Vermont

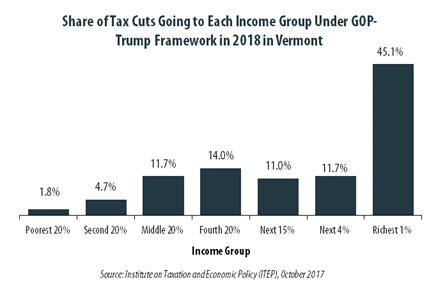

GOP-Trump Tax Framework Would Provide Richest One Percent in Vermont with 45.1 Percent of the State’s Tax Cuts

October 4, 2017 • By ITEP Staff

The “tax reform framework” released by the Trump administration and congressional Republican leaders on September 27 would not benefit everyone in Vermont equally. The richest one percent of Vermont residents would receive 45.1 percent of the tax cuts within the state under the framework in 2018. These households are projected to have an income of at least $505,400 next year. The framework would provide them an average tax cut of $45,250 in 2018, which would increase their income by an average of 3.8 percent.

Astonishingly, tax policies in virtually every state make it harder for those living in poverty to make ends meet. When all the taxes imposed by state and local governments are taken into account, every state imposes higher effective tax rates on poor families than on the richest taxpayers.

State lawmakers seeking to make residential property taxes more affordable have two broad options: across-the-board tax cuts for taxpayers at all income levels, such as a homestead exemption or a tax cap, and targeted tax breaks that are given only to particular groups of low- and middle-income taxpayers. One such targeted program to reduce property taxes is called a “circuit breaker” because it protects taxpayers from a property tax “overload” just like an electric circuit breaker: when a property tax bill exceeds a certain percentage of a taxpayer’s income, the circuit breaker reduces property taxes in excess of this “overload”…

Nearly Half of Trump’s Proposed Tax Cuts Go to People Making More than $1 Million Annually

August 17, 2017 • By ITEP Staff

A tiny fraction of the U.S. population (one-half of one percent) earns more than $1 million annually. But in 2018 this elite group would receive 48.8 percent of the tax cuts proposed by the Trump administration. A much larger group, 44.6 percent of Americans, earn less than $45,000, but would receive just 4.4 percent of the tax cuts.

In Vermont 27.8 Percent of Trump’s Proposed Tax Cuts Go to People Making More than $1 Million

August 17, 2017 • By ITEP Staff

A tiny fraction of the Vermont population (0.3 percent) earns more than $1 million annually. But this elite group would receive 27.8 percent of the tax cuts that go to Vermont residents under the tax proposals from the Trump administration. A much larger group, 41.5 percent of the state, earns less than $45,000, but would receive just 7.1 percent of the tax cuts.

Trump Tax Proposals Would Provide Richest One Percent in Vermont with 39.1 Percent of the State’s Tax Cuts

July 20, 2017 • By ITEP Staff

Earlier this year, the Trump administration released some broadly outlined proposals to overhaul the federal tax code. Households in Vermont would not benefit equally from these proposals. The richest one percent of the state’s taxpayers are projected to make an average income of $1,192,800 in 2018.

Trump’s $4.8 Trillion Tax Proposals Would Not Benefit All States or Taxpayers Equally

July 20, 2017 • By Matthew Gardner, Steve Wamhoff

The broadly outlined tax proposals released by the Trump administration would not benefit all taxpayers equally and they would not benefit all states equally either. Several states would receive a share of the total resulting tax cuts that is less than their share of the U.S. population. Of the dozen states receiving the least by this measure, seven are in the South. The others are New Mexico, Oregon, Maine, Idaho and Hawaii.

Sales Tax Holidays: An Ineffective Alternative to Real Sales Tax Reform

July 12, 2017 • By ITEP Staff

Sales taxes are an important revenue source, composing close to half of all state tax revenues. But sales taxes are also inherently regressive because the lower a family’s income, the more the family must spend on goods and services subject to the tax. Lawmakers in many states have enacted “sales tax holidays” (at least 16 states will hold them in 2017), to provide a temporary break on paying the tax on purchases of clothing, school supplies, and other items. While these holidays may seem to lessen the regressive impacts of the sales tax, their benefits are minimal. This policy brief…

State Rundown 6/28: States Scramble to Finish Budgets Before July Deadlines

June 28, 2017 • By ITEP Staff

This week, several states attempt to wrap up their budget debates before new fiscal years (and holiday vacations) begin in July. Lawmakers reached at least short-term agreement on budgets in Alaska, New Hampshire, Rhode Island, and Vermont, but such resolution remains elusive in Connecticut, Delaware, Illinois, Maine, Pennsylvania, Washington, and Wisconsin.

