Key Findings

- Immigrants and their families in as many as 30 states are at risk of seeing their state tax credits such as the Earned Income Tax Credit (EITC) and Child Tax Credit (CTC) reduced unless state lawmakers act, due to likely federal regulations prohibiting certain lawfully present immigrants from claiming the refundable portion of these credits.

- In addition to being needlessly punitive toward lawfully present immigrants authorized to work here, the expected regulations are also a poor fit for state tax codes because they reduce each family’s tax credit based on a complex federal tax calculation that has no bearing on state income tax law.

- Choosing to mirror these new federal restrictions in state law would lead to particularly nonsensical results in states that have made their credits immigrant-inclusive. In as many as 10 states, adopting these new federal restrictions could result in certain lawfully present immigrants facing harsher EITC restrictions than undocumented immigrants.

Federal Context

Federal law contains a definition of “federal public benefit” that was created by the Personal Responsibility and Work Opportunity Act of 1996 (PRWORA). This legislation overhauled the American safety net by converting Aid to Families with Dependent Children (AFDC) into the block grant we now know as Temporary Assistance for Needy Families (TANF). 1

It also disqualified many noncitizen groups from claiming TANF and other federal public benefits such as Supplemental Security Income, food stamps or SNAP, Medicaid, and more. Noncitizens unable to claim these benefits include those with Deferred Action for Childhood Arrivals (also known as DACA recipients), those with pending asylum applications, and those granted Temporary Protected Status.

The U.S. Treasury Department is now seeking to expand the definition of “federal public benefit” to include the refundable portion—the amount that exceeds your income tax liability—of the Earned Income Tax Credit (EITC), Child Tax Credit (CTC), American Opportunity Tax Credit (AOTC), and Saver’s Match Credit.

These credits were designed with a mix of objectives in mind, including boosting the wages of low- and moderate-income workers, bolstering the financial standing of families with children, defraying the cost of higher education, encouraging retirement savings, and offsetting some of the regressive taxes that disproportionately impact lower-income people like payroll, sales, and property taxes.

This proposed change would prevent people with certain immigration statuses from benefiting from the refundable portion of these credits. Having a Social Security Number is already a condition of eligibility for most of these credits, meaning these new restrictions target immigrants who are legally authorized to live and work in the U.S. who are already abiding by the law in filing tax returns. Because these credits also require income for eligibility, this change exclusively targets working immigrant families.

The Treasury’s proposed new restrictions on these credits would have a significant impact on certain immigrant communities starting as early as Tax Year 2026. New ITEP estimates, for example, indicate that there are 337,000 people who are either DACA recipients, or who are filing taxes with a DACA recipient, that would be harmed by the changes to the EITC and CTC. The average impacted household with a DACA recipient would lose $5,140 in federal credits—equivalent to 11.7 percent of their annual income. Additional losses would mount from lost state tax credits in states choosing to mirror the new federal restrictions in their own laws.

In total, millions of immigrant taxpayers and their families are likely to be harmed by these regulations. As of 2025, over 500,000 residents were registered as DACA recipients, 1.3 million were registered as having Temporary Protected Status, and 2.4 million had pending asylum cases. 2 Taking away credits such as the EITC and CTC from these groups will create more economic insecurity within their families and our communities.

State Conformity Implications

While the forthcoming regulations are expected to affect four federal tax credits, only two of those have any direct relevance to state tax law: the EITC and CTC.3 By curbing these tax credits, the proposed regulations aim to raise taxes on certain groups of immigrants compared to U.S. citizens in comparable financial situations.

Reducing these federal credits will have implications in every state, but the impact will be compounded in states that offer matching state credits because of the way state eligibility rules are connected to the federal statutes and regulations.

Most states tie their EITCs to the federal credit by matching a percentage of what a filer receives under Section 32 of the Internal Revenue Code. This has been considered a best practice, at least from the perspective of administrative simplicity, because it allows states to build on the power of the federal EITC with a state credit whose rules are largely already laid out in federal law.

Under the most straightforward state credit designs, when a tax filer receives an EITC at the federal level, a state simply matches a percentage of what was claimed on their federal tax form.

This feature of state law, which makes delivering the credit so simple, is now at risk of becoming a double-edged sword as new federal restrictions on eligibility potentially begin to flow through to the states. A working immigrant family receiving a reduced EITC when filing federal taxes will often see a reduced state EITC as well, since the state is providing a match against a smaller federal credit.

