Key Takeaways

The next time Congress is serious about making the wealthiest pay their fair share in federal taxes, they will need to make three key changes to the federal corporate income tax so that it applies effectively to all the businesses that generate their income. Policymakers should:

- Establish a strong global minimum tax: Implement a minimum tax on corporations that meets and exceeds the standards of the global minimum tax that other countries are implementing.

- Subject certain “pass-through” businesses to corporate tax: Expand the corporate income tax to apply to large businesses that are currently structured to avoid it.

- Raise the corporate tax rate: Raise the corporate income tax rate on the largest companies to fully capitalize on the first two changes, which will have closed off the most common ways businesses avoid corporate tax increases.

Any progressive tax reform plan must be resilient, meaning it is designed to survive the ideological hostility, or even corruption, it will face from the Supreme Court and possible future presidents and Congresses. Policymakers can make tax reform resilient by taking the following steps:

- Prevent sabotage by the Supreme Court: While a comprehensive progressive tax reform plan will have many components, reforms to the corporate income tax must be included because they are far less likely to be overturned by ideological justices on the Supreme Court than proposals to tax the income and wealth of billionaires more directly. Unlike other types of taxes, the constitutionality of the federal corporate income tax has been generally uncontroversial and unchallenged.

- Prevent sabotage by a future president: It is currently unclear whether any legal remedy exists when the executive branch, in violation of the law, issues regulations and guidance cutting the taxes of corporations and the wealthy, as the Trump administration has already done repeatedly. Federal courts may determine that no one is sufficiently harmed to have standing to sue. To increase the odds of successful litigation to block the executive branch from illegally cutting corporate taxes, lawmakers should explore creating situations in which a party could demonstrate harm done to them by reduced corporate tax revenue and thus have standing to sue.

- Prevent sabotage by a future Congress: Negotiate with the Organization for Economic Cooperation and Development (OECD) to end the “side-by-side” system demanded by the Trump administration, which weakens the global minimum tax to benefit American corporations but not regular American people. Establish the original, stronger standards as the international norm that future Congresses will be reluctant to deviate from for fear of triggering the enforcement mechanisms of the global minimum tax.

Introduction

We cannot allow profitable corporations and extremely wealthy individuals in the U.S. to avoid paying taxes forever. Americans recognize that the wealthy should pay their fair share to support the society that makes their success possible. Large majorities of Americans regularly tell pollsters that both corporations and the uber-rich should be required to pay more, even as the current Congress and President have consistently worked to reduce what they pay.1

The Institute on Taxation and Economic Policy has long argued that the U.S. needs to reform its tax code to raise more revenue and to be more progressive, taxing larger shares of income of those most able to pay.2 In addition to those two goals for tax policy, we now must add a third: resilience. For a policy to be resilient, it must be designed to survive the ideological hostility, or even corruption, it will face from the Supreme Court and, as much as possible, hostile future Congresses and presidents.

Adding this third element to the progressive policy agenda requires a shift in thinking. There are essential elements of the progressive tax agenda that ITEP has advocated for, such as subjecting unrealized capital gains of the billionaires to the income tax or taxing wealth itself, that lack resilience in the altered legal and political environment that we face today. This does not mean that they should be abandoned. It does mean that the agenda should be expanded to include more resilient proposals. We cannot afford to spend the enormous amount of political capital and go through the lengthy legislative process required for progressive tax reform, only to have it overturned by a hostile Supreme Court or easily sabotaged by a future president or Congress.

The next time policymakers supportive of progressive tax reform control Congress and the White House, what should they do, given the hostility of the Supreme Court and the uncertainty about future Congresses and presidents?

The answer begins with the fact that most income flowing to the wealthiest Americans is generated by business entities that are, or could be, subject to the federal corporate income tax. A reformed corporate income tax could effectively target the income that eventually flows to the wealthy at its source. As this report explains, well-designed corporate tax reforms would also be more resistant to being blocked, weakened, or undone than current proposals to tax wealth or income from wealth. The latter are well worth enacting, but a more robust federal corporate tax would ensure that most of the income flowing to the wealthiest Americans is taxed before it reaches them and would have the resiliency that is now required.

A president and a congressional majority supportive of progressive taxes could significantly strengthen and expand the corporate tax with a few important reforms.

- First, lawmakers should subject corporations to a robust minimum tax, one that meets and exceeds the standards of the global minimum tax that 65 countries, including most of the world’s major economies, are now implementing.

- Second, they should expand the reach of the corporate income tax to apply to large pass-through businesses that have all the relevant attributes of taxable corporations but are currently not taxed.

- These two reforms would in turn facilitate a third reform, an increase in the corporate income tax rate for the largest companies.

Together, these reforms would ensure that most of the income flowing to the wealthiest Americans is taxed before it reaches them. While many other changes are needed in our tax code, these proposals could form the most important building blocks of effective progressive tax reform.

This does not mean that lawmakers should not pursue other tax reforms. Rather it means the proposals described here should be considered an indispensable component of the reform agenda because other tax proposals affecting the very wealthy may be sabotaged in the future by any of the three branches of government.

The Risk of Sabotage

Each of the branches of government pose different challenges for the resilience of progressive tax policy.

Judicial Branch

A majority of the justices on the Supreme Court today are ideologically hostile to many tax reform proposals. Four justices indicated last year that they might strike down a proposal to tax the unrealized capital gains of billionaires if it were enacted.3 The other two Republican-appointed justices were silent on the issue and only one of their votes would be needed to strike down the policy. This speaks not just to the vulnerability of that specific proposal but of an entire class of progressive tax proposals.

Executive Branch

Trump’s Treasury officials have regularly usurped Congress’ legislative power by unilaterally cutting taxes. Starting during the first Trump administration, the Treasury Department issued regulations interpreting tax statutes in ways that essentially ignored limits placed by Congress on tax breaks from the 2017 tax law.4 During his second term, Treasury is advancing regulations that weaken corporate tax increases enacted under Biden.5

It is unclear if any legal mechanism could stop the executive branch from issuing regulations or taking other actions that reduce taxes, even when this violates statutes enacted by Congress and thus violates the Constitution. Federal case law is ambiguous on this point, but some legal precedents might be interpreted to suggest that no potential plaintiff is sufficiently, specifically harmed by illegal reductions in taxes to have legal standing to sue the federal government.

Legislative Branch

The most obvious way that a tax policy can be sabotaged after enactment is for a new Congress (and president) to repeal it. Certain parts of 2022’s Inflation Reduction Act (IRA) – such as its tax breaks for green energy – were limited or repealed by the so-called One Big Beautiful Bill Act (OBBBA) enacted this summer. OBBBA’s tax cuts have more than offset the revenue that the IRA raises from corporations and the wealthy.6

Sometimes the legislative branch can sabotage a reform even when the president is of the opposing party. An example is the successful drive by Congressional Republicans to partly defund the IRS. The IRA restored some of the funding for tax enforcement that had been slashed over the previous decade. The CBO estimated that this would result in a net revenue increase of more than $100 billion over a decade (others had much higher estimates).7 Even before Biden left the White House, Congressional Republicans began to whittle this funding away during appropriations negotiations. Now that funding, which was meant to last 10 years, is essentially gone.8

Resilient Policy Solutions

A wide set of reforms going far beyond tax policy is needed to address the existential challenges to the country. That said, tax policy is a crucial part of restoring democracy and there are specific tax policy choices that will be essential when those favoring progressive reform regain control of Congress and the presidency.

As the rest of this report explains, corporate tax reforms can be far more resilient than other types of tax reforms and can be designed to achieve many of the same objectives.

Tax reforms are less likely to be blocked by the Supreme Court if they rely on the corporate income tax. The Court has never limited Congress’ power to tax corporations the way it has limited Congress’ power to tax individuals directly.9 Even before ratification of the 16th Amendment, which empowered Congress to tax personal income, the courts justified a federal tax on corporate income as a federal excise tax on the privilege of operating through a corporation, which is clearly within Congress’ power under the Constitution.

