Key Findings

The U.S. Treasury Department announced late last year that it will release draft regulations seeking to reduce the federal tax credits claimed by certain immigrants and their families. This brief reports on the consequences of these restrictions for one of several affected groups—people brought to the country as children who have received Deferred Action for Childhood Arrivals (DACA). Specifically, it shows how this group would fare under the regulations’ two most significant restrictions, which would apply to the Earned Income Tax Credit (EITC) and Additional Child Tax Credit (ACTC). We find that:

- 337,000 people who are either DACA recipients, or living and filing tax returns with DACA recipients, would be harmed by this policy change.

- The average affected DACA recipient has lived in the U.S. for almost 29 years.

- Only working families who file tax returns would be affected because the EITC and ACTC both require earned income as conditions of eligibility.

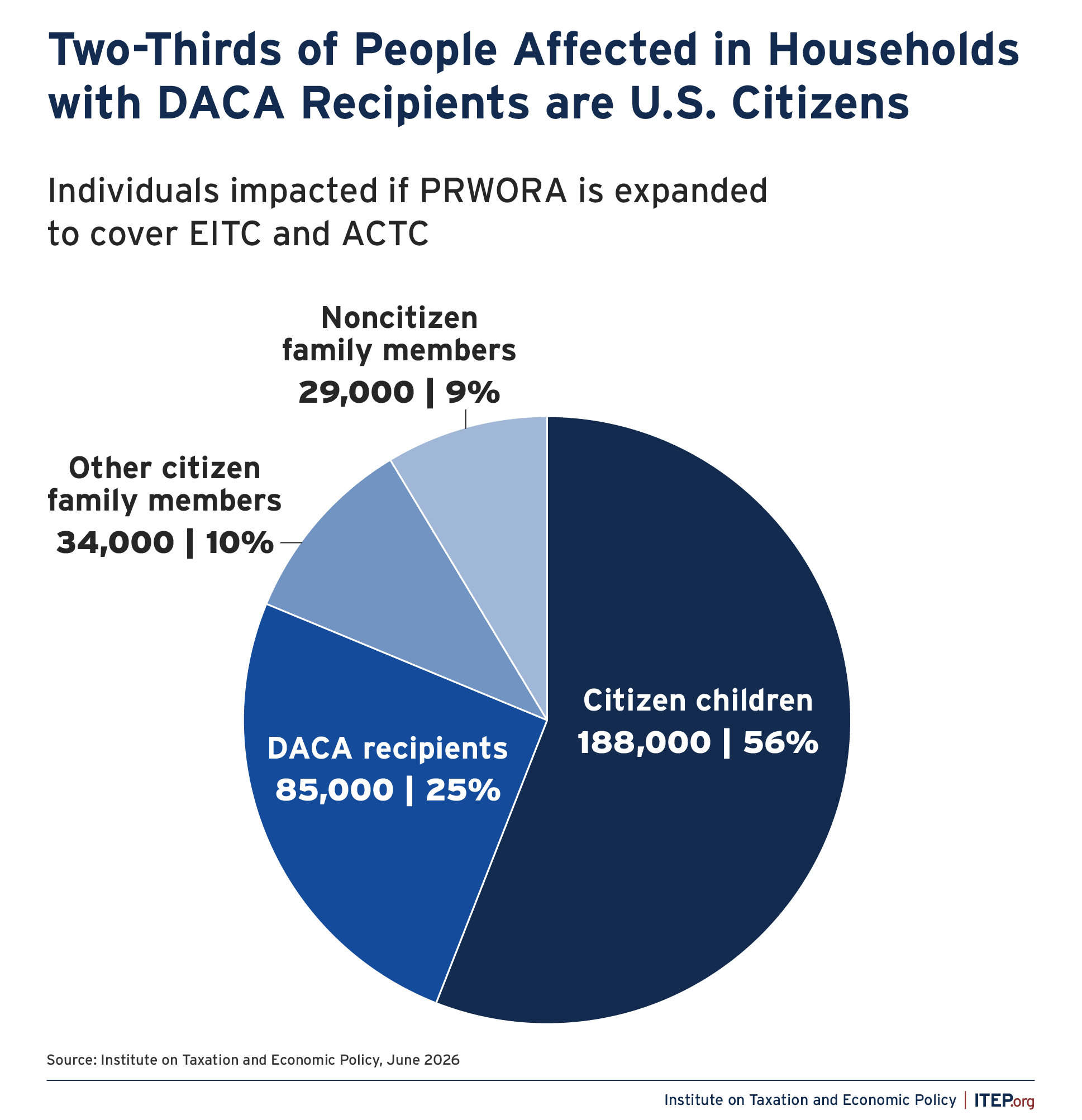

- Among families with DACA recipients, almost two-thirds of the people who would be harmed are U.S. citizens. More than half (56 percent) are U.S. citizen children and another 10 percent are U.S. citizen adults. In total, 188,000 U.S. citizen children would be harmed, along with 34,000 citizen adults.