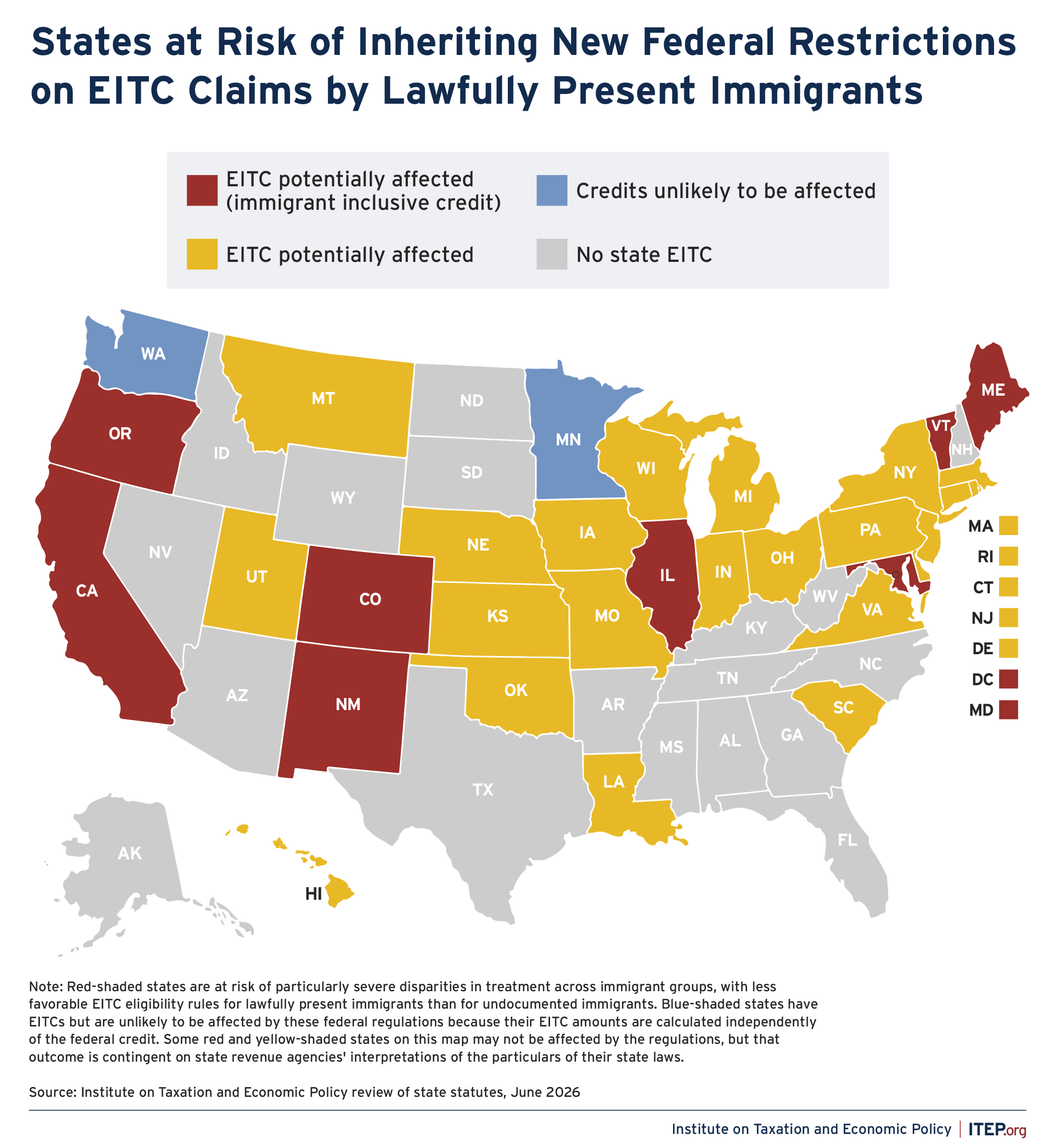

Figure 1

Our review of state statutes suggests that immigrants in up to 30 states with EITCs are at risk of seeing their state credits reduced by these regulations (see Figure 1). In addition, immigrant taxpayers in Oklahoma could also see their state CTC reduced because of the change.

Proposed Restrictions Would Not Translate Well to the States

Some states are likely to disconnect their tax codes from these new federal regulations because they do not want to harm lawfully present immigrants and their families who are working, using valid Social Security Numbers, and filing tax returns as required by law.

Putting aside any disagreements over the appropriate tax treatment of immigrant families, the proposed new federal restrictions are a poor fit for state law.

Under the forthcoming regulations, affected families would see the federal EITC transformed into a nonrefundable credit, meaning that they could no longer claim any portion of the EITC as a refund that goes beyond their federal income tax liability. Despite being poor public policy, there is at least a specific goal in mind for this federal calculation.