Corporate tax reforms could be more resilient to sabotage by a future President if Congress creates a situation where a party can demonstrate how it is harmed by a regulation or guidance cutting corporate taxes and thus is more likely to have standing to sue to block it. For example, Congress could provide some party (such as state governments or a specific group of individuals) with a benefit that is funded by corporate tax revenue and which would be diminished any time the executive branch takes action that reduces corporate tax revenue. This or a similar arrangement may increase the likelihood that federal courts would allow a case to challenge the regulation.

Corporate tax reforms can also be more resilient to sabotage by a future Congress if the U.S. works to reinstate the global minimum tax agreement with governments around the world in its original, stronger form, without the special provisions that the Trump administration demanded to weaken it. Under the global minimum tax as originally conceived, if the U.S. or any other government attempts to cut taxes of its corporations below a certain level, participating governments will step in and collect additional taxes on those corporations’ operations within their borders, likely neutralizing the tax cut the companies would have received from their own government. If the U.S. helps make the global minimum tax an established part of the international tax system, it will be difficult for any single government to unravel it.

The Fundamental Problem: Very Well-Off Americans Do Not Pay Taxes in Proportion to Their Ability to Pay

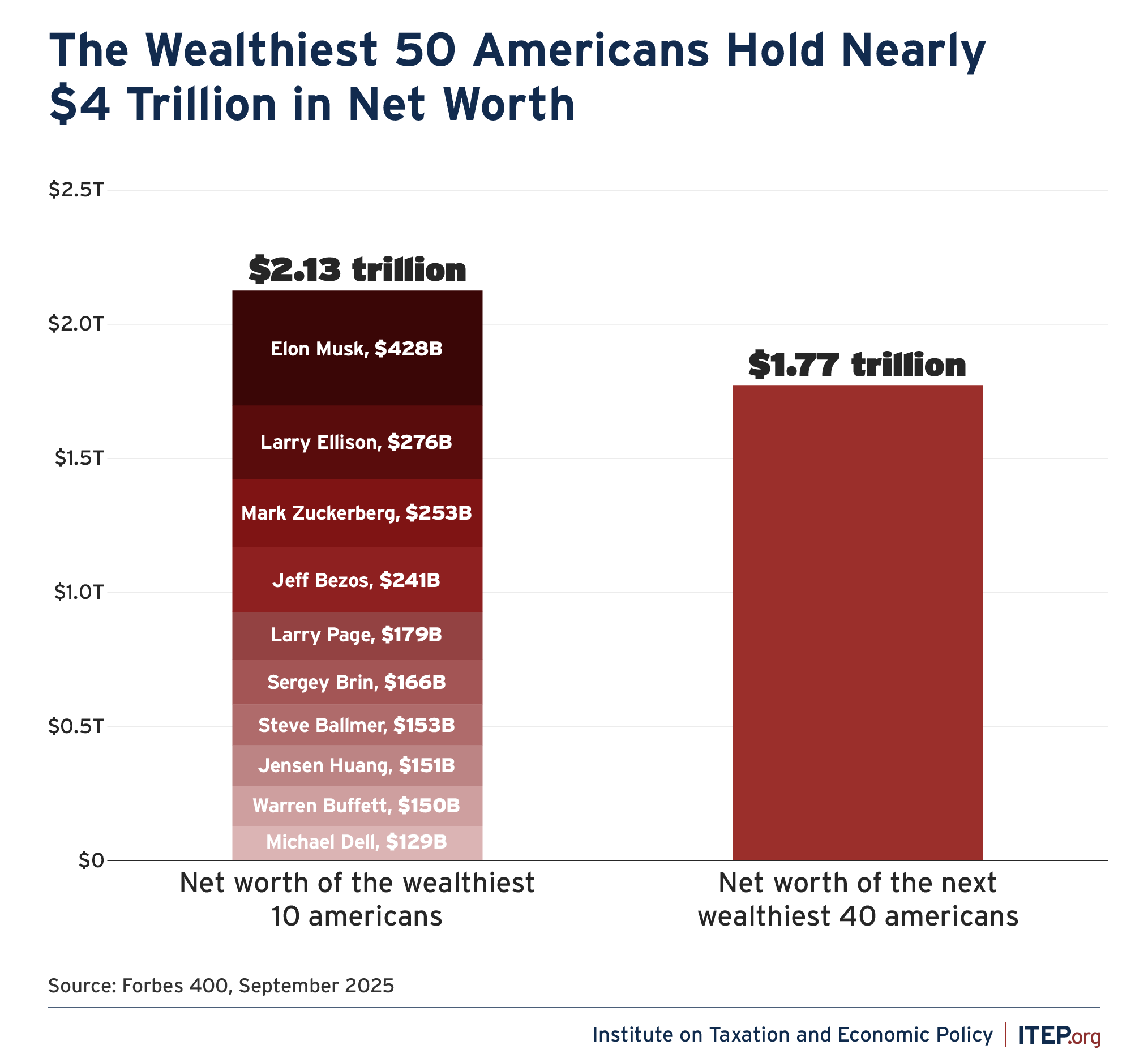

If the U.S. is ever to have a tax code that raises more revenue and is more progressive, it must address one problem above all others: the ability of very wealthy Americans to receive income in the form of “unrealized” capital gains that is not taxed. At its worst, this allows billionaires such as Elon Musk, Mark Zuckerberg, and Jeff Bezos to arrange their affairs to receive their income as unrealized gains, which are generally not taxed, rather than as wages and salaries which are taxed every year.10 Unfortunately, many of the proposals discussed in recent years to address this are very vulnerable to challenge at the Supreme Court and subject to sabotage by a future President and Congress.

If a person’s net worth increases from $1 billion to $3 billion over the course of a year, an economist would say that person must have had income of at least $2 billion. However, if this income is in the form of an increase in the value of assets owned at both the start and end of the year, it is considered unrealized capital gains. Under current personal income tax rules, unrealized capital gains are usually not considered income.

ProPublica reported that from 2014 to 2018, Jeff Bezos’s net worth increased by $99 billion but the income he reported to the IRS during that period was a little more than $4 billion.11 A simple definition of income that includes any increase in the ability of a person to buy something would suggest that Bezos had income of at least $99 billion during this period. But he paid income tax on a tiny fraction of that amount because most of it was unrealized capital gains.

In theory, wealthy people with unrealized capital gains could eventually pay taxes on this income if they sell their assets and “realize” the gains as profits on the sales. But many extremely wealthy people avoid this completely. They can often obtain whatever cash they need without selling assets because they have access to almost limitless credit. To avoid paying income tax on their gains, they can hold onto their assets and borrow at very low rates to finance their lifestyle, no matter how lavish.

Very wealthy people can hold onto their assets (and thus defer realizing income and defer paying tax) until they die, at which point the mother of all breaks takes over. All those unrealized capital gains simply disappear as far as the tax code is concerned. Even if their heirs choose to sell the assets, they only pay tax on the gains (the rise in the price of the stock or other assets) from the time they inherited them.12

The failure of the tax code to ever tax these massive amounts of income that accrue to the very wealthy is the single biggest reason the tax system fails to adequately tax the nation’s most well-off.