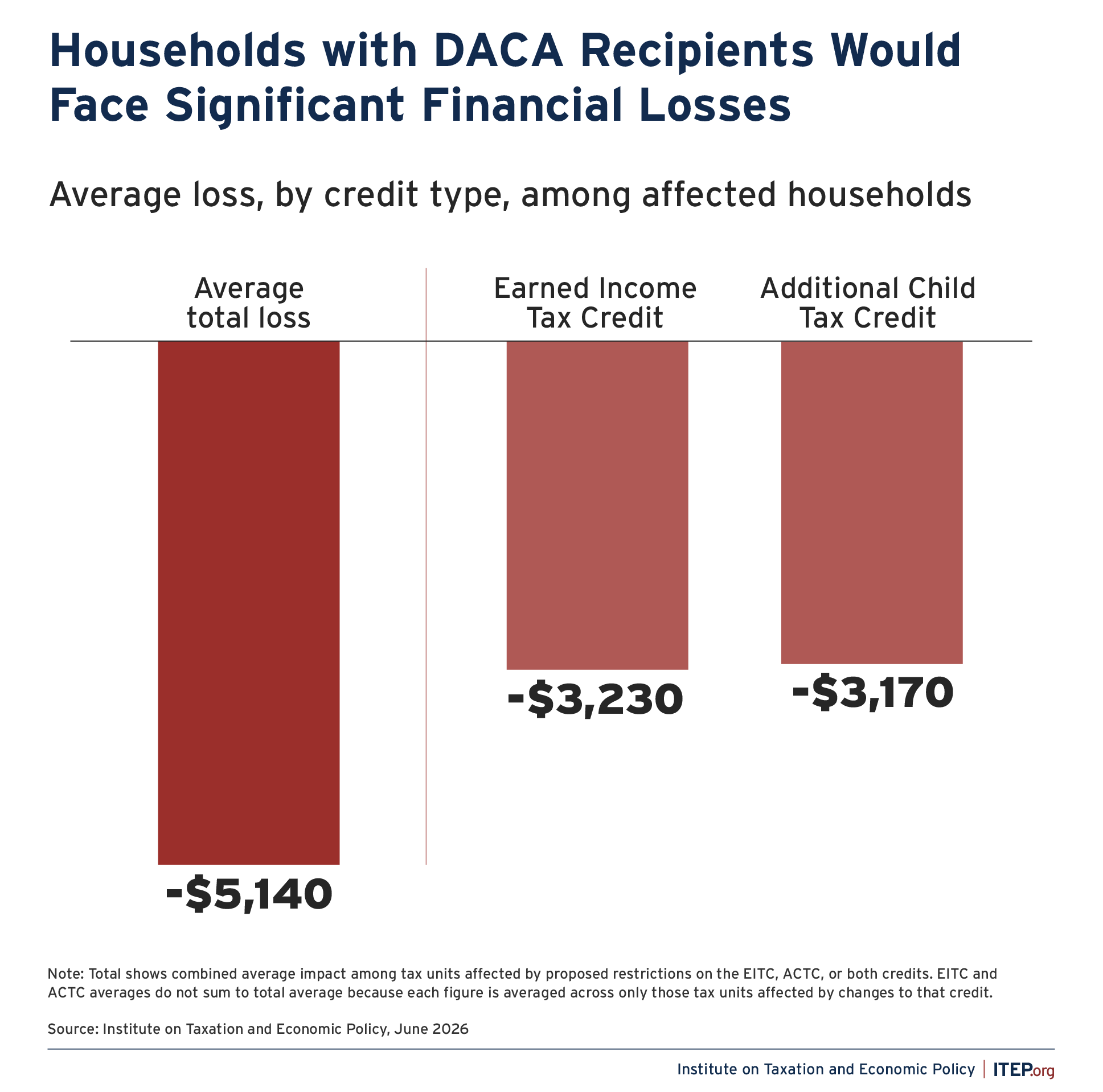

- The harm to families’ financial wellbeing would be substantial. Among families with DACA recipients, the average affected family would lose $5,140 in tax credits per year—an amount equal to 11.7 percent of their annual income.

- The financial loss for these families would be even larger in states that use federal credits as the starting point in determining eligibility for state EITCs or Child Tax Credits.

