomes and economic security of families of all races. When designed well, these credits are particularly helpful to the lowest-income families and can make up for some of the damage done by other policies that hurt poor children and particularly harm Black, Hispanic, and Indigenous children.[3] Economic inequality, low wages, and child poverty are defining challenges in the U.S. Systemic racism causes these problems to disproportionately weigh on Black families and other families of color. The federal CTC – particularly the expanded version in place in 2021 – helps address these challenges.

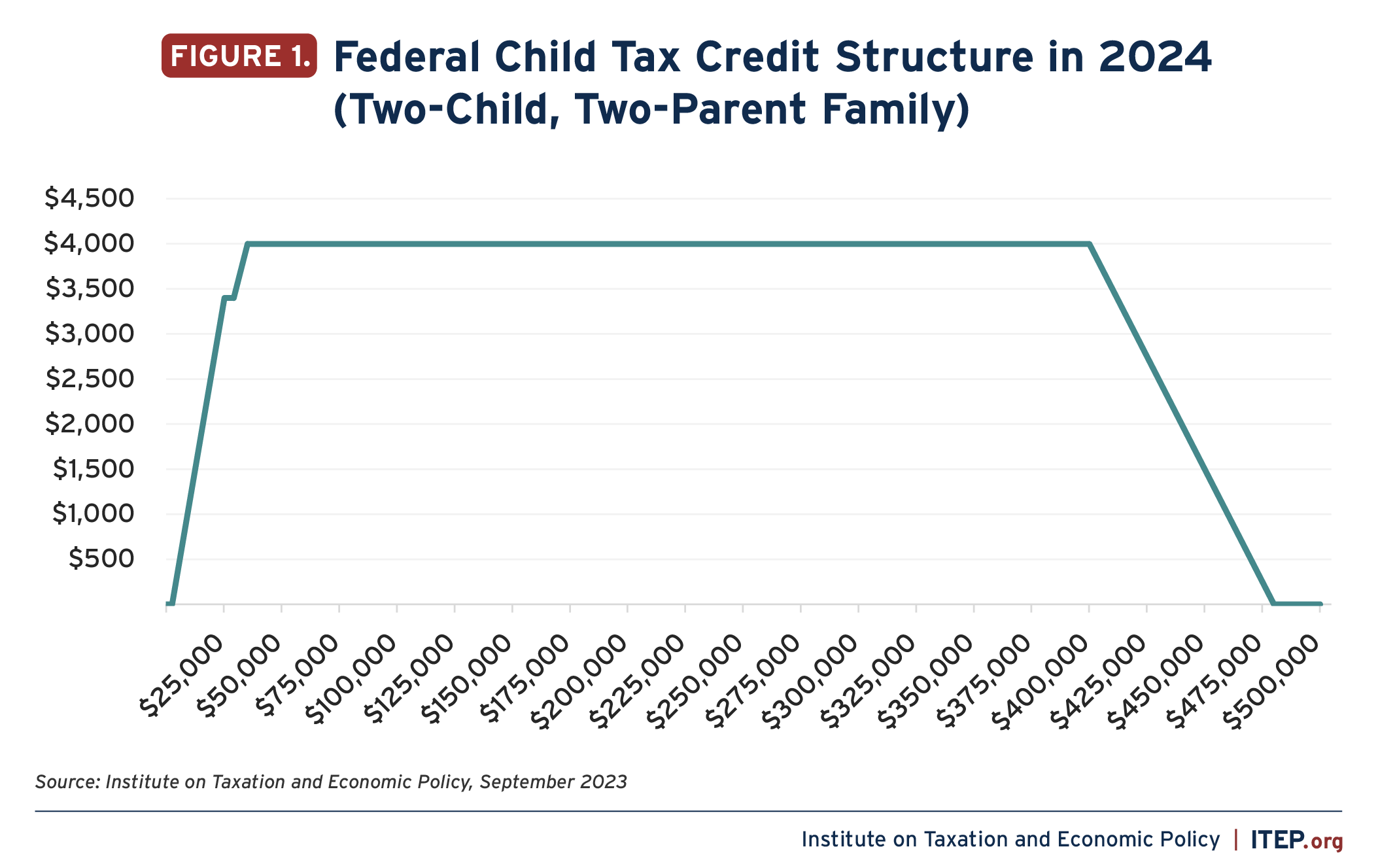

The federal CTC provides a credit of up to $2,000 for each dependent child under age 17. It phases out for married couples with incomes above $400,000 and for unmarried parents with incomes exceeding $200,000.