This week, we celebrate a victory in Kansas where lawmakers rolled back Brownback's tax cuts for the richest taxpayers. Governors in West Virginia and Alaska promote compromise tax plans. Texas heads into special session and Vermont faces another budget veto, while Louisiana and New Mexico are on the verge of wrapping up. Voters in Massachusetts may soon be able to weigh in on a millionaire's tax, the California Senate passed single-payer health care, and more!

Investors and Corporations Would Profit from a Federal Private School Voucher Tax Credit

May 17, 2017 • By Carl Davis

A new report by the Institute on Taxation and Economic Policy (ITEP) and AASA, the School Superintendents Association, details how tax subsidies that funnel money toward private schools are being used as profitable tax shelters by high-income taxpayers. By exploiting interactions between federal and state tax law, high-income taxpayers in nine states are currently able […]

Public Loss Private Gain: How School Voucher Tax Shelters Undermine Public Education

May 17, 2017 • By Carl Davis, Sasha Pudelski

One of the most important functions of government is to maintain a high-quality public education system. In many states, however, this objective is being undermined by tax policies that redirect public dollars for K-12 education toward private schools.

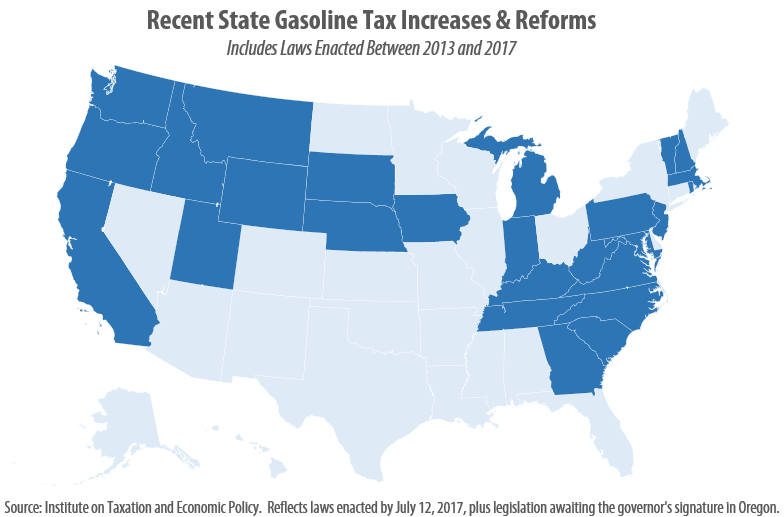

This post was updated July 12, 2017 to reflect recent gas tax increases in Oregon and West Virginia. As expected, 2017 has brought a flurry of action relating to state gasoline taxes. As of this writing, eight states (California, Indiana, Montana, Oregon, South Carolina, Tennessee, Utah, and West Virginia) have enacted gas tax increases this year, bringing the total number of states that have raised or reformed their gas taxes to 26 since 2013.

3 Percent and Dropping: State Corporate Tax Avoidance in the Fortune 500, 2008 to 2015

April 27, 2017 • By Aidan Davis, Matthew Gardner, Richard Phillips

The trend is clear: states are experiencing a rapid decline in state corporate income tax revenue. Despite rebounding and even booming bottom lines for many corporations, this downward trend has become increasingly apparent in recent years. Since our last analysis of these data, in 2014, the state effective corporate tax rate paid by profitable Fortune 500 corporations has declined, dropping from 3.1 percent to 2.9 percent of their U.S. profits. A number of factors are driving this decline, including: a race to the bottom by states providing significant “incentives” for specific companies to relocate or stay put; blatant manipulation of…

Aidan Davis

April 21, 2017 • By ITEP Staff

Aidan is ITEP’s acting state policy director. She coordinates ITEP’s state tax policy research and advocacy agenda and works closely with policymakers, legislative staff, national and state organizations across the country to advance policy solutions that aim to achieve equitable and sustainable state and local tax systems.