Introduction

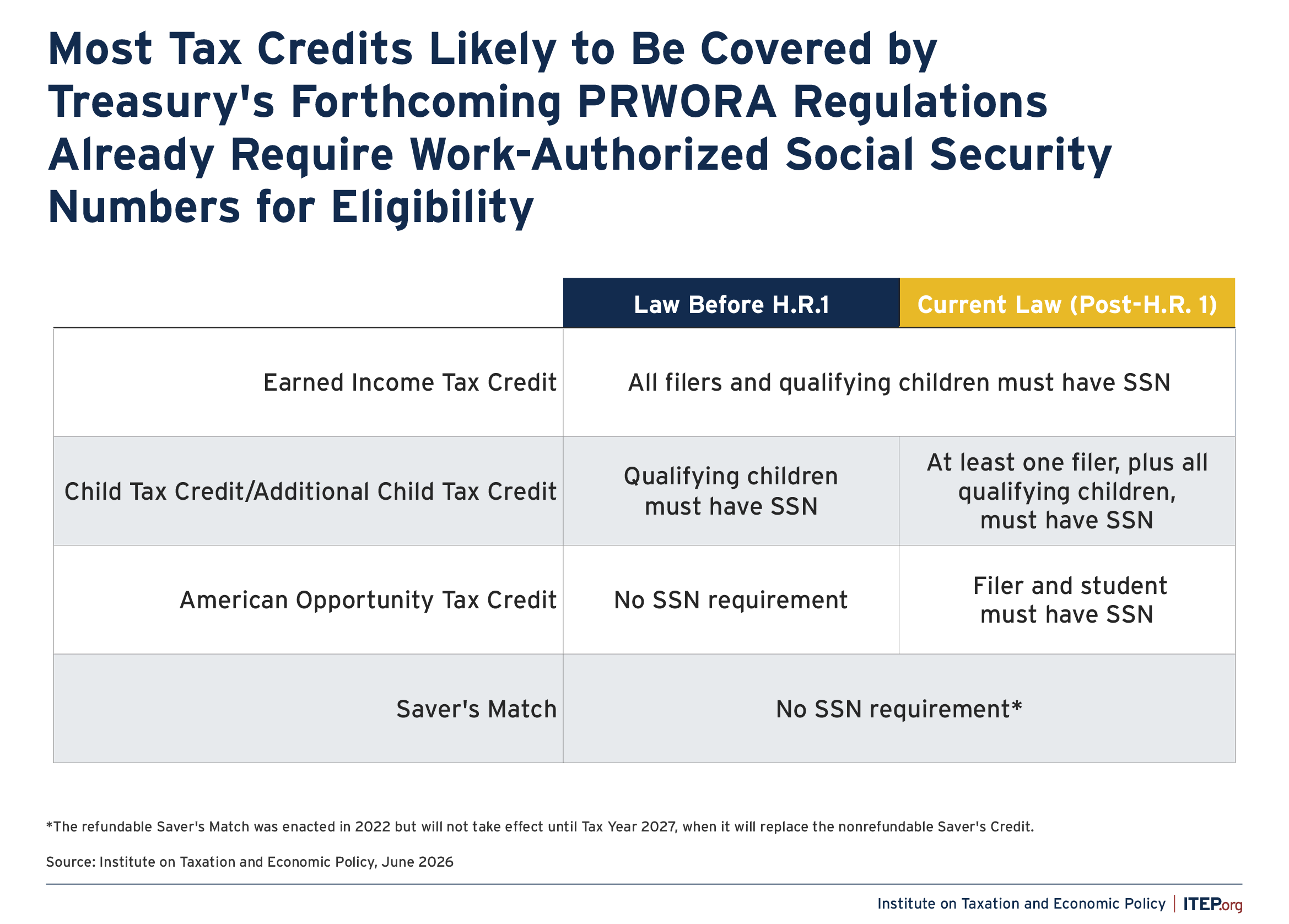

In November 2025, the Treasury Department announced that it will propose regulations barring certain immigrants from accessing the refundable portion of four federal tax credits—that is, the part of those credits that exceeds their federal individual income tax liability. The credits named in the announcement are the Earned Income Tax Credit (EITC), Additional Child Tax Credit (ACTC), American Opportunity Tax Credit (AOTC), and Saver’s Match Credit.

As seen in Figure 1, most of these credits already require taxpayers to have Social Security Numbers (SSNs) as a condition of eligibility. As a result, the practical effect of the proposal would be to restrict tax credit access for a variety of immigrant taxpayers who are lawfully present in the U.S. and have been issued SSNs valid for employment.

Some of the groups at risk of losing access to these credits are immigrants with Temporary Protected Status, asylum applicants, victims of serious crimes holding U visas, and recipients of Deferred Action for Childhood Arrivals (DACA).

Figure 1

Claiming these tax credits requires that taxpayers file a tax return with the IRS, so these restrictions will only affect those who are complying with federal tax laws by filing returns.

Moreover, while the proposed regulations have yet to be released as of this writing, we expect that individuals appearing on the same tax returns as these non-citizens (i.e. spouses and dependents) will also be harmed. This group includes many U.S. citizens.

The proposed rules are based on the Trump administration’s reinterpretation of legislative language from the Personal Responsibility and Work Opportunity Reconciliation Act of 1996 (PRWORA). PRWORA limited non-citizens’ access to “federal public benefits” to immigrants in certain categories, known as “qualified immigrants.” Last year, the Trump administration issued guidance