The federal CTC excludes some low-income families from receiving the full credit by requiring a minimum level of earnings and by not making the credit fully refundable to those whose income tax payments are smaller than the credit they would otherwise receive. Children whose parents or guardians earn less than $2,500 are ineligible for the federal CTC while families with earnings above this level receive a federal CTC limited to 15 percent of each dollar of earnings over $2,500 (until reaching a maximum credit of $2,000 per child). The CTC is also only partially refundable, meaning that families can only receive $1,500 per child in the form of a tax refund. In effect, the current CTC has a trapezoid-like structure where some families are too poor to receive any credit, some fall within the phase-in range, some benefit from the full credit, some fall within the phase-out range, and some families earn too much to receive the credit.

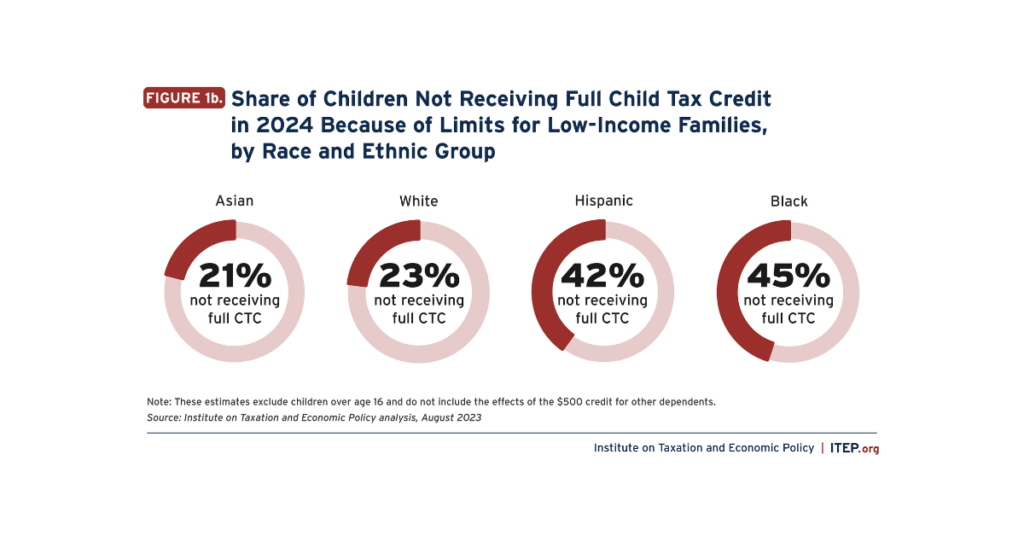

Under the American Rescue Plan Act of 2021 (ARPA), the credit was temporarily expanded—for 2021 only—to $3,000 for older children and $3,600 for children under 5. It was reformed to allow monthly credit payments rather than one annual lump sum. And most importantly, it was reworked to reach more children, including nearly one-third of children who live in families too poor to qualify for the credit under permanent law. Absent federal action, 45 percent of Black children, 42 percent of Hispanic children, and 23 percent of white children will not receive the full credit next year due to limits that prohibit lower-income families from accessing the credit either in full or in part.[4] Since current limits for lower-income families disproportionately leave out children of color, removing the limits would disproportionately help these groups.

Since its enactment in the late 1990s, the federal CTC has grown and changed. For instance, under the Tax Cuts and Jobs Act of 2017 (TCJA), the credit rose from $1,000 to $2,000 per child through 2025, was reshaped to allow more affluent families to claim it, and was written to exclude immigrant children without Social Security numbers.[5] Prior to the TCJA, all children whose parents met the income eligibility requirements, regardless of citizenship status, received the federal version of the credit.

