This post was updated in June 2019 with additional resources.

The Treasury Department and IRS are expected to finalize regulations in the coming days that would make it more difficult for taxpayers to circumvent the new $10,000 cap on deductions for state and local taxes (SALT). The department crafted the regulations in response to large charitable donation tax credits enacted in Connecticut, New Jersey, New York and Oregon, but the rules also will extend to private school tax credits that have been abused as profitable tax shelters for many years.

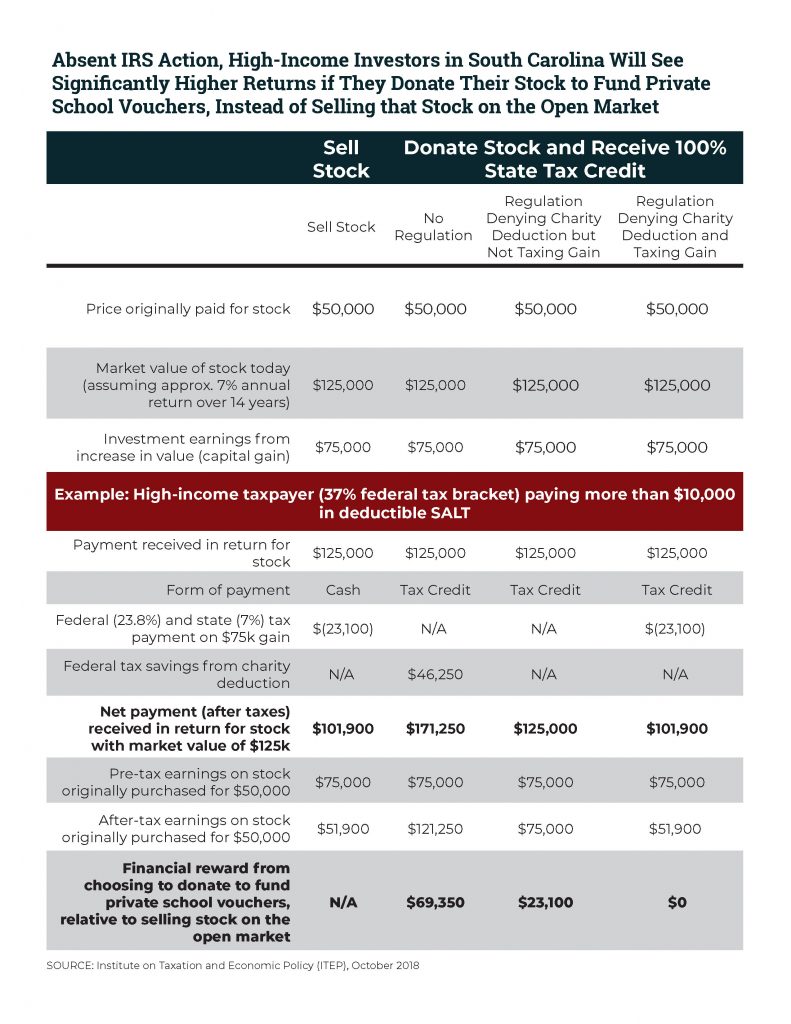

The tax credits that inspired these regulations allow taxpayers to make so-called “charitable donations” in lieu of paying state or local taxes. This relabeling is hugely beneficial to taxpayers on their federal returns since the cap on state and local tax deductions (a flat $10,000) is much lower than the cap on charitable giving deductions (60 percent of income). Put another way, the new federal law treats philanthropists much more generously than state and local taxpayers, and so the latter are predictably scrambling to look more like the former.

The IRS was correct to propose an even-handed rule that impacts not just the newest tax credits enacted in states like New York, but also existing credits for people who donate to fund vouchers that encourage families to send their children to private and religious K-12 schools. Private school “donors” in states such as Arizona and Alabama have leapt at the chance to turn a profit by claiming state tax credits and federal charitable deductions that are larger than the amounts they donate. And national groups promoting private schools, such as the American Federation for Children, urged the IRS to add a carveout to the regulations so that their particular tax shelter can remain intact.