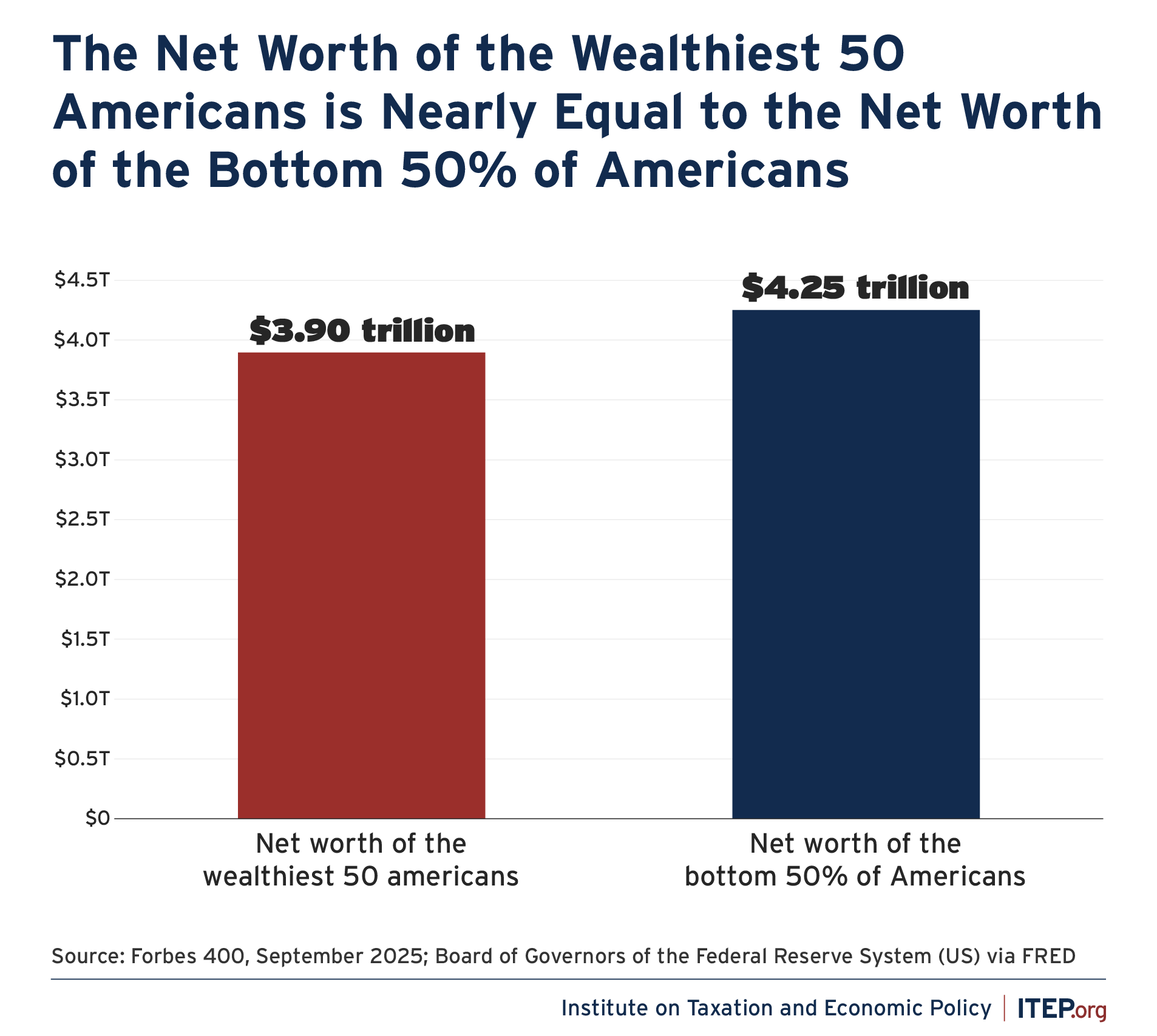

Figure 1

Figure 2

One solution is to reform the personal income tax so it does apply to the unrealized gains received by the very wealthy. Sen. Ron Wyden has sponsored a bill, which Reps. Beyer and Cohen sponsored in the House, to tax most unrealized capital gains of extremely wealthy people each year.13 It would apply only to taxpayers who have either income exceeding $100 million or net worth exceeding $1 billion for three years straight.

For publicly traded stocks that have an easily discerned market value, individuals subject to this provision would pay income tax on the unrealized gains (the rise in the value of stock held) each year. This approach is also called “mark-to-market” taxation.

For assets that are more difficult to put a price tag on (like a privately held business that has not changed hands in decades), the owner could continue to defer paying tax on the gains until they sell the asset. At that point the income tax due on the gains would be increased in a way that offsets the benefit of the tax deferral. This would have a result roughly similar to mark-to-market taxation.

Another solution is for the federal government to tax the wealth (the net worth) of the best-off Americans in addition to their income. This report will use the term “wealth tax” to mean a tax that is calculated as a percentage of an individual’s or household’s net worth. Starting in 2019, Senator Elizabeth Warren, along with others, has proposed to enact a federal tax on the net worth of the very wealthiest Americans.14

These proposals – taxing unrealized gains and taxing net worth – are different approaches but would address the same problem: the fact that the wealthiest do not pay taxes at any level remotely commensurate with their ability to pay.

Avoiding Potential Sabotage by the Judicial Branch

While both these approaches would be huge advances for tax fairness, they face a significant hurdle: the U.S. Supreme Court. A federal wealth tax would face enormous headwinds with the Supreme Court as it is currently comprised and is likely to be comprised for many years to come. A tax on unrealized capital gains would also face a significant threat from a constitutional challenge.

The history of the Supreme Court’s rulings on Congress’ taxing powers is one of the most bizarre areas of constitutional law. It hinges on the question of what the term “direct” tax means in the Constitution. Two different parts of the Constitution describe how Congress can impose a direct tax, without defining the term. One explains that direct taxes must be apportioned among the states based on population (meaning the total amount paid by each state would be the same per capita), but with each enslaved person counting as three-fifths of one person. The other requires that if a direct tax is imposed it must be in proportion to population as determined by a census or “enumeration.”

The direct tax clauses of the Constitution are part of the infamous Three-Fifths Compromise.15 The drafters themselves seemed unclear about what taxes might be described as “direct” but included the language as part of the compromise that would allow slavery to continue under the new Constitution.16

Starting with the 1796 case Hylton v. United States, the Supreme Court dealt with this uncertainty by ruling that a direct tax was any tax that could reasonably and sensibly be apportioned by population. (A head tax is one clear example, and the drafters believed that a tax on real estate alone was also a direct tax.)

In this reading, the point of these constitutional provisions was simply to specify how such a tax should be apportioned: according to a census and counting each enslaved person as three-fifths of a person. The point was not to impose an apportionment requirement on a vast category of taxes.

In Hylton, the Court held that a federal tax on carriages was not a “direct” tax. Because carriages were owned mainly by the wealthy, one might think of this as something like a tax on yachts or luxury cars today. The Justices who ruled on the case had been involved in drafting and ratification of the Constitution.

In subsequent cases, the Supreme Court applied this reasoning and allowed Congress to enact various taxes without apportioning them by population for a century. During this period, the Supreme Court would likely have allowed a federal tax on individuals’ wealth or on income (including unrealized capital gains) without much hesitation.

By the late 1800s, one would think that the direct tax clauses of the Constitution were even less relevant because their entire motivation – preserving slavery – had become irrelevant. In 1895, however, a right-wing Supreme Court ignored the precedents of the previous century and dramatically changed course in Pollack v. Farmers’ Loan and Trust Company. In a decision that was immediately criticized by legal scholars,17 a majority ruled that a personal income tax is a “direct” tax and therefore could not be enacted without being apportioned by population.

Apportioning a personal income tax by population would be convoluted, counterproductive to the very goal of tax fairness, and nearly impossible to implement. For example, a state with 5 percent of the nation’s population would be required to pay 5 percent of the income tax even if this state has only 1 percent of the nation’s income. The Pollack ruling killed the federal personal income tax.

The ruling so outraged the public that the nation took the extraordinary step of adding the 16th Amendment to the Constitution in 1913 to expressly grant Congress the power to tax income without the restrictions imposed by the direct tax clauses.