This expanded version of the federal CTC in 2021 was wildly successful in reducing child poverty, cutting it by 46 percent by lifting 3.7 million children out of poverty before it was allowed to lapse in 2022.[6] Research has since shown that low and middle-income households overwhelmingly spent this boosted credit on housing, food, and clothing – a testament to how vital an expanded CTC is to helping families make ends meet month-to-month.[7] In the absence of federal action to reinstate those reforms, state lawmakers are increasingly creating Child Tax Credits to boost income and opportunities for children and families in their states.

More States Adopting and Expanding Child Tax Credits

More and more lawmakers are adopting and expanding state-level Child Tax Credits. As we head into 2024, 14 states are providing Child Tax Credit benefits to families with children.

This year alone, lawmakers in three states – Minnesota, Oregon, and Utah – created new CTCs while lawmakers in seven states expanded their existing CTCs. Meanwhile, Arizona lawmakers created a one-time nonrefundable child tax rebate. These new and expanded credits are all permanent except for Arizona’s 2023 rebate, Oregon’s credit (which expires in 2029), and New Mexico’s credit (now scheduled to expire in 2032). These new and expanded credits are also larger than ever before, with five states – Colorado, Minnesota, New Jersey, Oregon, and Vermont – offering refundable credits at or above $1,000 per qualifying child

In 2023, three states – Minnesota, Oregon, and Vermont – passed bills to explore providing advanced payments throughout the year, rather than as a once-a-year lump sum, to help families with their normal bills and other expenses.

While most states have created CTCs that are independent of the federal Child Tax Credit, two states -Oklahoma and New York – have credits directly tied to some version of the federal CTC.

Oklahoma offers families a choice between a nonrefundable credit worth 5 percent of the federal CTC or a nonrefundable credit worth 20 percent of the federal Child and Dependent Care Tax Credit. The state limits the credit to taxpayers with incomes under $100,000. This credit doesn’t fully reach families in or on the verge of poverty because it is nonrefundable, meaning it cannot be used by lower-income families who have little state income tax liability but pay substantial amounts of sales, excise, and property taxes.

New York has a refundable credit worth $100 per qualifying child or 33 percent of the taxpayer’s allowable federal credit, whichever is greater. Lawmakers in New York decoupled their state credit (the Empire State Child Credit) from changes to the federal CTC occurring after 2017, so they continue to maintain a maximum credit of $330 (that is, 33 percent of the $1,000 maximum federal credit in place before TCJA) along with other pre-TCJA tax parameters. This year, New York’s legislature greatly improved the reach of the credit by extending eligibility to children under 4, recognizing that tackling the early effects of poverty has the greatest payoff.

In 2019, Massachusetts transformed two separate deductions into refundable credits. The Household Dependent Tax Credit replaced the state’s deduction for household dependents and now provides $180 per dependent and $360 for two or more dependents. Dependents in this case include a broad set of people: child dependents, senior dependents, and dependents with disabilities. People can choose between this Household Dependent Care Tax Credit or the Dependent Care Tax Credit but cannot take both. These are available on top of the state’s existing dependent exemption. Policymakers and advocates in Massachusetts continued to consider enhancements to this policy this year.

Other states have policies that resemble CTCs but are either far less robust or best thought of as state CTCs in name only.

In 2018, Idaho and Maine added nonrefundable dependent credits to their tax codes to replace lapsed personal exemptions. In practice, exemptions directly reduce taxpayer income while a credit reduces tax liability. Maine improved upon its credit this year by making it refundable. Generally, these credits would be stronger if they were available on top of existing dependent exemptions or if they were made substantially larger (and refundable, where applicable) to account for the lack of dependent exemptions in these states. Colorado also lacks a separate dependent exemption.

California also offers personal credits (via the California Dependent Exemption Credit) in place of exemptions, yet this is in addition to the state’s Young Child Tax Credit. These credits are broadly comparable to dependent exemptions that are offered in most states.

States Should Design Child Tax Credits with Equity in Mind

The lapse of 2021’s federal Child Tax Credit enhancements inspired state action in 2023 and could continue to do so going forward. In the absence of additional action by Congress, and to best support families with children, states have several options to strengthen economic security and child well-being through new or expanded CTCs. Lawmakers should design these state CTCs with an eye toward equity by ensuring that the credit reaches as many low- and moderate-income children as possible.