Below are resources on the issue:

- What to Watch for When the IRS Releases Its SALT Workaround Regulations

This article identifies four aspects of the final regulations that could potentially differ from the IRS’s August 2018 proposal. Did private school groups win a weakened de minimis rule, a delayed effective date, or a full-scale carveout for themselves? And what steps, if any, will the IRS take to ensure that investors do not use these types of tax credits to dodge taxes on capital gains income? - ITEP Comments and Recommendations on Proposed Section 170 Regulation (REG-112176-18)

These are ITEP’s official comments on the proposed regulation. ITEP commends the IRS for proposing an even-handed regulation and urges the IRS to reject appeals by private school groups seeking a special carveout. The comments also include recommendations for ending tax shelter behavior by private school voucher donors who use state tax credits to avoid capital gains taxes, and by businesses seeking to classify their donations as deductible business expenses. - IRS was right to include private-school credits in new SALT regulations

This op-ed, published by The Hill, discusses how the Tax Cuts and Jobs Act of 2017 encouraged more state governments to embrace a little-known tax strategy to help residents avoid federal taxes. It also explains that the new regulations proposed by the IRS offer a reasonable approach to solving this problem. Rather than picking winners and losers, the IRS’s proposal would have a consistent and equitable impact on both the newest “workarounds” and the older private school tax credits. - SALT/Charitable Workaround Credits Require a Broad Fix, Not a Narrow One

This report, published in May 2018, explained that there are good reasons for the IRS to reconsider its treatment of state charitable tax credits. A taxpayer who makes a so-called “charitable donation,” only to later be reimbursed in full with a state tax credit, is not engaging in genuine “charity” according to any commonsense definition of the word. The report urged a broad overhaul of the federal tax treatment of state charitable credits, which is precisely what the IRS has since proposed. This report explains that a regulation treating some state tax credits differently from others would be unfair, arbitrary, and ultimately ineffective. - Twelve States Offer Profitable Tax Shelter to Private School Voucher Donors; IRS Proposal Could Fix This

This article spotlights the twelve states in which high-income taxpayers can reap a profit by claiming state tax credits and federal tax deductions that exceed the amounts they donate to private school voucher funds. It includes calculations of the precise level of profit that donors in each of these twelve states will be able to receive, at taxpayer expense, unless the IRS finalizes a regulation ending this tax shelter. In Alabama, for example, it shows how a $50,000 donation can generate up to $67,575 in tax cuts—meaning that a wealthy taxpayer could enjoy a $17,575 return each year for helping facilitate the movement of public dollars into private schools. - IRS Reopens Tax Loophole Sought by Sen. Toomey, but it Won’t Work in Pennsylvania

This article describes a troubling IRS “clarification” that has the potential to partly reopen the tax shelter that the IRS proposed closing. Specifically, the clarification raises the possibility of businesses getting around limits on the federal charitable deduction by relabeling their donations to private school voucher programs, and other causes, as business expenses rather than charitable gifts. Sensible laws in Pennsylvania, Illinois, and Virginia would prevent the exploitation of this loophole in those states. But most states with private school voucher credits remain vulnerable. - Tax Bill Would Increase Abuse of Charitable Giving Deduction, with Private K-12 Schools as the Biggest Winners

The SALT deduction cap included in the 2017 federal tax overhaul indirectly expanded a long-running loophole benefiting private K-12 schools. This report, written shortly before the bill’s final enactment, explains how the tax shelter operates and how the new federal tax law expanded its size and scope. - The Other SALT Cap Workaround: Accountants Steer Clients Toward Private K-12 Voucher Tax Credits

The tax shelter opportunity built into voucher tax credits quickly became a central feature of private schools’ efforts to raise money in some states. This report catalogues numerous examples of private schools, voucher organizations, tax accountants, and financial advisors telling their clients and prospective donors that “giving” is a way to “make money” by “bypassing” the federal government’s $10,000 cap on SALT deductions. These tax avoidance schemes would be rendered invalid under the proposed version of the IRS regulations, starting on Aug. 28, 2018. - How States Turn K-12 Scholarships Into Money-Laundering Schemes

This article offers a brief overview of the idea behind private school voucher credits: “Rather than include line-items in state budgets for spending on school vouchers, lawmakers ask taxpayers to undertake such spending on the state’s behalf, in return for a generous tax giveaway.” Sometimes states set up these roundabout systems because of a state constitutional ban on direct public funding of private and religious education. Other times, lawmakers have judged that labeling their voucher programs as tax credits simply makes them more politically palatable. Regardless of why these policies ended up on the books, the result has been a lucrative tax shelter that private schools have harnessed as a fundraising tool, and that their allies at the national level are fighting to preserve. - SALT Deduction Cap Should be Reformed, Not Repealed

This article discusses a major ITEP report about the SALT deduction more broadly. While the $10,000 cap is flawed policy, the report explains that there are good reasons for Congress to scale back tax deductions and outlines better options for doing so.