ITEP's Research Priorities

- 2025 tax debate

- Blog

- Cannabis Taxes

- Citations

- Corporate Taxes

- Corporate Taxes

- Earned Income Tax Credit

- Education Tax Breaks

- Employment

- Estate Tax

- Federal Policy

- Fines and Fees

- Georgia

- Immigration

- Income & Profits

- Income Taxes

- Inequality and the Economy

- Internship Opportunities

- ITEP Work in Action

- Local Income Taxes

- Local Policy

- Local Property Taxes

- Local Refundable Tax Credits

- Local Sales Taxes

- Maps

- Media Quotes

- News Releases

- OBBBA

- Other Revenues

- Personal Income Taxes

- Property & Wealth

- Property Taxes

- Property Taxes

- Publications

- Refundable Tax Credits

- Sales & Excise

- Sales, Gas and Excise Taxes

- Sales, Gas and Excise Taxes

- SALT Deduction

- Select Media Mentions

- Social Media

- Staff

- Staff Quotes

- State Corporate Taxes

- State Policy

- State Reports

- States

- Tax Analyses

- Tax Basics

- Tax Credits for Workers and Families

- Tax Credits for Workers and Families

- Tax Guide

- Tax Principles

- Tax Reform Options and Challenges

- Taxing Wealth and Income from Wealth

- Toolkits

- Trump Tax Law

- Trump Tax Policies

- Trump Tax Policies

- Trump-GOP Tax Law

- Video

- Webinar

- Who Pays?

Creating Racially and Economically Equitable Tax Policy in the South

June 21, 2022 • By Kamolika Das

The South's negative outcomes on measures of wellbeing are the result of a century and a half of policy choices. Lawmakers have many options available to make concrete improvements to tax policy that would raise more revenue, do so equitably, and generate resources that could improve schools, healthcare, social services, infrastructure, and other public resources.

Bloomberg Tax: Flat Income Tax Revival Draws Sharply Mixed Reviews (Podcast)

June 14, 2022

With cash cushions plump with federal pandemic relief dollars and a surge in tax revenues, state legislatures across the country have cut taxes aggressively this year. But several states went further, converting their tiered income tax structures to flat-rate systems. Arizona, Georgia, Iowa, and Mississippi have committed to the flat tax in recent weeks, and […]

Rising Prices: Another Reason to Be Wary of Tax Cutting Right Now

June 10, 2022 • By Carl Davis

Many state lawmakers see any economic challenge as an excuse to cut taxes and in 2022, some are citing inflation as a reason to do so. All eyes today are on the inflation rate facing consumers which, spurred on in part by rising corporate profits, is now running at its fastest pace in decades. But […]

State Policy Associate or Policy Analyst (Policy Team)

June 9, 2022 • By ITEP Staff

Read as PDF The Institute on Taxation and Economic Policy (ITEP) is a non-profit research organization that analyzes tax laws and tax proposals at the federal, state and local levels. ITEP’s work demonstrates the need to raise more revenue from corporations and wealthy individuals. Our small, influential staff works with policymakers and front-line partners to research, support, and develop tax policies that address […]

Georgia Budget and Policy Institute: New Tax Plan Risks State’s Long-Term Fiscal Health, Worsens Income and Racial Inequities

May 27, 2022 • By ITEP Staff

House Bill 1437, signed into law by Gov. Kemp after a final version emerged during the last hours of Sine Die 2022, sets Georgia on course to make fundamental changes to its income tax that primarily benefit the state’s highest earners at an annual cost greater than $2 billion when fully implemented. Beyond adding to […]

Arizona Center for Economic Progress: $2 Billion Tax Cuts for the Rich are Irresponsible

May 13, 2022 • By ITEP Staff

Last year, the legislature passed huge tax cuts whose benefits will only be seen by the richest Arizonans. Once these new tax cuts go into effect, they will reduce state revenues by an estimated $2 billion a year. The state approved a flat tax that will not result in a meaningful tax cut for most […]

Communications Director

April 25, 2022 • By ITEP Staff

Read as PDF The Institute on Taxation and Economic Policy seeks an experienced communications director to build the visibility and influence of our tax policy research. This senior position reports to ITEP’s executive director. ITEP, a non-profit, non-partisan research organization, conducts rigorous analyses of tax and economic proposals and provides recommendations to shape tax policy. […]