that sought to expand the scope of what would be considered a “federal public benefit.” This guidance is currently the subject of litigation. In November 2025, the Justice Department quietly issued an opinion asserting that the refundable portion of certain tax credits could also be considered a “federal public benefit.” The Treasury announcement followed shortly thereafter.

This action marks a reversal from the position taken during the first Trump administration, when the Department of Homeland Security articulated a variety of reasons that tax credits should not be covered under PRWORA, including complexities related to mixed-status families and the fact that the tax system is structured to encourage claiming all credits.

The administration’s attempt to use PRWORA as a tool for restricting tax credit access comes after Congress already restricted immigrants’ eligibility for several tax credits and deductions under H.R. 1 of 2025.1 One notable new restriction is a requirement that families can now only claim the Child Tax Credit (CTC) if at least one parent has an SSN. This represents a stark departure from prior law which considered only the citizenship of the child in determining eligibility, in acknowledgement of the fact that the CTC is clearly aimed at improving children’s lives.2

Approximately 2.7 million American citizen children have lost access to the CTC because of the new requirement that their parents must have SSNs. The Treasury Department’s November statement indicates that its forthcoming regulations will be even more punitive than the approach agreed upon by Congress.

National Analysis

To shed some light on the potential impact of these regulations, this brief examines a subset of those affected—DACA recipients—and quantifies how they would be affected by restrictions on the two largest tax credits identified in the Treasury Department’s announcement: the EITC and the ACTC.