Some future Supreme Court decisions backed away from the reasoning of Pollack and narrowed its relevance, but it was never overturned and today provides a precedent that could be easily used by a court predisposed to strike down a federal tax on wealth. ITEP has explained why this reasoning is wrong, but there is a good chance that the Republican-appointed majority on the Supreme Court would see it differently.18

Beyond the wealth tax, a new federal tax on unrealized capital gains would also be at great risk. The most logical way to view unrealized gains is that they are income, and Congress has the authority under the Constitution to tax them. However, four justices on the Supreme Court indicated last year that they might strike down a federal tax on unrealized gains premised on the idea that they are wealth, not income, until they are realized.19

Other Personal Income Tax Proposals May Be More Resilient in the Face of a Hostile Judiciary

Not all progressive reforms to the federal personal income tax are in danger from the Supreme Court. Several bills introduced in Congress would make important reforms to the personal income tax that lawmakers can support without worrying at all about raising constitutional issues.

For example, Rep. Delia Ramirez’s Equal Tax Act would tax unrealized gains when a wealthy person dies and passes assets onto their heirs.20 The Supreme Court is unlikely to strike this down given that longstanding precedents give Congress deference to tax transfers of income and wealth (as with the estate tax, which has been in effect for more than a century in its current form).21 The Equal Tax Act includes other important reforms, among them removing the provision taxing most realized capital gains at lower rates than other types of income for high-income people.

As is true of every tax proposal, this one alone will not solve all problems in the tax code. Even if the Equal Tax Act was enacted to tax unrealized gains of the wealthy eventually, they would still receive an enormous benefit from putting off paying taxes on a huge part of their income for years or decades during their lives. Over time, this makes a significant difference. A decade ago, one analyst calculated that Warren Buffett would have been worth $9.5 billion if his capital gains were taxed every year regardless of whether he sold his assets, just as the salaries and wages of most Americans are taxed. But the tax break provided by deferral of income tax on unrealized capital gains resulted in his vastly greater net worth of $70 billion at that time.22

While taxing gains of very wealthy people upon their death is very important, it will not immediately change anything for most billionaires, who will have years to lobby Congress to reverse this reform before it touches their accumulated wealth.

There are, however, less vulnerable approaches. Most of the income flowing to the wealthiest Americans is generated by business entities that are, or could be, subject to the federal corporate income tax. Taxes imposed on this income at the point where it is generated by a business are more likely than other taxes to survive in the face of a judiciary ideologically biased against new types of taxes.

The narrow interpretation that federal courts have applied to Congress’ taxing power under the constitution generally relates to taxes imposed on individuals and not taxes imposed on corporations. The Supreme Court’s right-wing turn in its 1895 Pollack decision to restrict Congress’ power to tax was never applied to federal taxes on corporate income.

In Flint v. Stone Tracy Company, the Supreme Court in 1911 upheld the federal corporate income tax, justifying it as an excise tax paid for the privilege of operating as a corporation. Congress’ power to impose excises is clear under the constitution. The justification for an excise on corporations is especially strong because corporations – and the benefits they come with, such as limited liability and the ability to be publicly traded – are creations of government.

The way to fully tax the currently untaxed income of the wealthy in a way that is likely to survive judicial scrutiny is to tax it at its source. This means taxing the profits of the businesses that they own with a strong corporate income tax.

Avoiding Potential Sabotage by the Executive Branch

We increasingly face the possibility of a president acting unilaterally to sabotage our tax code as President Trump has during his two terms in office. The first and second Trump administrations have used regulatory power to provide tax cuts that are arguably not even allowed in statute. There is no obvious limit to the executive’s ability to do this even when it is clearly illegal. When Treasury fails to adequately enforce tax laws, it is possible that no one who has standing to sue the government because federal courts may not recognize that anyone has suffered a direct injury merely because others pay less taxes than Congress intended.

Executive Branch Sabotage of the Tax System During the First Trump Administration

Following the passage of Trump’s 2017 tax law, the Treasury Department issued regulations implementing its provisions in ways that provided more tax breaks than any reasonable interpretation of the statute would warrant. Many of the regulations relate to capital gains or other types of income that flow mostly to the richest Americans.

Tax law professor Rebecca Kysar described several examples during Congressional testimony in 2020:23

- The 2017 law provided various capital gains tax breaks for assets invested in designated “Opportunity Zones.” One way that investors could meet the law’s requirements was to “substantially improve” property in an Opportunity Zone, which was defined as “addition to basis,” a term long used in tax law to refer to permanent improvements in property like replacing a roof on a building. The Treasury Department created a definition of this term that included buying linens, mattresses, furniture, and gym equipment.

- The 2017 law also provided a 20 percent deduction for “qualified business income” reported on individual income tax returns and subject to the personal income tax. The statute defined qualified business income to specifically exclude “financial services.” In common English, that means banks cannot take the deduction. And yet, under the Treasury Department’s regulations, taking deposits and making loans (what most of us would call “banking”) are not considered “financial services.”

- The 2017 law also barred the deduction for businesses whose principal asset is the “reputation or skill” of the owners or employees. But the examples provided by Treasury clearly indicate that a celebrity chef’s restaurant profits would qualify for the deduction. It is difficult to imagine an enterprise based more on reputation or skill than a celebrity chef’s restaurant.

The Trump administration also almost certainly exceeded its statutory authority with the regulations it issued to implement the 2017 law’s corporate tax provisions. This included a major loophole that the Treasury Department created for certain banks to completely avoid a provision that was supposed to block tax avoidance. That provision, the Base Erosion and Anti-Abuse Tax (BEAT), was supposed to stop foreign corporations from using interest payments and other payments from their U.S. subsidiaries to strip profits out of the country. Foreign banks like Credit Suisse and Barclays persuaded Treasury to create an exception, not mentioned anywhere in the statute, for the interest foreign banks pay on loans to their U.S. subsidiaries to meet the requirements of federal banking regulation. Officials at the Joint Committee on Taxation reportedly said this exception created by Treasury could cost $50 billion over ten years.24

Executive Branch Sabotage of the Tax System During the Second Trump Administration

The Inflation Reduction Act that President Biden signed into law in 2022 includes a Corporate Alternative Minimum Tax (CAMT) that is supposed to ensure that very profitable corporations pay federal income tax of at least 15 percent of the profits they report to investors, with certain exceptions.

The Treasury Department recently proposed regulations to limit the CAMT’s impact on cryptocurrency companies, energy companies, and private equity firms. Even business-friendly tax experts say these limits far exceed any reasonable interpretation of statute.25 This amounts to an unconstitutional power grab by the executive branch and the courts are unlikely to do anything to prevent it given that no party can claim to be injured in any particular or concrete way by it.

There is no end in sight to this administration’s unchecked campaign to unilaterally cut corporate taxes by weakening CAMT. In the months following the passage of the One Big Beautiful Bill Act (OBBBA) in the summer of 2025, some corporations complained that OBBBA’s benefits to them would be less than they initially expected because the CAMT limits those benefit in some cases.26 Corporate lobby associations pushed the Treasury Department for regulations that would provide exceptions to the CAMT with no real statutory justification at all.27

How to Rein in the Executive Branch: Give Someone Standing to Sue When the Administration Violates Tax Law to Cut Corporate Taxes

Caselaw regarding standing is opaque. Some legal scholars have long doubted that anyone has standing to sue to block regulations that reduce tax liability. Others have argued that precedents exist that would facilitate suits by a Congressional majority opposing the regulations or by other parties that arguably are harmed by them.28

Congress can reduce, if not eliminate, this uncertainty and increase the odds that a suit to block such regulations would be allowed to proceed. For example, a future president and Congress willing to enact a corporate tax increase could include in the legislation a provision dedicating a percentage of all federal corporate income tax revenue to a specific entity so that this entity likely has standing to sue whenever the Treasury Department attempts to reduce corporate taxes below what the law allows.

One possible variation of this could require that some percentage of all corporate tax revenue be provided to state governments to be used for infrastructure spending. If the Treasury Department subsequently issues regulations that allow corporations to pay less than specified under any provision of federal income tax law, any of the state governments might then have standing to sue in in federal court to block these regulations because they reduce the infrastructure funding that states receive. Alternative examples of this concept might dedicate a percentage of corporate income tax revenue to some other party (besides states) who would be likely to sue the federal government when Treasury regulations harm their interests.

