Tax Basics

Below is a list of tax expenditure reports published in the states.

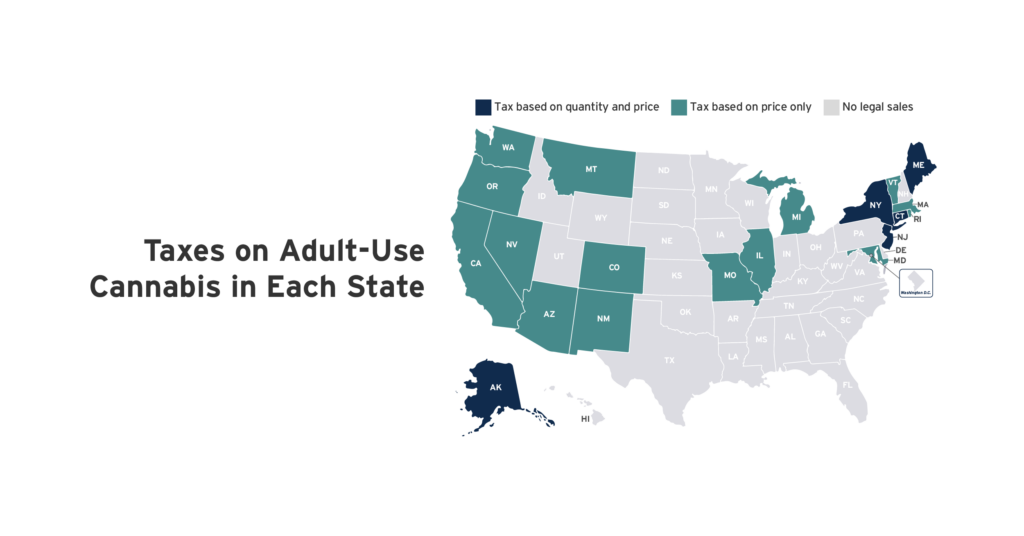

Twenty states have legalized cannabis sales for general adult use. Every state allowing legal sales applies a cannabis tax based on the product’s quantity, its price, or both. ITEP research indicates that taxes based on quantity will be more sustainable over time because prices are widely expected to fall as the cannabis industry matures.

As Tax Day approaches, it’s worth thinking about not only the taxes that we individually pay but the overall condition of our tax code as well. State tax codes, while perhaps less discussed than the federal system, are critically important. Depending on how they are designed, state taxes can improve or worsen economic and racial […]

State governments provide a wide array of tax subsidies to their older residents. But too many of these carveouts focus on predominately wealthy and white seniors, all while the cost climbs.

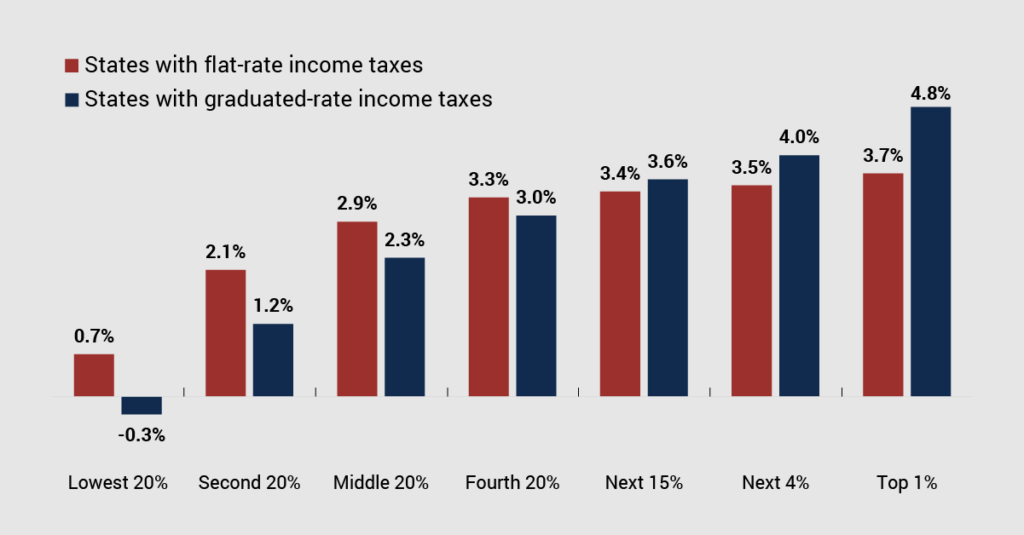

Flat taxes have some surface appeal but come with significant disadvantages. Critically, a flat tax guarantees that wealthy families’ total state and local tax bill will be a lower share of their income than that paid by families of more modest means.