The EITC is designed to offset regressive payroll taxes and bolster the wages of lower-paid workers, especially those with children. Of the 24 million filers claiming the EITC in 2023, almost 21 million claimed at least part of the credit as a refundable rebate that went beyond their federal individual income tax liability.

The ACTC is the refundable portion of the Child Tax Credit (CTC) and it assists families with children who have modest incomes. This kind of support has been shown to be crucial in improving child wellbeing across a range of health, educational, and economic outcomes. More than 16 million tax returns claimed some amount of ACTC as a refundable rebate in 2023.

As mentioned above, Treasury has stated that it also intends to limit the ability of certain immigrants to claim two smaller tax credits related to the cost of college and saving for retirement, but they are omitted from this brief due to data limitations.

The analysis conducted here examines just one of the groups (DACA recipients) that would be affected by Treasury’s forthcoming proposed regulations. It is important to emphasize that this is not a comprehensive analysis of the forthcoming regulations because most (potentially 90 percent or more) of the people likely to be affected by this change are neither DACA recipients nor family members of DACA recipients. Our analysis is therefore best understood as a case study of the DACA recipient population rather than an analysis of the proposed regulations’ full impact.

We focus on DACA recipients in this brief both because available data and analytical techniques offer a higher level of confidence in analyzing this population, and because the DACA recipient population has been a particularly salient group in debates over U.S. immigration policy for many years.

The DACA policy was created in 2012, reflecting the judgement that young people brought to the U.S. as children, who have only known this country as their home, should not be a priority for deportation and should have work authorization so that they can support themselves. However, not all individuals brought here as children are eligible for DACA. To qualify, DACA requestors must have entered the U.S. before turning 16, been in the U.S. for at least 5 years as of June 15, 2012 (when the policy was created), and been under the age of 31 on that date. Additionally, they must meet certain educational requirements and not pose a threat to national security or public safety.

We estimate that by the end of 2026, there will be approximately 475,000 DACA recipients, each of whom was brought to the country as a child between 1981 and 2007. As of this writing, they range in age from 19 to 45, with an average age of 32.

Our analysis finds that the average DACA recipient came to the U.S. at about age 7 and has lived here for 28 years. Those affected by the proposed regulation are somewhat older and more settled, largely because the targeted credits are most often claimed by parents. We estimate that the average affected DACA recipient has lived in the U.S. for 29 years. Because eligibility for both the EITC and ACTC depends on having earned income, only working families would be affected.

We expect that each tax filing unit that includes a DACA recipient will lose access to the refundable portions of the EITC and ACTC under the regulations. That is, both DACA recipients and their family members would be harmed. Our analysis of the expected new restrictions reveals the following:

- Counting people who are either DACA recipients, or living and filing tax returns with DACA recipients, 242,000 people would be made worse off by the EITC change and 313,000 people would lose access to the refundable portion of the ACTC. There is significant overlap between these two groups, such that 337,000 people in total would be affected by at least one of these changes.

- Among families with DACA recipients, the average impacted family would lose $5,140 in tax credits per year—an amount equal to 11.7 percent of their $44,000 annual income. For families affected by the change in EITC eligibility, the average loss of EITC dollars would total $3,230 per year. For families impacted by new restrictions on ACTC eligibility, the average financial loss from changes to that credit would be $3,170 per year.

Figure 2

- Nearly two-thirds (66 percent) of the people living in households with DACA recipients who would be hurt by this regulation are U.S. citizens. This is because nearly all DACA recipients’ children are U.S. citizens, and because most spouses of DACA recipients are U.S. citizens. More than half (188,000) of those harmed are U.S. citizen children and another 10 percent (34,000) are U.S. citizen adults. Figure 2 provides an overview of the affected people.

