In a year of cautious uncertainty around current and ongoing revenues, many state lawmakers strengthened their tax credits for families and children.

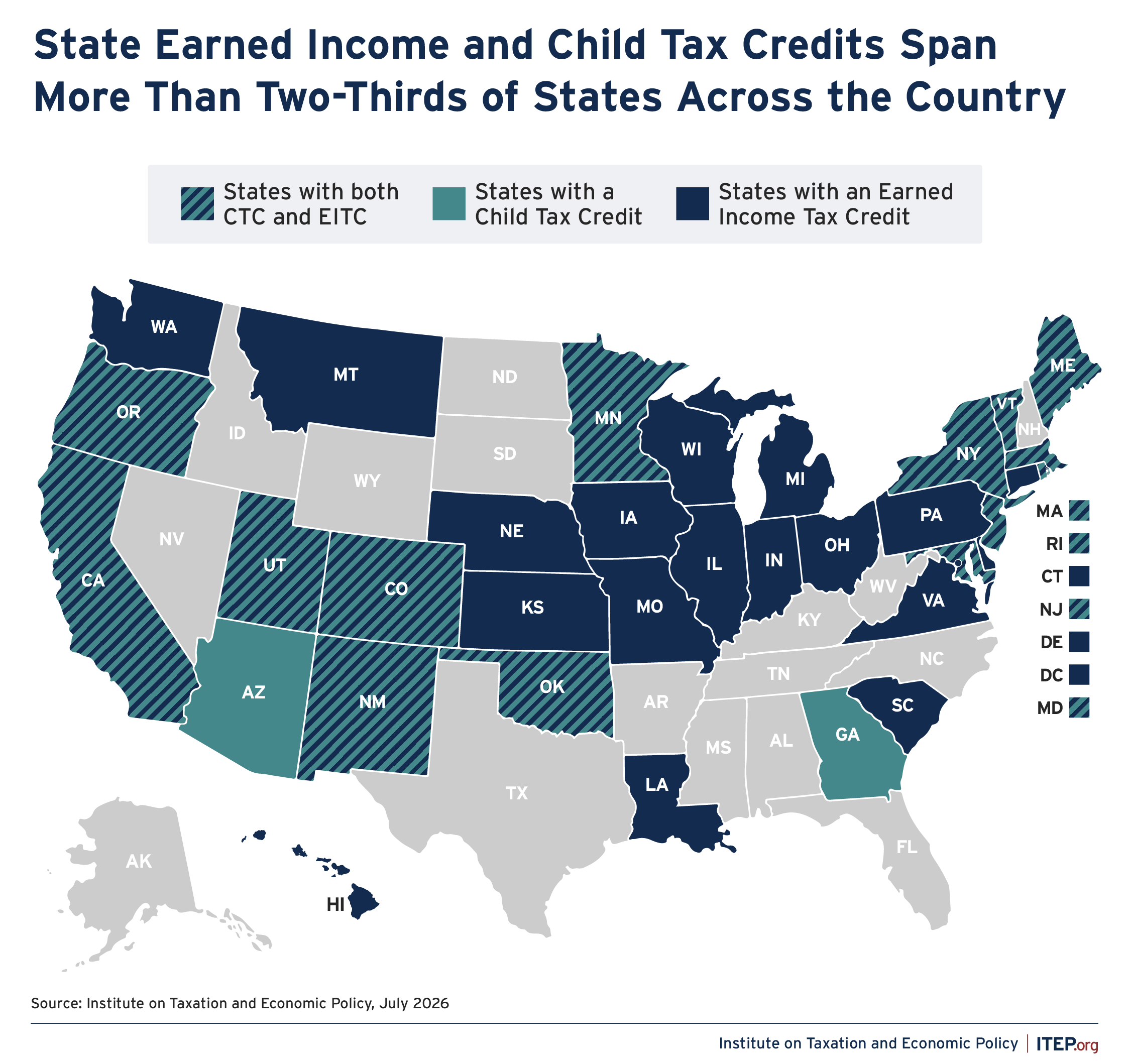

Most notably: Rhode Island lawmakers enacted the state’s first permanent Child Tax Credit (CTC), becoming the 16th state with a state CTC. Arizona, New Jersey, and Utah expanded their existing CTCs, while Oregon and Washington strengthened their state Earned Income Tax Credits (EITCs).

Maine, New York, and Vermont enhanced childcare and property tax credits to provide additional support for families. And Maryland authorized county autonomy to create local CTCs, opening the door for new local CTCs down the road.

Figure 1

A common thread among the states pursuing the most significant tax credit expansions – Rhode Island, Washington, Oregon, Maine, and Vermont – is that they were made possible by preserving or generating new revenue elsewhere. New or expanded tax credits in Rhode Island, Washington, and Maine were achieved as part of tax packages that also raised tax rates on high-income individuals. Meanwhile, lawmakers in Oregon, Vermont, and elsewhere pursued these credits for families and children while at the same time declining to double down on top-heavy tax cuts found in last year’s federal tax bill. These choices gave lawmakers the resources and flexibility to invest in children, families, and communities while improving the equity of their tax codes.

State Tax Credit Action This Year

Rhode Island’s new CTC is refundable, providing up to $330 per child. The full credit is available to all children 18 and under in families with income below $88,500 (single) and $110,640 (married). The credit begins to phase out for incomes above those amounts.

New Jersey lawmakers approved an across-the-board 25 percent increase to the state’s CTC, boosting the maximum credit to $1,250 for the lowest-income Garden Staters (families earning under $30,000 a year). Overall, the credit is available to families with children under 6 with annual incomes below $80,000.

Utah and Arizona improved their limited, nonrefundable CTCs by expanding eligibility thresholds (in Utah) and by boosting the credit amount from $100 to $125 (in Arizona).

Washington and Oregon enhanced their state Earned Income Tax Credits (EITCs). In Washington, lawmakers doubled the reach of the Working Families Tax Credit to an additional 460,000 households, thanks to new revenue from the state’s millionaires’ tax. In Oregon, lawmakers increased the state’s EITC to 14 percent for individual filers and 17 percent for filers with a child under 3, from 9 and 12 percent, respectively.

Elsewhere, New York enhanced the state’s Child and Dependent Care Credit, Maine strengthened its refundable Property Tax Fairness Credit, and Vermont expanded its property tax circuit breaker known as the Education Property Tax Adjustment and provided a one-time boost to the state’s renter’s credit.

The District of Columbia was poised to permanently reinstate and expand its first fully funded Child Tax Credit, a refundable $ 1,000-per-child credit, and speed up the increase to its EITC from 85 percent to 100 percent of the federal credit. But Congress got in the way. The District passed legislation to decouple from several 2025 federal tax law changes and used the saved revenue to pay for these tax credit improvements. Then the U.S. Congress tried to override the District’s law, although many observers note that Congress failed to act within the required time frame. The uncertainty and accompanying federally driven slowdown in local revenue collections kept lawmakers from following through on debuting their new CTC and EITC enhancement, which together were estimated to reduce child poverty in the District by one-fifth.

Not every state action this year was a move to enhance state tax credits. In South Carolina, rather than boosting benefits for children and families, lawmakers instead paired top-heavy tax cuts and ultimate income tax elimination with a $200 cap on the state’s already limited, nonrefundable EITC, cutting the state’s investment in the credit in half. Luckily, the Palmetto State was the outlier.