ITEP's Research Priorities

Opportunity Zones Bolster Investors’ Bottom Lines Rather than Economic or Racial Equity

December 12, 2019 • By Lorena Roque

This policy brief provides an overview of how opportunity zones are designed and highlights some of the flaws of the policy, including the detrimental impact opportunity zones have on communities of color.

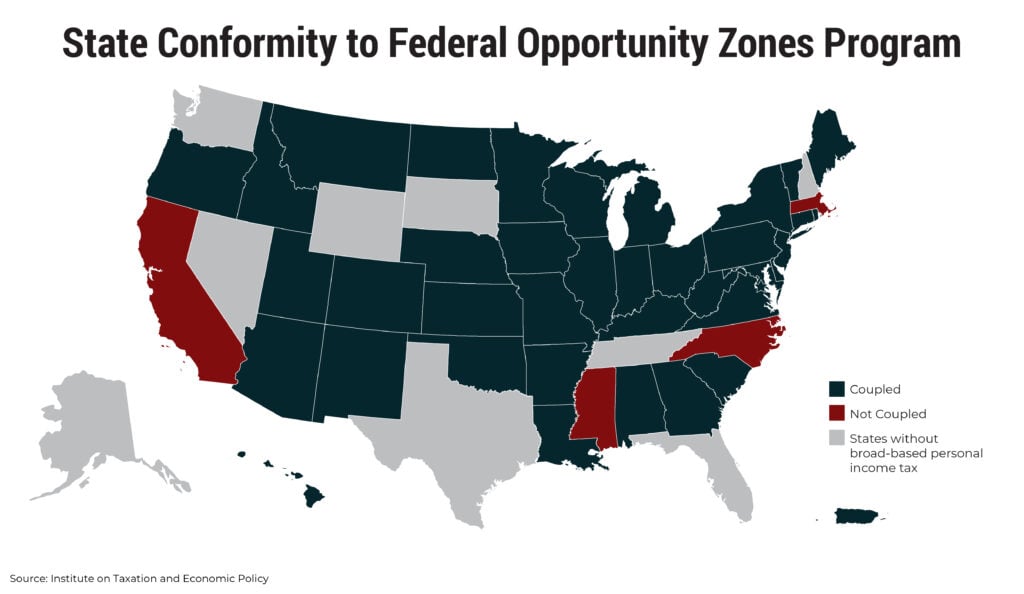

States Should Decouple from Costly Federal Opportunity Zones and Reject Look-Alike Programs

December 12, 2019 • By ITEP Staff

Post enactment of TCJA, lawmakers in most states needed to decide how to respond to the creation of this new program. Given the shortcomings of the federal Opportunity Zones program and its added potential costs to states, the most prudent course of action is three-pronged: States should move quickly to decouple; states should reject look-alike programs; and lawmakers should make investments directly into economically distressed areas.

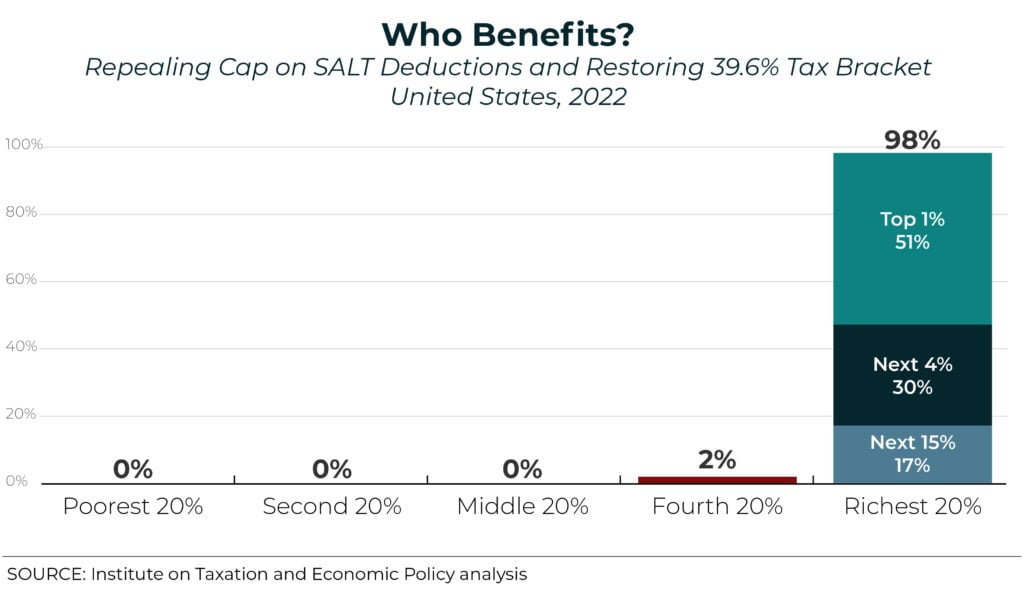

House Democrats’ Latest Bill on SALT Deductions Would Mean Bigger Tax Cuts for the Rich