Figure 3

State Tax Policy Effects

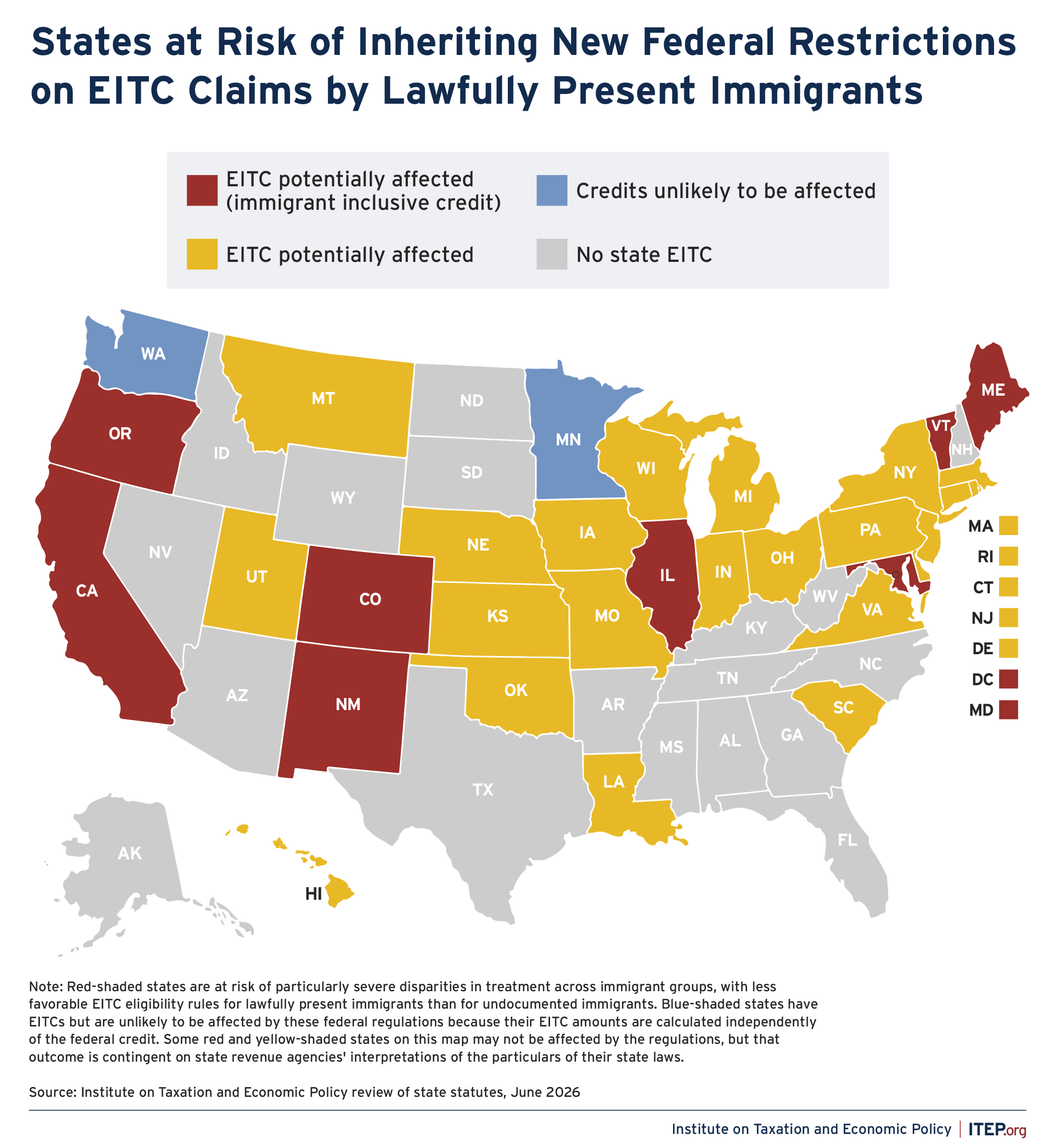

While the Treasury Department’s forthcoming regulations would only apply to federal claims, most state EITCs and some state CTCs piggyback on federal rules to a significant degree. If DACA recipients and other immigrants are barred from making full use of these credits on their federal tax returns, there is a risk that they will see their state tax credits automatically reduced as well. If so, they would lose even more than the $5,140 federal-level average estimated here.