Avoiding Potential Sabotage by the Legislative Branch

Of course, any tax law can be eliminated by Congress and a future president. Nevertheless, there is a progressive corporate tax policy that would be harder to undermine: U.S. adoption of the Global Minimum Tax (GMT) and elimination of the “side-by-side” agreement that the Trump administration demanded to largely exempt tax avoidance by American corporations. Full implementation of the GMT as originally envisioned and as most of the governments of the world’s largest economies have already begun, would require an act of Congress. Elimination of the side-by-side agreement would be easily accomplished as none of the parties outside of the U.S. wanted it in the first place.

As explained below, the GMT has specific features that would make it very difficult for any single government (even one as powerful as the U.S. government) to abandon it once it is a firmly established part of the international tax system. At that point, any attempt by the U.S. government to reduce the effective tax rate paid by the largest multinational American corporations below a certain level would be neutralized by tax increases imposed in other countries where U.S. companies have operations.

Raising Revenue from the Corporate Income Tax

The income of the wealthy would be adequately taxed if the businesses that generate their income were subject to a well-functioning corporate income tax. Sadly, we do not have one right now.29 The OBBBA makes the federal corporate income tax even less effective.30 Congress can remedy this by taking three important steps:

- Impose a powerful minimum tax on American corporations that is more effective than the existing provisions that operate as minimum taxes to varying degrees. This would be accomplished with legislation that broadly implements the global minimum tax that governments around the world have begun to implement.

- Expand the reach of the corporate income tax to many businesses that currently are subject to the personal income tax but not the corporate income tax—so-called “pass-through” business entities.

- Raise the corporate income tax rate for the largest companies.

Enact an Effective Minimum Tax for American Corporations

In 2021, after several years of negotiations among member nations of the Organization for Economic Cooperation and Development (OECD), 137 governments that account for about 95 percent of global economic output agreed to a framework to create a global minimum tax.31 Full implementation of this framework requires an act of Congress and is the best hope for blocking the types of tax avoidance that have weakened corporate income taxes all over the world. Some features of the global minimum tax (GMT) would, once it is firmly established, make it difficult for any one government to ignore or weaken it.

Since Trump returned to the White House, the U.S. pressured the most powerful participants (the G7 countries) to carve out an exception for U.S. corporations that would essentially leave their tax avoidance practices unchallenged.32 If the next president and Congress return to the original vision of the global minimum tax and enact legislation to broadly meet its terms, the GMT could meet its potential. Once a fully functioning GMT is operational for a few years, it is far less likely that other governments would ever weaken it again – even if another U.S. Congress and president in the future oppose it.

The framework of the global minimum tax requires each participating country to ensure three things:

- Any corporation’s profits generated within its borders (whether profits of a domestic company or foreign company) are taxed at an effective rate of at least 15 percent.

- Its own corporations pay an effective tax rate of at least 15 percent on their offshore profits in each country where they do business. If they do not, the participating country that is home to the corporation in question would impose a tax on top of whatever foreign taxes are paid to ensure this result.

- The profits of foreign multinational corporations earned within their borders will be subject to additional taxes if necessary to address effective tax rates they pay in other countries that are less than 15 percent when those corporations’ own governments are not complying with the GMT to ensure this result.

Below is more detail on each of these components of the GMT.

First, a participating government must ensure that any corporation’s profits generated within its borders (whether profits of a domestic company or foreign company) are taxed at an effective rate of at least 15 percent. If the country’s regular, existing tax rules fail to accomplish this, under the global minimum tax framework it will impose a Qualified Domestic Minimum Top-Up Tax (QDMTT), an additional tax to bring the effective rate to 15 percent. The U.S. has a 15 percent minimum tax (known as the corporate alternative minimum tax, or CAMT) enacted as part of the Inflation Reduction Act. This minimum tax is helpful but insufficient. Unlike a QDMTT as originally envisioned, the CAMT applies to the total worldwide profits of affected corporations. This means that if a company pays effective rates higher than 15 percent in other countries, it could pay less than 15 percent on its U.S. profits. In addition, the CAMT applies to a much more limited group of corporations (about 150 corporations with profits exceeding $1 billion over three years) than does the global minimum tax (some 1,600 corporations with revenues exceeding $860 million a year).33

Second, a participating government must ensure that its own corporations pay an effective tax rate of at least 15 percent on their offshore profits in each country where they do business and, if necessary, impose a tax on top of whatever foreign taxes are paid to ensure this result. The global minimum tax framework refers to this as the Income Inclusion Rule (IIR). As explained below, the No Tax Breaks for Outsourcing Act, which was recently reintroduced in Congress, would move U.S. tax rules in this direction. The U.S. currently has provisions that somewhat serve as a minimum tax on offshore profits, but they are not nearly effective enough to comply with the global minimum tax framework, as explained in detail in the appendix.

Third, participating governments must ensure that even multinational corporations based in countries that are not participating in the global minimum tax will ultimately pay an effective rate of at least 15 percent on their profits in each country where they do business. The global minimum tax framework accomplishes this with an Undertaxed Profits Rule (UTPR) calling on participating governments to respond by imposing additional taxes on the profits these companies generate in their borders to offset their ability to pay effective rates of less than 15 percent in other jurisdictions. The Biden administration offered proposals to accomplish this.34

Once the global minimum tax is firmly established, its structure would make it difficult for any one government (even the U.S. government) to change its laws or regulations in ways that would otherwise allow corporations to pay effective tax rates of less than 15 percent. Any attempt by the federal government to allow American corporations to pay less could be met by tax increases imposed by other governments on the operations of U.S. companies within their borders (tax increases imposed through the IIR or UTPR), thus neutralizing the tax break that the federal government intended to provide.

The appendix explains in detail why the U.S. needs the global minimum tax and why existing U.S. laws fail to address the same problems.

Expand the Reach of the Corporate Income Tax to Include All Large Companies that Operate Like Corporations

Generally, a business is organized as either a “C corporation,” which is subject to the corporate income tax, or a pass-through entity, which is not. While much of the income flowing to the wealthiest people is corporate profit subject to the corporate income tax, the wealthy also receive a lot of income from pass-through businesses. For these enterprises there is no tax at the business entity level. Ostensibly, their profits are “passed through” straight to the individual owners and reported on their personal income tax returns. Large pass-through companies, however, are nearly impossible for the IRS to audit and are notoriously adept at ensuring that their owners avoid tax.

For example, the Trump Organization is really a web of more than 500 entities that are all or mostly pass-through companies and it is unclear that the IRS would be able to understand how it functions (even an IRS that was adequately funded and interested in investigating the Trump Organization35 ). To achieve the goal of effectively taxing the income of the wealthy, Congress must expand the reach of the corporate income tax to apply to the types of pass-through companies owned by the wealthy.

In the past, people who wanted the benefits of incorporation paid for them through the corporate income tax. If businesspeople wanted to limit their personal legal liability for the debts and obligations of their enterprise, or they wanted to trade their company on a public exchange, they asked the government (at the state level typically) to grant them these favors by allowing them to create a corporation. In return, among other obligations, the business would pay a corporate income tax at the state or federal level.

Over time, state governments and the federal government facilitated the creation of business entities that had limited liability without paying the corporate income tax. In 1987, Congress even allowed companies traded on a public exchange to not pay corporate income tax in certain situations.36 Originally, these privileges were intended for smaller businesses, but the trend has been to extend them to larger and larger enterprises. This trend picked up in the 1980s and 1990s, when more very large companies had the traditional attributes of corporations but were structured as pass-through businesses and thus not subject to the corporate income tax.