Public Assets Institute: Meeting Vermonters’ needs in Fiscal 2018 and beyond

April 17, 2017

Elected leaders acknowledge investments are needed to clean up Lake Champlain, provide families with child care financial assistance, and make higher education more affordable. But progress has been slow in making these investments. And to balance the budget they make cuts—to Reach Up benefits for the poorest families, to affordable housing programs, to key policy […]

The Guardian: My undocumented friend: Carlos does the work few in Vermont want to do

March 31, 2017

While on the campaign trail, Donald Trump called CNN’s Erin Burnett “naive” for suggesting “illegal immigrants” pay taxes. But nationally, they contribute an estimated $11.64bn a year in just state and local taxes, with at least 50% of undocumented immigrant households filing tax returns, according to the non-partisan Institute on Taxation and Economic Policy. Vermont’s […]

State tax debates have been very active this week. Efforts to eliminate the income tax continue in West Virginia. Policymakers in many states are responding to revenue shortfalls in very different ways: some in Iowa, Mississippi, and Nebraska seek to dig the hole even deeper with tax cuts, while the Missouri House’s response has been […]

Undocumented Immigrants’ State & Local Tax Contributions

March 1, 2017 • By Lisa Christensen Gee, Meg Wiehe, Misha Hill

Public debates over federal immigration reform, specifically around undocumented immigrants, often suffer from insufficient and inaccurate information about the tax contributions of undocumented immigrants, particularly at the state level. The truth is that undocumented immigrants living in the United States paybillions of dollars each year in state and local taxes. Further, these tax contributions would increase significantly if all undocumented immigrants currently living in the United States were granted a pathway to citizenship as part of comprehensive immigration reform. Or put in the reverse, if undocumented immigrants are deported in high numbers, state and local revenues could take a substantial…

Combined Reporting of State Corporate Income Taxes: A Primer

February 24, 2017 • By Dylan Grundman O'Neill, Meg Wiehe

Over the past several decades, state corporate income taxes have declined markedly. One of the factors contributing to this decline has been aggressive tax avoidance on the part of large, multi-state corporations, costing states billions of dollars. The most effective approach to combating corporate tax avoidance is combined reporting, a method of taxation currently employed in more than half of the states that tax corporate income. The two most recent states to enact combined reporting are Rhode Island in 2014 and Connecticut in 2015. In several states, including Connecticut, Illinois, Massachusetts, Rhode Island, and Vermont, lawmakers adopted the policy after…

Below is a list of notable resources for information on state taxes and revenues: Alabama Alabama Department of Revenue Alabama Department of Finance – Executive Budget Office Alabama Department of Revenue – Tax Incentives for Industry Alabama Legislative Fiscal Office Alaska Alaska Department of Revenue – Tax Division Alaska Office of Management & Budget Alaska […]

And Then There Were Six: Amazon Expands Its Sales Tax Collection

January 30, 2017 • By Carl Davis

UPDATE: After this post was published, Amazon announced that it will begin collecting sales tax in Oklahoma on March 1. This post has been updated to reflect this development. The nation’s largest Internet retailer has made an about-face on its sales tax policy, making consumers’ ability to evade sales tax on online purchases a little […]

Fairness Matters: A Chart Book on Who Pays State and Local Taxes

January 26, 2017 • By Carl Davis, Meg Wiehe

When states shy away from personal income taxes in favor of higher sales and excise taxes, high-income taxpayers benefit at the expense of low- and moderate-income families who often face above-average tax rates to pick up the slack. This chart book demonstrates this basic reality by examining the distribution of taxes in states that have pursued these types of policies. Given the detrimental impact that regressive tax policies have on economic opportunity, income inequality, revenue adequacy, and long-run revenue sustainability, tax reform proponents should look to the least regressive, rather than most regressive, states in crafting their proposals.

Seven Days: Afford-Ability: Can Gov. Phil Scott Deliver a Bigger Slice of the Pie?

January 12, 2017

“Despite all the ink spilled over the state’s supposedly high tax burden, Vermont’s effective tax rate is roughly average. And according to a 2015 study by the left-leaning Institute on Taxation and Economic Policy, “Vermont’s tax system is among the least regressive in the nation because it has a highly progressive income tax and low […]

State Rundown 1/11: State Legislative Sessions Kick Off Amid Uncertainty

January 11, 2017 • By ITEP Staff

This week brings still more states looking for solutions to revenue shortfalls, multiple governors’ State of The State addresses, important reading on counter-transparency and local-preemption efforts, and more. — Meg Wiehe, ITEP State Policy Director, @megwiehe A Nebraska legislator this week diagnosed the state’s $900 million revenue shortfall in plain terms, describing it as “self-inflicted […]