Our analysis of state laws suggests that as many as 30 of the 32 states with EITCs are at risk of inheriting these new federal restrictions in their own tax codes.3 State CTCs are less likely to be impacted, though Oklahoma’s statute appears likely to pick up the federal regulatory changes under discussion.

Figure 4

These restrictions would be a poor fit for state tax codes because they would result in arbitrary cuts to state tax credits based on details of the federal tax calculation that should have no bearing on state law. While the goal of the restrictions at the federal level is to end refundability for certain families, that math used to make that happen does not translate to the state forms and some families would face reductions even to the nonrefundable portion of their state credits.4

Furthermore, the restrictions would be particularly nonsensical in states that have chosen to make their tax credits inclusive of immigrant filers. In these states, allowing the federal regulations to flow through into their own tax codes would result in their EITC eligibility rules being less favorable toward DACA recipients and other lawfully present immigrants than toward undocumented immigrants.

State lawmakers, of course, can fully or partially decouple their EITC and CTC rules from federal law. They should consider doing so both because the regulations do not mesh well with state law, and to avoid adding to the financial harm inflicted on immigrant families from the Treasury Department’s forthcoming regulations.

Conclusion

DACA recipients pay income taxes according to the same rules as other taxpayers—they are responsible for the same tax liabilities and are eligible for the same tax credits. This new rule would change that by drastically reducing tax credit claims by DACA recipients and their families, among others.

The Treasury Department’s statement announcing these forthcoming regulations emphasized their impact on non-citizen immigrants. But the average DACA recipient has been in the U.S. for 29 years and many DACA recipients have citizen family members. Our analysis confirms that many U.S. citizens would be harmed as well.

Specifically, we find that 337,000 people in households with at least one DACA recipient will suffer financial harm, and that nearly two-thirds (66 percent) of the impacted individuals are U.S. citizens. More than half (56 percent) of all affected people would be U.S. citizen children. The effects on these families would be significant, averaging $5,140 per year or roughly 11.7 percent of their average annual income of approximately $44,000.

Finally, it bears noting that a recent Gallup poll shows that 85 percent of Americans favor giving childhood arrivals the chance to become U.S. citizens. This finding raises doubts about whether the administration’s actions on this front are responsive to the public’s views on this issue.

Methodology

The bulk of the calculations performed for this brief were done with the U.S. Census Bureau’s 1-year, 2023 American Community Survey (ACS) data. While 2024 ACS data were available at the time we conducted this analysis, a supplementary research file for 2023 allowed for more detailed tax calculations in that year. Our process for identifying DACA recipients in the file involved first isolating the full universe of potential recipients and then selecting from among this pool based on administrative targets across a range of dimensions.

We arrived at the initial population of potential DACA recipients by applying the following filters to the ACS data:

- Reported citizenship status as “Not a citizen of the United States”

- Age at the time of entry into the U.S. of 15 or younger

- Entry date of 2007 or earlier

- Age of less than 31 in 2012

In addition to these criteria, to be eligible for an initial grant of DACA a requestor had to also be enrolled in school, have graduated from high school in the U.S., held a GED, or have been an honorably discharged veteran of the armed forces of the U.S. This methodology did not use education or military service as conditions for selection because the ACS data do not provide historical information on a respondent’s educational attainment or enrollment at the time of their initial DACA request, and continued school enrollment or graduation are not required for DACA renewal. Still, the vast majority of our pool at this point were enrolled in school, had a high school diploma or equivalent, or were a veteran—a fact that suggests these individuals likely met the abovementioned educational or military service criteria at the time of their initial request.

This filtering process yielded a pool of 1.6 million potential DACA recipients. From that population, we selected 530,000 of those potential recipients for inclusion in the analysis based on U.S. Citizenship and Immigration Services (USCIS) administrative data on the size and characteristics of active DACA recipients as of the end of Tax Year 2023. Using these data, we developed targets by state, age group, marital status, and country of birth using an iterative raking procedure. We preserved the comparative distribution of marriage rates by age group observed in the ACS data while taking care to match the overall number of married DACA recipients in the USCIS administrative data. We also used information from the 2024 National DACA survey to impose additional restrictions around the number of DACA recipients with children and the number of DACA recipients married to U.S. citizens, both of which are important for determining tax credit eligibility and amount.