December 11, 2019 • By Steve Wamhoff

ITEP estimates show that if the House Democrats' proposal was in effect in 2022, it would have a net cost of $81 billion in that year alone. The estimates also show that 51 percent of the benefits would go to the richest 1 percent of taxpayers in the U.S. Clearly, lawmakers concerned about the SALT cap need to go back to the drawing board.

Earlier this year, Amazon and Netflix made headlines when ITEP reported findings that these and at least 58 other companies paid no federal income taxes in 2018. One of the tax breaks they use to manage this feat is related to stock options. Some companies saved hundreds of millions, and in some cases more than a billion dollars, in taxes in 2018 alone with this break. It’s time for Congress to eliminate the stock options tax dodge.

How Congress Can Stop Corporations from Using Stock Options to Dodge Taxes

December 10, 2019 • By ITEP Staff

The stock option rules in effect today create a problem because they allow corporations to report a much larger expense for this compensation to the IRS than they report to investors. The result is that corporations can report larger profits to investors but smaller profits to the IRS, undermining the fundamental fairness of the tax system.

A new ITEP report explains that an income tax cut for cannabis businesses embedded in the MORE Act is probably larger than the new 5 percent sales tax. This means that the average cannabis retailer—and its customers—could expect to pay LESS tax if the MORE Act is signed into law. Congress might have good reasons for structuring legalization this way, but it is an underappreciated aspect of the bill that should be made clearer as this debate progresses.

Understanding the full tax consequences of cannabis legalization requires evaluating not only the excise taxes proposed in most legalization bills, but also the effects on the federal income tax liability of cannabis businesses.

The News Tribune: Washington State Leaders Must Tax the Way to a Just Society

December 7, 2019

The inequalities in our state’s tax code are well known, and have gained us the ignoble designation of “the most unfair state and local tax system in the country.” This medal of dishonor from the Institute on Taxation and Economic Policy is based on ITEP’s assessment of how fairly the tax burden is spread among […]

Beacon: New Ad Highlights Collins’ Vote to Pass Tax Break for Wealthy Corporations

December 4, 2019

Marking two years since Senator Susan Collins cast a key vote in support of the 2017 Republican tax overhaul, the progressive 16 Counties Coalition launched a new ad on Monday highlighting corporations like Amazon and Prudential Financial that paid no corporate income taxes following the bill’s passage. In comparison, the ad notes, “one in four Mainers will eventually see their taxes […]

Fox Business: Biden to Unveil Tax Proposal Targeting Corporations, Wealthy

December 4, 2019

Under Biden’s plan, companies like Amazon, Netflix, General Motors, JetBlue and IBM, which reported net income of more than $100 million in the U.S. but paid zero or negative federal income taxes, would be hit with a 10 percent minimum levy on book income. The minimum tax, which Biden’s campaign expects to impact 300 companies, […]

Worker Relief and Credit Reform Act

December 2, 2019 • By ITEP Staff

Data available for download The Worker Relief and Credit Reform (WRCR) Act would replace the existing EITC. In most cases, the WRCR credit would be $4,000 for single people and $8,000 for married couples. Eligible taxpayers would be allowed a credit equal to the maximum amount or their earnings, whichever is less. People caring for […]

Institute on Taxation

and Economic Policy

ITEP is a non-profit, non-partisan tax policy organization. We conduct rigorous analyses of tax and economic proposals and provide data-driven recommendations to shape equitable and sustainable tax systems.

Subscribe to ITEP Emails

Tax research and policy news in your inbox.

Promote Fair Tax Policy

Your gift to ITEP promotes tax justice. With your help, we do research that supports taxing millionaires and billionaires, taxing big corporations and raising revenue for the things our people, our communities and our planet need.

Together, we can create a country with more economic justice, more racial justice, more climate justice… and more tax justice.