To be sure, there are still plenty of pass-through entities that are small businesses. The archetypical example might be a painting business owned by two brothers and staffed by them and their families, or a law firm made up of a handful of attorneys. But today, pass-through businesses also include massive entities like Bechtel and Bloomberg.37

Given that many of these entities have the salient features of C corporations, several tax experts and analysts have suggested that some of these companies should be subject to the corporate income tax. One approach would be to treat any business as a C corporation for tax purposes if it has limited liability or is publicly traded, with exemptions for small and medium-sized businesses.38

Raise the Corporate Income Tax Rate

The two business tax reforms just described – ensuring that corporations pay meaningful tax on their profits in each country where they operate and requiring all large businesses to actually pay the corporate income tax – would block the main exits that businesses might use to avoid any tax increase. Large businesses and their owners could no longer avoid U.S. corporate taxes by using accounting gimmicks to make their domestic profits appear to be earned in a country that will not tax them. Nor could they avoid the corporate tax by structuring their business as a pass-through company that is exempt from it.

This creates an opportunity for Congress to raise the corporate income tax rate with little fear that companies will avoid the resulting tax increase. Kimberly Clausing, a tax professor and former Treasury Department official, has put forth a proposal that would leave in place the 21 percent corporate income tax rate for the vast majority of companies, those with less than $100 million in taxable income, but would add graduated rates that would apply to the few companies with more.39

Her proposal would impose a rate of 25 percent on a corporation’s taxable income between $100 million and $1 billion, 30 percent on its taxable income between $1 billion and $10 billion, and 35 percent on taxable income beyond $10 billion.

As Clausing explains, a small handful of huge corporations are earning nearly all the corporate profits, and these are the companies her proposal would target.

“Of the approximately 500,000 corporate tax returns filed in 2019 with positive tax liability, fewer than 2,000 of them had tax payments of more than $10 million (and thus taxable income nearing $50 million). Indeed, about 99.7 percent of corporate taxpayers fall below those thresholds, and thus even more would be excluded from the reform suggested above.

But most of the tax base would be affected by this reform, since 87 percent of the tax payments are made by corporations above the $10 million tax payment threshold, and 69 percent of all corporate tax is paid by companies with tax payments of more than $100 million (and thus with taxable income nearing $500 million). The average company with more than $100 million in tax payments has $3.2 billion in taxable income.”

Clausing also points out that this reform would have the benefit of pushing back against the increasing consolidation of economic power in the hands of a few, very large companies.

Other Potential Business Tax Reforms

The three business tax reforms just described – requiring corporations to pay a minimum tax on all their profits, making the biggest companies subject to the corporate income tax regardless of their business structure, and raising the corporate tax rate for the largest companies – are the most important building blocks for true tax reform.

Other potential business tax changes could also be very helpful. For example, businesses are allowed to deduct interest they pay on loans, just as they deduct other expenses. But combined with other tax breaks enacted by President Trump and his allies in Congress, these deductions will become a massive tax shelter that Congress may need to eliminate.

Congress has, for years, allowed companies to deduct the cost of acquiring capital assets (like equipment) more quickly than those assets wear out, a type of tax break known as accelerated depreciation. And in some years, Congress has allowed the most extreme form of accelerated depreciation, often called “expensing,” which allows companies to write off the entire cost of such investments in the year they are made. This year’s tax law allows expensing permanently. Proponents claim this will encourage investment, despite evidence that it mainly rewards corporations for investments they would have made in the absence of any such tax break.40

Expensing combined with interest deductions facilitates tax shelters that could push our revenue system towards collapse. Even proponents of expensing acknowledge that it is not compatible with interest deductions.41 [41] The combination of the two encourages investment in money-losing activities for the purposes of generating tax savings that exceed the losses. Put differently, full expensing creates situations where debt-financed investments have negative marginal tax rates.42 Existing limits on interest deductions are weak and were made even weaker by the new tax law.43

Conclusion

The next time Congress and the White House are controlled by responsible leaders, they should reform the federal tax code to more effectively tax the wealthiest individuals in many different ways. This might include federal legislation to better tax unrealized capital gains and other income, better tax estates or inheritances and to tax the net worth of the very wealthiest Americans. This, however, is not enough. To prepare for the possibility that a hostile judiciary or a future administration could sabotage such reforms, the new president and Congress must also enact the far more resilient corporate income tax reforms described here. In the event that the federal government is incapable of directly taxing much of the income that flows to the wealthiest Americans, these reforms would ensure that most of this income is taxed before it reaches them.

Appendix: The Need for a Global Minimum Tax

While corporations have many ways of avoiding taxes, the main focus of the OECD’s global minimum tax is offshore tax avoidance. In this context, offshore tax avoidance generally means that corporations use accounting gimmicks to make profits which are actually earned in countries that would meaningfully tax them appear to be earned by subsidiaries in countries or jurisdictions known as tax havens, where they will be taxed little or not at all.

For example, an American corporation might transfer the ownership of a patent to a subsidiary company that is nothing more than a post office box in a country where it carries out no real business. The subsidiary pays a small one-time fee to the U.S. parent company for the patent. The U.S. parent company then pays hugely inflated royalties to the subsidiary to use that patent—deducting those royalties from its U.S. income, thus lowering its U.S. tax liability.

Real life examples are more complicated, and subject to complex “transfer pricing” rules. But those rules have proven largely ineffective in challenging big corporations and their absurd claims about where their profits are generated.44

The federal corporate tax does include provisions that act to some degree as minimum taxes to address this, but they are not nearly as effective as the OECD global minimum tax. For example, international corporate provisions enacted as part of the 2017 Trump tax law and then modified by the 2025 Trump law in theory impose some restrictions on the worst abuses, but these provisions are convoluted and ineffective. Under these rules, the U.S. taxes offshore profits of American corporations at an effective rate of just 12.6 percent, considerably less than the 21 percent that applies to domestic profits. (The 12.6 percent imposed by the U.S. is reduced by 90 percent of whatever was paid in foreign taxes on the offshore profits, which means no U.S. tax is owed if foreign taxes were paid at a rate of at least 14 percent.)45 While this in theory operates as a minimum tax, American companies can still achieve substantial tax reductions by characterizing their domestic profits as offshore income and benefiting from the lower effective rate.

An even more important problem is that this minimum tax is applied to the foreign profits of a given corporation as a whole rather than applied separately to the profits reported in each country. Effectively, that means higher taxes that a corporation pays in one jurisdiction could offset very low taxes it pays in another jurisdiction (in a tax haven).

For example, an American corporation might claim that a portion of its profits are earned in Foreign Country A where it pays an effective tax rate of just 5 percent. This is likely the result of transactions designed to avoid taxes rather than real investments, but the company would not necessarily be affected by the existing minimum tax. The corporation might pay an effective rate of 20 percent in Foreign Country B. Its overall effective tax rate calculated on its total foreign profits could be more than 14 percent, so the existing minimum tax might not affect it.

These problems would be resolved if Congress enacted the No Tax Breaks for Outsourcing Act, recently reintroduced by Sen. Whitehouse and Rep. Doggett, which would ensure that offshore profits of U.S. corporations are not taxed less than their domestic profits.46 This would bring U.S. tax law closer to the global minimum tax’s income inclusion rule (IIR). In some ways it would exceed the standard set by the IIR because it would subject the offshore profits of American corporations to a rate of 21 percent (the same rate that applies to domestic profits) rather than the 15 percent rate required by the GMT rules. If this were in effect, the type of accounting scheme described above would provide no benefit because the corporation attempting it would end up paying U.S. corporate tax on offshore income that is not taxed by the country where it supposedly is earned.