Biden’s Proposals Would Fix a Tax Code that Coddles Billionaires

April 21, 2022 • By Steve Wamhoff

Billionaires can afford to pay a larger share of their income in taxes than teachers, nurses and firefighters. But our tax code often allows them to pay less, as demonstrated by the latest expose from reporters at ProPublica using IRS data. According to their calculations, Betsy DeVos, the Education Secretary under former President Donald Trump, […]

Model Development Intern Summer 2022

April 21, 2022 • By ITEP Staff

The Institute on Taxation and Economic Policy, the country’s premier progressive tax policy research organization, seeks a model development intern for 28 hours a week for 10 weeks between June and August 2022, with flexibility on precise dates. Preference given to those available for on-site work in Northeast Ohio but remote applicants may apply.

Some Lawmakers Continue to Mythologize Income Tax Elimination Despite Widespread Opposition

April 19, 2022 • By Kamolika Das

One of the most surprising trends this legislative session is that conservative leaders and the business community joined with progressive advocates to oppose income tax repeal plans. There is a general consensus that income tax repeal is a step too far.

Cannabis Taxes Outraised Alcohol by 20 Percent in States with Legal Sales Last Year

April 19, 2022 • By Carl Davis

In 2021, the 11 states that allowed legal sales within their borders raised nearly $3 billion in cannabis excise tax revenue, an increase of 33 percent compared to a year earlier. While the tax remains a small part of state budgets, it’s beginning to eclipse other “sin taxes” that states have long had on the books.

Long-term troubles for this country and this planet now demand our attention. Progressive tax policy would transform our ability to tackle them.

Frequently Asked Questions and Concerns About the President Billionaires’ Minimum Income Tax

April 6, 2022 • By Steve Wamhoff

Find the answers to some frequently asked questions about President Biden's Billionaires’ Minimum Income Tax, which would limit very wealthy individuals’ ability to put off paying income taxes on capital gains until they sell assets.

DC Fiscal Policy Institute: DC’s Earned Income Tax Credit – The Most Generous in the Nation, but not the Most Inclusive

April 6, 2022 • By ITEP Staff

The DC Earned Income Tax Credit (EITC) is a powerful tool for advancing racial, gender, and economic equity. Modeled after the federal tax credit by the same name, DC’s EITC goes to families and individuals earning low and moderate incomes to help them keep more of what they earn and meet basic needs. It is claimed […]

Racial Discrimination in Home Appraisals Is a Problem That’s Now Getting Federal Attention

March 31, 2022 • By Brakeyshia Samms

With both assessments and appraisals being unfair, homeowners of color are stuck between a rock and a hard place when it comes to determining the worth of what is, for most homeowners, their most valuable asset.

The Commonwealth Institute for Fiscal Analysis: Gas Tax Proposal Misses the Mark

March 29, 2022 • By ITEP Staff

Earlier this month, Virginia Gov. Glenn Youngkin announced a new policy proposal to suspend the state’s 26-cents per gallon gas tax for three months and to cap gas tax rates in future years. If enacted, this policy is likely to miss the mark on helping families in Virginia who are struggling with higher costs, while […]

ITEP Statement on Biden Administration’s Billionaire Minimum Income Tax Plan

March 28, 2022 • By ITEP Staff

The following is a statement from Amy Hanauer, executive director of the Institute on Taxation and Economic Policy, on the Biden administration’s inclusion of a Billionaire Minimum Income Tax in its latest budget proposal: “Creating a Billionaire Minimum Income Tax would ensure for the first time that the very wealthiest people in this country, those […]

What the Biden Administration Can Do on Its Own, Without Congress, to Fix the Tax Code

March 25, 2022 • By Steve Wamhoff

The Biden administration has several options to address tax reform even when Congress is unable or unwilling to help.

Women’s History Month is a Reminder that Sensible Tax Policy is Central to Women’s Economic Security

March 24, 2022 • By Brakeyshia Samms

Women’s History Month is a chance to remember what happens for women when tax policy becomes more progressive, boosts income, and helps make raising a family more affordable.