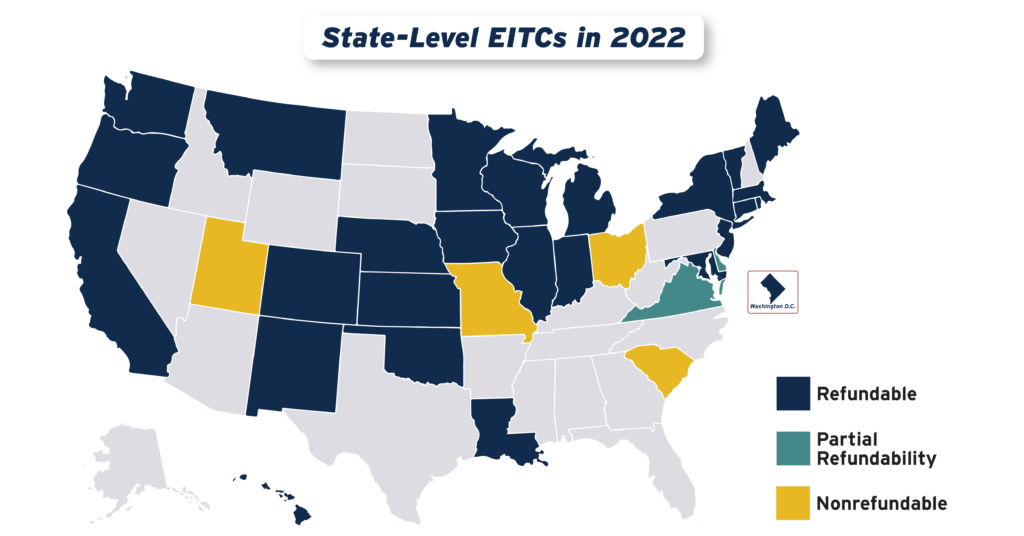

Boosting Incomes and Improving Tax Equity with State Earned Income Tax Credits in 2022

September 15, 2022 • By Aidan Davis

States continued their recent trend of advancing EITCs in 2022, with nine states plus the District of Columbia either creating or improving their credits. Utah enacted a 15 percent nonrefundable EITC, while the District of Columbia, Hawaii, Illinois, Maine, Vermont and Virginia expanded existing credits. Meanwhile, Connecticut, New York and Oregon provided one-time boosts to their EITC-eligible populations.

More States are Boosting Economic Security with Child Tax Credits in 2022

September 15, 2022 • By Aidan Davis

After years of being limited in reach, there is increasing momentum at the state level to adopt and expand Child Tax Credits. Today ten states are lifting the household incomes of families with children through yearly multi-million-dollar investments in the form of targeted, and usually refundable, CTCs.

Take a minute on this Tax Day to reflect on all that you survived, accomplished, and contributed to the collective good this past year, and be proud. There is always more work to be done to build the communities we desire, and paying your share is what allows that work to continue.

Fairness Matters: A Chart Book on Who Pays State and Local Taxes

March 6, 2019 • By ITEP Staff

There is significant room for improvement in state and local tax codes. State tax codes are filled with top-heavy exemptions and deductions and often fail to tax higher incomes at higher rates. States and localities have come to rely too heavily on regressive sales taxes that fail to reflect the modern economy. And overall tax collections are often inadequate in the short-run and unsustainable in the long-run. These types of shortcomings provide compelling reason to pursue state and local tax reforms to make these systems more equitable, adequate, and sustainable.

No Need for the MythBusters, the Millionaire Tax Flight Myth is Busted Again

May 1, 2018 • By Dacey Anechiarico

One of the most repeated myths in state tax policy is called “millionaire tax flight,” where millionaires are allegedly fleeing states with high income tax rates for states with lower rates. This myth has been used as an argument in state tax debates for years but Cristobal Young argues in his book, “The Myth of the Millionaire Tax Flight,” that both Democrats and Republicans are “searching for a crisis that does not really exist,” and that there is no evidence to support this myth.