Endnotes

- 1. “Taxes,” Gallup, https://news.gallup.com/poll/1714/taxes.aspx

- 2. Steve Wamhoff, “Federal Tax Policy: What Should It Accomplish?,” Institute on Taxation and Economic Policy, March 26, 2025. https://itep.org/federal-tax-policy-us-tax-system-what-should-it-accomplish/

- 3. Steve Wamhoff, “SCOTUS Rejects Expansion of Trump’s Corporate Tax Cuts, Leaves Broader Tax Questions for Another Day,” Institute on Taxation and Economic Policy, June 20, 2024. https://itep.org/scotus-moore-v-us-ruling-corporate-tax-cuts-capital-gains/

- 4. Steve Wamhoff, “Hearing Witness: Trump Administration Giving Tax Breaks Not Allowed by Law,” Institute on Taxation and Economic Policy, February 12, 2020. https://itep.org/hearing-witness-trump-administration-giving-tax-breaks-not-allowed-by-law/

- 5. Steve Wamhoff, “Trump Goes Outside the Law to Give Even More Tax Cuts to the Wealthy,” Institute on Taxation and Economic Policy, November 12, 2025. https://itep.org/trump-goes-outside-the-law-to-give-even-more-tax-cuts-to-the-wealthy/; Matthew Gardner, “Biden Tax Reforms Take a $16 Billion Bite Out of Trump’s Big Tax Giveaway to Meta,” Institute on Taxation and Economic Policy, October 30, 2025. https://itep.org/meta-tax-16-billion-trump-biden/

- 6. Steve Wamhoff, Carl Davis, Joe Hughes, Jessica Vela, “Analysis of Tax Provisions in the Trump Megabill as Signed into Law: National and State Level Estimates,” Institute on Taxation and Economic Policy, July 7, 2025. https://itep.org/tax-provisions-in-trump-megabill-national-and-state-level-estimates/

- 7. Steve Wamhoff, “What Tax Provisions are in the Senate-Passed Inflation Reduction Act?,” Institute on Taxation and Economic Policy, August 9, 2022. https://itep.org/what-tax-provisions-are-in-the-senate-passed-inflation-reduction-act/

- 8. Sarah C. G. Christopherson, “IRS Enforcement Boost Was Supposed to Last 10 Years. Congress Killed It in Under Three,” Institute on Taxation and Economic Policy, September 16, 2025. https://itep.org/irs-funding-cuts-inflation-reduction-act-tax-avoidance/

- 9. Flint v. Stone Tracy Co., 220 U.S. 107 (1911) https://supreme.justia.com/cases/federal/us/220/107/

- 10. Steve Wamhoff, “Biden’s plan will stop Jeff Bezos and Elon Musk from avoiding billions in taxes,” Bloomberg, June 19, 2021. https://fortune.com/2021/06/09/propublica-taxes-bezos-buffett-musk-bloomberg/

- 11. Jesse Eisinger, Jeff Ernsthausen and Paul Kiel, “The Secret IRS Files: Trove of Never-Before-Seen Records Reveal How the Wealthiest Avoid Income Tax,” ProPublica, June 8, 2021. https://www.propublica.org/article/the-secret-irs-files-trove-of-never-before-seen-records-reveal-how-the-wealthiest-avoid-income-tax

- 12. This tax break is often called the “stepped up basis” for the heirs who inherit the asset. For example, if you buy an asset for $5 million, your “basis” in the asset is $5 million. If one year later you sell it for $8 million, you realize a gain equal to the $8 million you receive minus your basis of $5 million, which comes to $3 million. (People who are not tax experts would simply say you made a $3 million profit from selling the asset.) But if you die and leave the asset to your heirs, the current rules “step up” their basis to the $8 million that the asset is worth when they inherit it. That means they could sell it right away for $8 million and, under the current rules, they would realize no gains and therefore have no income from the sale of the asset to report on their tax return.

- 13. “Wyden, Cohen, Beyer Introduce the Billionaires Income Tax Act,” United States Senate Committee on Finance, September 17, 2025. https://www.finance.senate.gov/ranking-members-news/wyden-cohen-beyer-introduce-the-billionaires-income-tax-act

- 14. Steve Wamhoff, “The U.S. Needs a Federal Wealth Tax,” Institute on Taxation and Economic Policy, January 19, 2021. https://itep.org/the-u-s-needs-a-federal-wealth-tax/

- 15. Delegates to the Constitutional Convention from southern states wanted slaves counted as part of their populations for determining the number of Representatives elected to the House from each state. At the same time, the southern delegates did not want slaves counted as part of the population for the purpose of any federal tax that was apportioned by population. The men who spoke on behalf of southern states at the Convention wanted to maximize their clout in Congress while minimizing the federal taxes paid by their states.

- 16. Ackerman, Bruce. “Taxation and the Constitution.” Columbia Law Review, vol. 99, no. 1, 1999. https://doi.org/10.2307/1123596

- 17. Dawn Johnsen and Walter Dellinger, “The Constitutionality of a National Wealth Tax,” Indiana Law Journal, Winter 2018, page 114. https://www.repository.law.indiana.edu/ilj/vol93/iss1/8/

- 18. Steve Wamhoff, “The U.S. Needs a Federal Wealth Tax,” Institute on Taxation and Economic Policy, January 19, 2021. https://itep.org/the-u-s-needs-a-federal-wealth-tax/

- 19. Moore v. United States, 144 S. Ct. 1680 (2024). See Steve Wamhoff, “SCOTUS Rejects Expansion of Trump’s Corporate Tax Cuts, Leaves Broader Tax Questions for Another Day,” Institute on Taxation and Economic Policy, June 20, 2024. https://itep.org/scotus-moore-v-us-ruling-corporate-tax-cuts-capital-gains/ Some observers note that the majority’s opinion in Moore suggests that the Pollack court more than a century earlier had erred when they characterized a personal income tax as a direct tax that must be apportioned and that the 16th Amendment merely correct that mistake. See Lily Batchelder et al., “The Moores Lost Their Claim and Moore,” Tax Notes, August 19, 2024. https://www.taxnotes.com/featured-analysis/moores-lost-their-claim-and-moore/2024/08/16/7kkw7 This seems to leave open the possibility that other federal taxes could be struck down in the future as direct taxes if they are not apportioned, such as a tax on net worth or even a tax on unrealized capital gains.

- 20. “Congresswoman Ramirez Introduces Legislation to Tax the Rich,” Congresswoman Delia C. Ramirez Press Release, September 11, 2025. https://ramirez.house.gov/media/press-releases/congresswoman-ramirez-introduces-legislation-tax-rich

- 21. Knowlton v. Moore (U.S. 1900).

- 22. Miller, David S., How Mark-to-Market Taxation Can Lower the Corporate Tax Rate and Reduce Income Inequality, October 20, 2015. https://ssrn.com/abstract=2544048 or http://dx.doi.org/10.2139/ssrn.2544048

- 23. Steve Wamhoff, “Hearing Witness: Trump Administration Giving Tax Breaks Not Allowed by Law,” Institute on Taxation and Economic Policy, February 12, 2020. https://itep.org/hearing-witness-trump-administration-giving-tax-breaks-not-allowed-by-law/

- 24. Jesse Drucker and Jim Tankersley, “How Big Companies Won New Tax Breaks From the Trump Administration,” The New York Times, December 30, 2019. https://www.nytimes.com/2019/12/30/business/trump-tax-cuts-beat-gilti.html

- 25. Jesse Drucker, “How the Trump Administration Is Giving Even More Tax Breaks to the Wealthy,” The New York Times, November 8, 2025. https://www.nytimes.com/2025/11/08/business/trump-administration-tax-breaks-wealthy.html

- 26. Matthew Gardner, “Biden Tax Reforms Take a $16 Billion Bite Out of Trump’s Big Tax Giveaway to Meta,” Institute on Taxation and Economic Policy, October 30, 2025. https://itep.org/meta-tax-16-billion-trump-biden/

- 27. Steve Wamhoff, “Trump Goes Outside the Law to Give Even More Tax Cuts to the Wealthy,” Institute on Taxation and Economic Policy, November 12, 2025. https://itep.org/trump-goes-outside-the-law-to-give-even-more-tax-cuts-to-the-wealthy/

- 28. Daniel Hemel and David Kamin make this argument regarding the possibility of an executive branch unilaterally providing for basis inflation-adjustments for capital gains. Daniel Hemel and David Kamin, “The False Promise of Presidential Indexation,” 36 Yale Journal on Regulation 393 (2019). https://www.yalejreg.com/articlepdfs/36-JREG-693-Hemel.pdf