1. Ideally, lawmakers should create standalone refundable CTCs that would ensure that all children benefit, regardless of their family’s employment or immigration status.

The advantage of implementing a credit separate from the federal CTC is that states can avoid the shortcomings of the federal credit (particularly the earnings requirement and lack of full refundability) that keep many lower-income families from receiving the full benefit. Instead, states can use the flexibility they have to determine the scope and scale of their credits without these restrictions.

That flexibility allows state lawmakers to:

- Make the credit fully refundable. Refundability is key to the CTC’s success. If a credit is refundable, taxpayers receive a refund for the portion of the credit that exceeds their income tax bill. Refundable credits help offset all taxes paid, not just income taxes, helping mitigate some of the regressive effects of state and local sales, excise, and property taxes.

- Avoid an earnings requirement. Earnings requirements mean that families with lower earnings get a smaller credit or no credit at all, paradoxically structuring a policy meant to help children to exclude kids who are the most in need. All children, regardless of the amount of income their parents bring in per year, should benefit from a robust state CTC.

- Set a maximum amount per child, rather than per household, to not penalize children in larger families. Lawmakers should also provide a more robust credit to younger children in their formative years when an income boost is found to be most beneficial.

- Set state-specific phase-out ranges that can better target the credit to low- and middle-income families. Setting a lower phase-out range enables the state credit to reach families in need while dramatically reducing the cost. If lawmakers are most interested in poverty reduction, an administratively simple approach for states with Earned Income Tax Credits could be to mirror EITC phase-outs, creating a tightly targeted state CTC.[8]

- Index the credit to inflation so that it does not erode over time. Whether and how policies are indexed for inflation has major implications for their power to improve economic well-being and reduce poverty over the long run.[9]

- Make the credit available on an advanced or monthly basis. Research shows that monthly cash payments reduce poverty and keep it low year-round.[10] This provides families flexibility to meet financial needs in real time and prevent debt.

2. If unable to create a standalone credit, lawmakers could enact a CTC as a percentage of the federal credit in combination with a minimum credit.

States can piggyback CTCs on top of federal rules at a flat percentage rate, as many do with their EITCs. For example, a state CTC calculated as 10 percent of the federal CTC would amount to a $200 state credit for any child who receives it in full.

State lawmakers should not, however, amplify the worst features of federal law. It is important to ensure that children in families too poor to receive the full federal credit are not denied the full state benefit. Lawmakers should establish a minimum, refundable benefit of $200 per child for lower-income families. This option would still rely upon the federal CTC’s high phaseout range through 2025 (starting at $400,000 for married parents and guardians, $200,000 for single parents and guardians)—providing more sweeping tax cuts to families throughout the income distribution at a relatively high cost to state coffers. Decoupling from federal law in favor of a standalone CTC benefit, as described above, would allow states to implement their own, likely lower, phase-out ranges.

3. Lawmakers could also opt to fill the gap for children left behind by the federal CTC.

State lawmakers can make up for the shortcomings of the federal CTC by ensuring that children in families too poor to receive the full credit are brought up to the full $2,000 amount, or to some portion of that amount. This approach ensures that a state’s lowest-income children are not left behind. Of these three options, this is the most carefully tailored to reach only those families in the most vulnerable economic circumstances. As a result of its narrower reach, this option could also cost less than the other proposals described above, which may be appealing to some lawmakers concerned about the budgetary impact of more expansive CTC proposals.

Under any of these options, states should explore advanced or monthly payments in addition to annual payments. Recent federal experience suggests that this approach can play a role in meaningfully reducing child poverty, improving economic security, and expanding family access to critical resources like groceries, housing, and clothing.[11]

The approaches under options two and three would fail to bring in non-citizen children unless state lawmakers took additional action. Parents who are undocumented immigrants, or filers using Individual Taxpayer Identification Numbers (ITINs) often live, work, and pay taxes in the U.S. These families are often specifically left behind by federal and state policies. Lawmakers can ensure that these filers, who would otherwise meet eligibility criteria, are not denied access.[12]