Below is a list of notable resources for information on state taxes and revenues: Alabama Alabama Department of Revenue Alabama Department of Finance – Executive Budget Office Alabama Department of Revenue – Tax Incentives for Industry Alabama Legislative Fiscal Office Alaska Alaska Department of Revenue – Tax Division Alaska Office of Management & Budget Alaska […]

While it can be hard to look away from the important federal policy debates occurring right now in Washington D.C., state lawmakers across the country will also be debating consequential fiscal policy changes in 2017 that will deserve close scrutiny. The context of those debates will vary by state: from coping with major revenue shortfalls, […]

Fairness Matters: A Chart Book on Who Pays State and Local Taxes

January 26, 2017 • By Carl Davis, Meg Wiehe

When states shy away from personal income taxes in favor of higher sales and excise taxes, high-income taxpayers benefit at the expense of low- and moderate-income families who often face above-average tax rates to pick up the slack. This chart book demonstrates this basic reality by examining the distribution of taxes in states that have pursued these types of policies. Given the detrimental impact that regressive tax policies have on economic opportunity, income inequality, revenue adequacy, and long-run revenue sustainability, tax reform proponents should look to the least regressive, rather than most regressive, states in crafting their proposals.

For much of the last century, estate and inheritance taxes have played an important role in fostering strong communities by promoting equality of opportunity and helping states adequately fund public services. While many of the taxes levied by state and local governments fall most heavily on low-income families, only the very wealthy pay estate and inheritance taxes. Changes in the federal estate tax in recent years, however, caused states to reevaluate the structure of their estate and inheritance taxes. Unfortunately, the trend of late among states has tended toward weakening or completely eliminating them. But this need not be so;…

How State Tax Changes Affect Your Federal Taxes: A Primer on the “Federal Offset”

August 22, 2016 • By Dylan Grundman O'Neill

Read this brief in PDF here. State lawmakers frequently make claims about how proposed tax changes would affect taxpayers at different income levels. Yet too many lawmakers routinely ignore one important consequence of their tax reform proposals: the effect of state tax changes on their constituents’ federal income tax bills. Wealthier taxpayers in particular can […]

Indexing Income Taxes for Inflation: Why It Matters

August 22, 2016 • By Dylan Grundman O'Neill

Read brief in PDF here. All of us experience the effects of inflation as the price of the goods and services we buy gradually goes up over time. Fortunately, as the cost of living goes up, our incomes often tend to rise as well in order to keep pace. But many state tax systems are […]

Read the Report in PDF Form An individual savings account can serve as an emergency reserve – a financial cushion to sustain yourself in the event of an emergency. “Rainy day” funds are much like individual saving accounts, but on a statewide scale. Lawmakers use rainy day funds to set aside state tax revenue during […]

Major tax overhauls are on the agenda in a record number of states, and “Who Pays?” documents in state-by-state detail the precise distribution of state income taxes, sales and excise taxes and property taxes paid by each income group as of January 2013. It is a critical baseline against which future proposals can be measured. […]

Read the Report in PDF The 2015 Who Pays: A Distributional Analysis of the Tax Systems in All Fifty States (the fifth edition of the report) assesses the fairness of state and local tax systems by measuring the state and local taxes that will be paid in 2015 by different income groups as a share […]

STAMP is an Unsound Tool for Gauging the Economic Impact of Taxes

May 21, 2014 • By Carl Davis

The Beacon Hill Institute (BHI), a free-market think tank located at Suffolk University, frequently uses its State Tax Analysis Modeling Program (STAMP) to perform analyses purporting to show that lowering taxes, or not raising them, will benefit state economies. But STAMP suffers from a number of serious methodological problems and should not be relied upon by anybody seeking to understand the economic impacts of state tax policies.