- 29. Matthew Gardner, Michael Ettlinger, Steve Wamhoff, Spandan Marasini, “Corporate Taxes Before and After the Trump Tax Law,” Institute on Taxation and Economic Policy, May 2, 2024. https://itep.org/corporate-taxes-before-and-after-the-trump-tax-law/

- 30. Steve Wamhoff, Carl Davis, Joe Hughes, Jessica Vela, “Analysis of Tax Provisions in the Trump Megabill as Signed into Law: National and State Level Estimates,” Institute on Taxation and Economic Policy, July 7, 2025. https://itep.org/tax-provisions-in-trump-megabill-national-and-state-level-estimates/

- 31. “Remarks by Secretary of the Treasury Janet L. Yellen at the Brussels Economic Forum,” U.S. Department of the Treasury, May 17, 2025. https://home.treasury.gov/news/press-releases/jy0788

- 32. Upon Trump’s return to the White House, the U.S. government announced that it would not participate in the global minimum tax and Congressional Republicans threatened to impose a “revenge tax” on companies based in countries that impose the global minimum tax on American corporations. The Trump administration called off the revenge tax after G7 issued a shared “understanding” to allow a “side-by-side” system in which the existing U.S. minimum tax rules (which were created by the 2017 tax law and amended by the OBBBA) are deemed to satisfy the global minimum tax rules, despite widespread recognition that they do not. See https://thefactcoalition.org/g7-tax-p2-senate-bill.

- 33. The tax will apply to corporations with average profits exceeding $1 billion over a three-year period. (Foreign-owned companies operating in the U.S. would be subject to it if their three-year average profits in the U.S. exceed $100 million.) Taking this into account, as well as other limits discussed below, the Joint Committee on Taxation projects that only 150 companies will be subject to the minimum tax. See Joint Committee on Taxation, letter to Sen. Ron Wyden, August 1, 2022. https://www.finance.senate.gov/imo/media/doc/CAMT%20JCT%20Data.pdf. The global minimum tax applies to corporations with annual revenue of more than 750 million euros (about $860 million currently). A company could have profits of just, say, $10 million, but could still have revenue exceeding $860 million. For American companies, this means that many more could be affected by the global minimum tax than by the IRA’s minimum tax, which applies only to companies with average profits exceeding $1 billion. The global minimum tax could apply to well more than 1,000 American corporations. (In 2019, about 1,600 corporations complied with reporting requirements that applied to corporations above a similar revenue threshold — $850,000.) See Internal Revenue Service, ”Table 1A. Country-by-Country Report: Tax Jurisdiction Information by Major Geographic Region and Selected Tax Jurisdiction, Tax Year 2019.” https://www.irs.gov/statistics/soi-tax-stats-country-by-country-report

- 34. Steve Wamhoff, “Revenue-Raising Proposals in President Biden’s Fiscal Year 2025 Budget Plan,” Institute on Taxation and Economic Policy, March 12, 2024.https://itep.org/revenue-raising-proposals-biden-fiscal-year-2025-budget/

- 35. Sarah C. G. Christopherson, “IRS Enforcement Boost Was Supposed to Last 10 Years. Congress Killed It in Under Three,” Institute on Taxation and Economic Policy, September 16, 2025. https://itep.org/irs-funding-cuts-inflation-reduction-act-tax-avoidance/

- 36. A publicly traded partnership will not be subject to the corporate income tax if it meets certain requirements, most importantly that 90 percent of its gross income is certain types of investment income or income from mining and fossil fuels. As a report from the Washington Center for Equitable Growth explains, “Sophisticated tax planners, however, have figured out how to “launder” nonqualifying income through blocker corporations, allowing private equity firms and even cemetery operators to win the exemption.” David S. Mitchell, “What the Research Says About Taxing Pass-Through Businesses,” Washington Center for Equitable Growth, April 2024. https://equitablegrowth.org/wp-content/uploads/2024/04/Factsheet-What-the-research-says-about-taxing-pass-through-businesses.pdf

- 37. David Mitchell, “Factsheet: What the research says about taxing pass-through businesses,” Equitable Growth, April 30, 2024. https://equitablegrowth.org/factsheet-what-the-research-says-about-taxing-pass-through-businesses/

- 38. Miles Johnson, Sophia Yan, Chye-Ching Huang, Grace Henley, “Modernizing Partnership Taxation,” Tax Law Center, Hamilton Project, September 25, 2024. https://taxlawcenter.org/work/modernizing-partnership-taxation; Congressional Budget Office, “Taxing Businesses Through the Individual Income Tax,” December 6, 2012. https://www.cbo.gov/publication/43750; Jason Furman, “How to Increase Growth While Raising Revenue: Reforming the Corporate Tax Code,” Hamilton Project, January 28, 2020. https://www.brookings.edu/articles/how-to-increase-growth-while-raising-revenue-reforming-the-corporate-tax-code/

- 39. Kimberly Clausing, “Combating market power through a graduated U.S. corporate income tax,” Equitable Growth, April 15, 2025. https://equitablegrowth.org/combating-market-power-through-a-graduated-u-s-corporate-income-tax/

- 40. Steve Wamhoff, Richard Phillips, “The Failure of Expensing and Other Depreciation Tax Breaks,” Institute on Taxation and Economic Policy, November 19, 2018. https://itep.org/the-failure-of-expensing-and-other-depreciation-tax-breaks/

- 41. Jason Furman, “How to Increase Growth While Raising Revenue: Reforming the Corporate Tax Code,” Harvard University and Peterson Institute for International Economics, January 2020. https://www.hamiltonproject.org/assets/files/Furman_LO_FINAL.pdf

- 42. Mark P. Keightley and Jane G. Gravelle, “CRS Model Estimates of Marginal Effective Tax Rates on Investment Under Current Law,” Congressional Research Service, September 2, 2025. https://www.congress.gov/crs-product/R48277

- 43. A provision of the 2017 tax law limits interest deductions but does not bar companies using full expensing from deducting interest payments altogether. The provision limits interest deductions to 30 percent of adjusted taxable income. Before 2022, the 2017 tax law defined adjusted taxable income as taxable income before interest, taxes, depreciation, and amortization are subtracted. From 2022 on, a stricter definition of adjusted taxable income went into effect, which was taxable income before interest and taxes are subtracted (after depreciation and amortization are subtracted). (This stricter definition was repealed under the OBBBA). The limit does not apply at all to companies with less than $25 million in gross revenue nor does it apply to some specific types of businesses (farms, real estate, certain types of energy).

- 44. In 2020, American corporations claimed profits in 15 of these jurisdictions that were often far too high to be possible. For example, in four jurisdictions – Bermuda, the Cayman Islands, the British Virgin Islands and Barbados – American corporations claimed profits that dramatically exceeded the jurisdiction’s entire economic output. In the first three of these, the claimed profits are more than five times the size of the jurisdiction’s entire economy. See Steve Wamhoff, “Ongoing Use of Offshore Tax Havens Demonstrates the Need for the Global Minimum Tax,” January 17, 2024, Institute on Taxation and Economic Policy. https://itep.org/offshore-tax-havens-corporate-tax-avoidance-demonstrates-need-for-global-minimum-tax/

- 45. The basic international corporate tax rules were enacted as part of the 2017 tax law, were scheduled under that law to become stricter under that law starting in 2026, and then modified as part of the OBBBA. The rules described here will take effect under the OBBBA in 2026.

- 46. “In the Wake of Trump Tariffs, Whitehouse & Doggett Reintroduce Bill to Eliminate Trump’s Outsourcing Tax Breaks That Are Up for Renewal,” Press Release: Lloyd Doggett, February 5, 2025. https://doggett.house.gov/media/press-releases/wake-trump-tariffs-whitehouse-doggett-reintroduce-bill-eliminate-trumps