We then reorganized the ACS households into tax units, which are people or groups of people who file one tax return. This reorganization relied on an algorithm similar to those described in research published by analysts within and outside of government. Our approach involved using information about individual relationships, ages, marital status, and incomes to determine dependents, heads of households, spouses, and filing statuses within households.

We also supplemented the ACS data with childcare expenses from the 2023 ACS Supplemental Poverty Measure research file, which is helpful for estimating potential claims of the Child and Dependent Care Credit.

Finally, we attached an identifier to certain married tax units that are ineligible for the EITC under current law because the spouse of the DACA recipient lacks a work-authorized Social Security Number (SSN). The ACS data allowed us to observe the share of DACA recipients married to noncitizens, which we validated against other survey data. Our review of information from the Pew Research Center and other sources suggests that approximately one-third of these noncitizen spouses are likely to lack work-authorized SSNs and thus we tagged one-third of DACA recipients married to noncitizen spouses as ineligible for the EITC in both our baseline scenario and our analysis of the proposed change, giving preference to spouses whose occupations suggest they might have status through work.

With the Tax Year 2023 base file in place, we then extrapolated to Tax Year 2026 levels using a technique that accounts for the fact that the DACA recipient population is both shrinking and aging over time as new initial requests are not being processed and current recipients grow older or exit the program by gaining lawful permanent resident status, not submitting a DACA renewal, losing DACA eligibility, leaving the country, or dying.

Specifically, we used a linear regression based on the trend in the total size of the DACA recipient population since 2021 to forecast that there will be 475,500 active DACA recipients by the close of Tax Year 2026. This is roughly 10 percent less than at the close of Tax Year 2023. We also accounted for the aging of the recipient population by observing the shift in the age distribution of recipients between December 31, 2023 and June 30, 2025 in the USCIS data, and then manually applied an additional 18 months of aging to move the data forward to December 31, 2026 levels.

We then re-weighted each tax unit to ensure that we had the correct number of recipients across six age bands. This resulted in observations aged 30 or below being down-weighted while observations aged 31 or older were up-weighted. Again, the net effect of this re-weighting was to shrink the overall population by approximately 10 percent, in line with our expectation for 2026.

After the re-weighting was complete, each type of income in the file was aged in accordance with the most recent Congressional Budget Office (CBO) projections for average income growth rates by source. Childcare expenses were also adjusted according to inflation.

Finally, with the 2026 file in place we then ran our own proprietary tax calculator, which we constructed to match the calculations found on federal tax forms and in recently enacted legislation. This calculator reflects actual federal tax law for 2026 in effect as of the publication date of this report. This calculator was used to compute federal tax liability and tax credit claims under the individual income tax, which was necessary to identify the refundable portions of the EITC and ACTC at risk of being denied under the Treasury Department’s forthcoming regulations.

Endnotes

- 1. “Temporary Assistance for Needy Families (TANF) at 26.” Center on Budget and Policy Priorities. Last updated August 4, 2022.

- 2. “Immigration and Citizenship Data.” United States Citizenship and Immigration Services. Active DACA Recipients – (Fiscal Year 2025, Quarter 4). “Temporary Protected Status and Deferred Enforced Departure.” Congressional Research Service. Accessed June 16, 2026. “Asylum Process in immigration Courts and Selected Trends.” Congressional Research Service. Accessed June 16, 2026.

- 3. No state offers a tax credit that piggybacks on the federal AOTC or Saver’s Match Credit, and thus changes in federal eligibility rules governing these provisions do not flow through to states.

- 4. Guzman, Marco, and Emma Sifre. Improving Refundable Tax Credits by Making Them Immigrant-Inclusive. Pittsburgh Tax Review, Volume 21, Number 2. July 2024.