New Hampshire Fiscal Policy Institute: Expansions of the Earned Income Tax Credit and Child Tax Credit in New Hampshire

March 23, 2022 • By ITEP Staff

Prior to the temporary expansions, nearly one in five likely eligible Granite Staters did not claim the EITC, and approximately 7,745 children were estimated to be eligible for the CTC while the credit was not claimed on their household’s tax return. The potential under enrollment in key assistance programs, along with underutilization of the EITC […]

Tax Breaks for Elderly Taxpayers in the States in 2022

March 21, 2022 • By ITEP Staff

Read as PDF

Georgia Budget and Policy Institute: House Proposes Massive Tax Cuts for Wealthiest, Slashing State Revenues

March 14, 2022 • By ITEP Staff

Members of the Georgia General Assembly are considering legislation that would fundamentally change the structure of the tax code and result in disproportionately large tax cuts for the wealthiest while hundreds of thousands of families would see tax increases or few benefits. This is due to the package’s proposed flat personal income tax rate and […]

What We Can Learn Today from the American Rescue Plan – and Sen. Rick Scott’s Proposed Tax Increases

March 11, 2022 • By Steve Wamhoff

The success of the American Rescue Plan Act is worth revisiting today. Instead of pursuing Sen. Rick Scott’s agenda of making life more difficult for those already working the hardest, Congress should extend or make permanent some of the beneficial policies in ARPA.

California Budget & Policy Center: California’s Tax & Revenue System Isn’t Fair for All

March 10, 2022 • By ITEP Staff

Californians need quality public health and schools, access to affordable housing and clean water, and safe roads and neighborhoods along with many more services to live and thrive – no matter one’s zip code. Accordingly, the state’s tax and revenue system must raise adequate revenue to cover the services provided by state and local governments and make […]

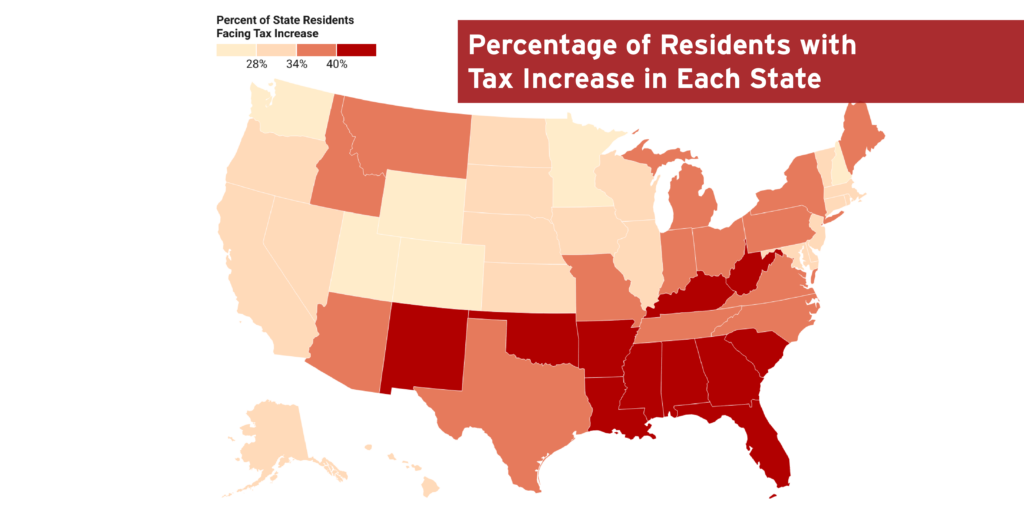

State-by-State Estimates of Sen. Rick Scott’s “Skin in the Game” Proposal

March 7, 2022 • By Steve Wamhoff

A proposal from Sen. Rick Scott would increase taxes for more than 35% of Americans, with the poorest fifth of Americans paying 34% of the tax increase.

Institute on Taxation

and Economic Policy

ITEP is a non-profit, non-partisan tax policy organization. We conduct rigorous analyses of tax and economic proposals and provide data-driven recommendations to shape equitable and sustainable tax systems.

Subscribe to ITEP Emails

Tax research and policy news in your inbox.

Promote Fair Tax Policy

Your gift to ITEP promotes tax justice. With your help, we do research that supports taxing millionaires and billionaires, taxing big corporations and raising revenue for the things our people, our communities and our planet need.

Together, we can create a country with more economic justice, more racial justice, more climate justice… and more tax justice.