Endnotes

[1] Sophie, Collyer, Megan Curran, Aidan Davis, David Harris, and Christopher Wimer. State Child Tax Credits and Child Poverty: A 50-State Analysis. Institute on Taxation and Economic Policy and Center on Poverty and Social Policy at Columbia University, November 2022. https://itep.org/state-child-tax-credits-and-child-poverty-50-state-analysis/

[2] Waxman, Samantha, et al., Income Support Associated With Improved Health Outcomes for Children, Many Studies Show: Refundable Tax Credits Among Programs that Boost Income. Center on Budget and Policy Priorities, May 27, 2021. https://www.cbpp.org/research/federal-tax/income-support-associated-with-improved-health-outcomes-for-children-many. Hardy, Bradley L., Child Tax Credit Has a Critical Role in Helping Families Maintain Economic Stability. Center on Budget and Policy Priorities, April 14, 2022. https://www.cbpp.org/research/federal-tax/child-tax-credit-has-a-critical-role-in-helping-families-maintain-economic

[3] Davis, Carl and Marco Guzman. State Income Taxes and Racial Equity: Narrowing Racial Income and Wealth Gaps with State Personal Income Taxes. Institute on Taxation and Economic Policy, October 4, 2021. https://itep.org/state-income-taxes-and-racial-equity/

[4] Hughes, Joe and Emma Sifre. “Expanding the Child Tax Credit Would Advance Racial Equity in the Tax Code,” August 29, 2023. Institute on Taxation and Economic Policy. https://itep.org/expanding-the-child-tax-credit-would-advance-racial-equity-in-the-tax-code/

[5] Guzman, Marco. “Inclusive Child Tax Credit Reform Would Restore Benefit to 1 Million Young ‘Dreamers’.” Institute on Taxation and Economic Policy. April 27, 2021. https://itep.org/inclusive-child-tax-credit-reform-would-restore-benefit-to-1-million-young-dreamers/

[6] Parolin, Zachary, et al. Absence of Monthly Child Tax Credit Leads to 3.7 Million More Children in Poverty in January 2022. Center on Poverty and Social Policy at Columbia University, February 17, 2022. https://www.povertycenter.columbia.edu/publication/monthly-poverty-january-2022

[7] Schild, Jake, et al. Effects of the Expanded Child Tax Credit on Household Spending: Estimates based on U.S. Consumer Expenditure Survey Data. National Bureau of Economic Research. June 2023. https://www.nber.org/system/files/working_papers/w31412/w31412.pdf

[8] Butkus, Neva and Aidan Davis. “Boosting Incomes, Improving Tax Equity: State Earned Income Tax Credits in 2023.” Institute on Taxation and Economic Policy, September 2023. https://itep.org/boosting-incomes-improving-equity-state-earned-income-tax-credits-in-2023/

[9] Collyer, Sophie, et al., Keeping up with Inflation: How Policy Indexation Can Enhance Poverty Reduction. The Century Foundation, August 25, 2022. https://tcf.org/content/report/keeping-up-with-inflation-how-policy-indexation-can-enhance-poverty-reduction/ and Grundman O’Neill, Dylan. Indexing Income Taxes for Inflation: Why It Matters. Institute on Taxation and Economic Policy, August 22, 2016. https://itep.org/indexing-income-taxes-for-inflation-why-it-matters-1/

[10] Parolin, Zachary, Elizabeth Ananat, Sophie Collyer, Megan Curran, and Christopher Wimer. 2023. "The Effects of the Monthly and Lump-Sum Child Tax Credit Payments on Food and Housing Hardship." American Economic Association Papers and Proceedings, vol. 113: 406-12. https://www.povertycenter.columbia.edu/publication/child-tax-credit-payments-on-food-and-housing-hardship

[11] Hamilton, Christal, et. al. Monthly Cash Payments Reduce Spells of Poverty Across the Year. Center on Poverty and Social Policy at Columbia University, May 9, 2022. https://www.povertycenter.columbia.edu/publication/monthly-cash-payments-reduce-poverty-spells

[12] “Most Common Uses of 2021 Child Tax Credit Payments: Food, Utilities, Housing, Clothes.” The Annie Casey Foundation Kids Count Data Center, March 22, 2022. https://datacenter.kidscount.org/updates/show/294-child-tax-credit-payments