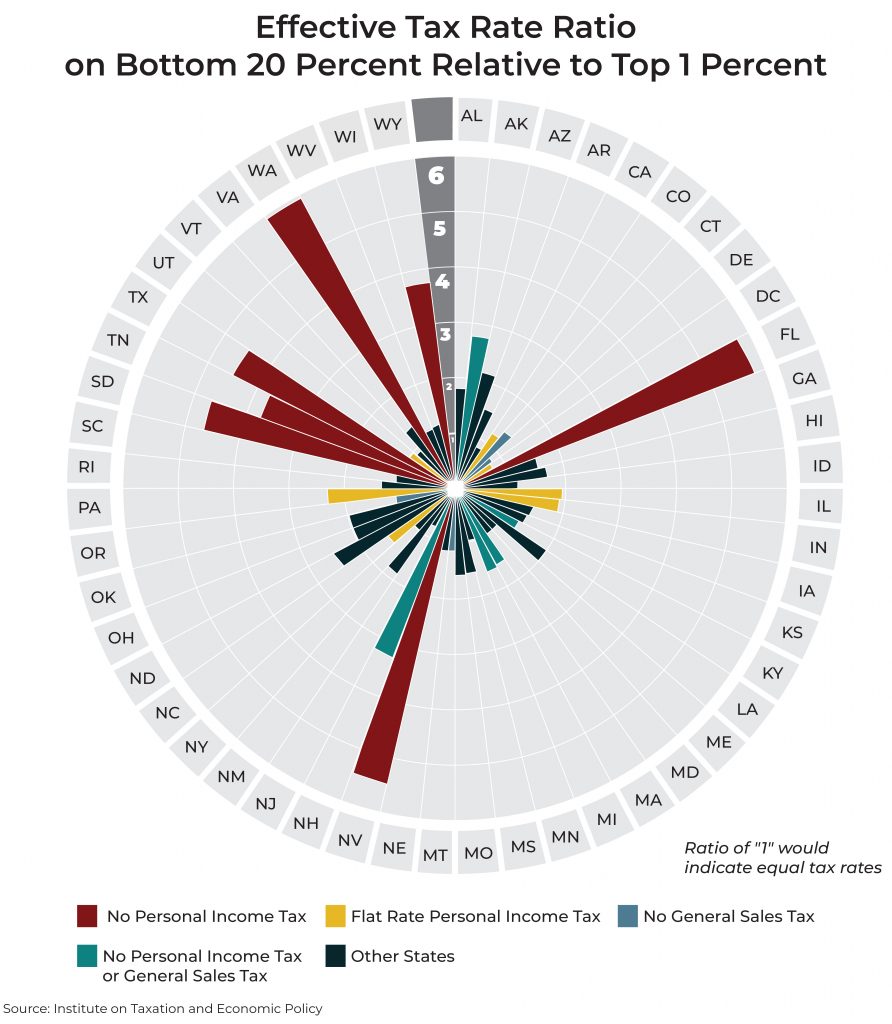

Annual state and local finance data from the Census Bureau are often used to rank states as "low" or "high" tax states based on taxes collected as a share of state personal income. But focusing on a state's overall tax revenues overlooks the fact that taxpayers experience tax systems very differently. In particular, the poorest 20 percent of taxpayers pay a greater share of their income in state and local taxes than any other income group in all but 10 states (including DC). And, in every state, low- income taxpayers pay more as a share of income than the wealthiest…

Colorado has become infamous for its Taxpayer Bill of Rights, or TABOR, a constitutional amendment restricting growth in revenue collections to an arbitrary "population-plus-inflation" formula. Although TABOR has had significant negative effects on Colorado's finances, similar proposals have surfaced in at least 30 states over the past decade. None of these proposals were approved, and in five states they were placed directly on a state-wide ballot where they were rejected by voters. Even in Colorado itself, citizens voted to suspend TABOR for five years in an effort to allow the s

Tax Expenditure Reports: A Vital Tool with Room for Improvement

August 14, 2013 • By Carl Davis

State and local tax codes include a huge array of special tax breaks designed to accomplish almost every goal imaginable: from encouraging homeownership and scientific research, to building radioactive fallout shelters and caring for "exceptional" trees. Despite being embedded in the tax code, these programs are typically enacted with tax policy issues like fairness, efficiency, and sustainability only as secondary considerations. Accordingly, these programs have long been called "tax expenditures." They are essentially government spending programs that happen to be housed in the tax code for ease of administration, political expedience, or both.

Tax incentives are intended to spur economic growth that would not have otherwise occurred. More specifically, these narrowly targeted tax breaks are usually offered in an attempt to convince businesses to relocate, hire, and/or invest within a state's borders.

States with “High Rate” Income Taxes are Still Outperforming No-Tax States

February 28, 2013 • By Carl Davis

Lawmakers in about a dozen states are giving serious consideration to either cutting or eliminating their state personal income taxes. In each case, these proposals are being touted as a way to boost economic growth.

These ITEP publications provide a broad overview of state tax systems as well as narrower information about specific state tax policies.

Institute on Taxation

and Economic Policy

ITEP is a non-profit, non-partisan tax policy organization. We conduct rigorous analyses of tax and economic proposals and provide data-driven recommendations to shape equitable and sustainable tax systems.

Subscribe to ITEP Emails

Tax research and policy news in your inbox.

Promote Fair Tax Policy

Your gift to ITEP promotes tax justice. With your help, we do research that supports taxing millionaires and billionaires, taxing big corporations and raising revenue for the things our people, our communities and our planet need.

Together, we can create a country with more economic justice, more racial justice, more climate justice… and more tax justice.