At the state level, however, a restriction of this kind will lead to arbitrary results. To illustrate, imagine two immigrant families claiming the federal EITC:

- The first family uses 40 percent of their credit to offset their federal tax bill and claims the other 60 percent as a refund which they no longer qualify for.

- The second family earns too little to owe any federal income tax before credits are applied, and therefore the entirety of their federal EITC is considered a refund that they can no longer receive.

- If these taxpayers live in a state with EITC rules connected to these new federal regulations, the first family would see its state EITC cut by 60 percent, while the second family would see its state EITC eliminated entirely.

The severity of the cuts would have no connection to the state income tax calculation. Rather, the percentage cut (60 vs. 100 percent) is solely an artifact of federal law and has no connection to whether the family happens to be claiming their state EITC as an income tax offset or as a refundable rebate.

Put another way, a regulation designed to eliminate refundability at the federal level in this way does not translate into elimination of refundability at the state level. Both refunded and nonrefunded state EITC dollars would be cut if states fold this regulation into their tax systems.

Proposed Restrictions Would Yield Nonsensical Result in Some States

The Treasury Department’s proposed regulations are in direct opposition to the trend in many states toward expanding eligibility for their credits to a wider range of immigrant filers, such as those who lack Social Security Numbers (SSNs) and file with Individual Taxpayer Identification Numbers (ITINs) instead.4 In fact, the regulations would result in nonsensical disparities across different immigrant groups with varying forms of legal status.

A longstanding feature of federal law restricts EITC eligibility to those taxpayers who have work-authorized SSNs. Ten states and the District of Columbia, despite conforming to many features of the federal EITC, have not mirrored this SSN requirement in their own tax codes. Instead, they allow their state-level EITCs to be claimed by SSN and ITIN holders alike.

Given the structure of state tax laws, it appears that state efforts to grant EITC eligibility to ITIN filers would not be impacted by the proposed federal regulations.5 Taken on its own, this is good news for immigrant families. But it also means that a bizarre result looms in these states: the possibility that lawfully present immigrants with SSNs will see their state EITCs reduced, while undocumented immigrants will continue to maintain full EITC eligibility.

In states affected by the federal regulations, immigrant tax filers who are filing with SSNs will receive a reduced state credit, calculated as a percentage of their reduced federal credit. Meanwhile immigrants who lack lawful presence, do not possess SSNs, and who file with an ITIN instead will receive a full state EITC.6

In short, conformity to Treasury’s proposed regulation could result in certain lawfully present immigrants receiving smaller state EITCs than undocumented immigrants or even being denied state EITCs outright. The 10 states, plus DC, currently at risk of confronting this indefensible outcome are identified with red shading in Figure 1.

Conclusion

Forthcoming restrictions on federal credits claimed by lawfully present immigrant tax filers are the latest in a series of federal tax changes with potentially consequential impacts for states. 7 While the states cannot prevent the federal government from pursuing this policy, they should decline to apply these new restrictions to their own tax credits to avoid compounding financial harm to immigrant families.

Endnotes

- 1. “Temporary Assistance for Needy Families (TANF) at 26.” Center on Budget and Policy Priorities. Last updated August 4, 2022.

- 2. “Immigration and Citizenship Data.” United States Citizenship and Immigration Services. Active DACA Recipients – (Fiscal Year 2025, Quarter 4). “Temporary Protected Status and Deferred Enforced Departure.” Congressional Research Service. Accessed June 16, 2026. “Asylum Process in immigration Courts and Selected Trends.” Congressional Research Service. Accessed June 16, 2026.

- 3. No state offers a tax credit that piggybacks on the federal AOTC or Saver’s Match Credit, and thus changes in federal eligibility rules governing these provisions do not flow through to states.

- 4. Guzman, Marco, and Emma Sifre. Improving Refundable Tax Credits by Making Them Immigrant-Inclusive. Pittsburgh Tax Review, Volume 21, Number 2. July 2024.

- 5. When states depart from the federal treatment of ITIN filers, they typically do so by disregarding the specific provision of federal tax law, 26 U.S. Code §32(m), that contains the requirement that eligible claimants must have SSNs. Treasury’s forthcoming regulation restricting EITC claims by lawfully present immigrants would not rewrite section 32(m), and thus is unlikely to change the way that states have typically granted their EITCs to people, such as undocumented immigrants, who file with ITINs.

- 6. For ITIN filers, the state EITC is typically calculated as a percentage of the federal credit that they would have received if not for the existence of 26 U.S. Code §32(m).

- 7. Davis, Aidan, and Wesley Tharpe. States Can Push Back Against Reckless Federal Tax Policy. Here’s How. Governing. January 22, 2026.